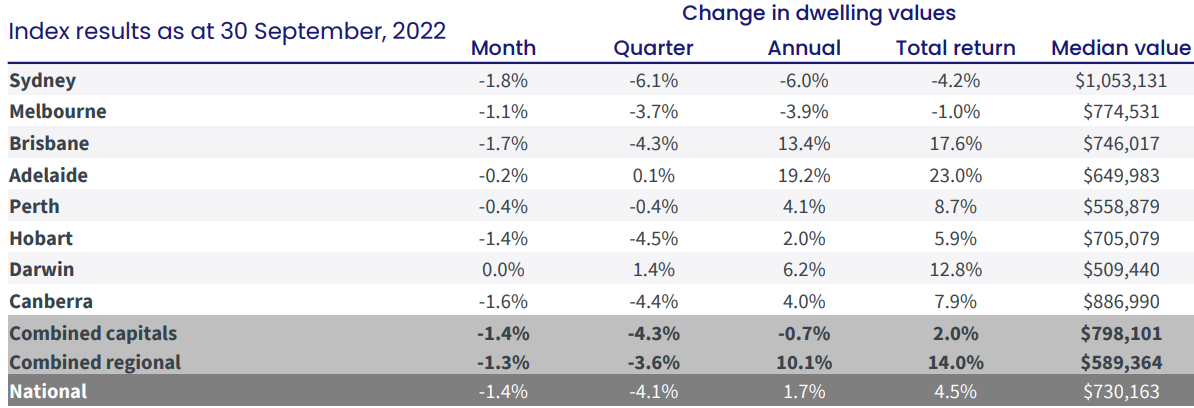

CoreLogic has released its official house price results for September, with national dwelling values falling by 1.4% over the month – a deceleration from the 1.6% decline in August:

As shown above, dwelling values fell across every sub-market except Darwin, where values were flat.

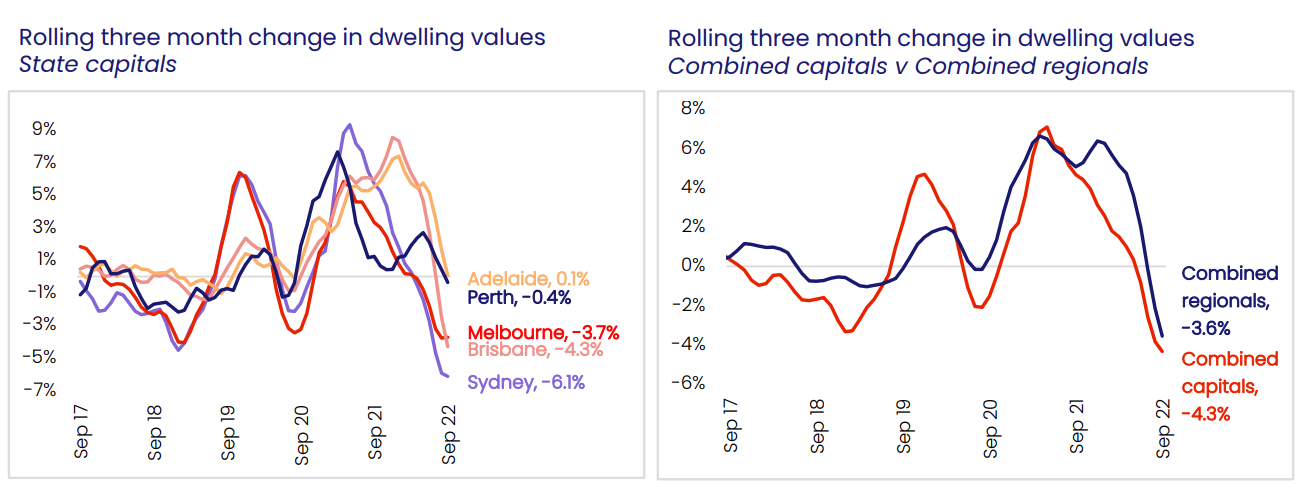

The quarterly pace of decline has accelerated, however, with both the combined capital cities (-4.3%) and regions (-3.6%) bombing:

In fact, the quarterly decline across the combined capitals was the sharpest since the 4.4% fall recorded in January 1983.

After rising 25.5% over the recent growth cycle, housing values across the combined capitals index are now 5.5% below the recent peak, or in dollar terms, down approximately -$46,100.

Sydney continues to record the largest falls, with housing values now 9.0% or – $104,300 below the city’s January 2022 peak.

CoreLogic’s research director, Tim Lawless, is not willing to declare the worst of the downturn over, given it depends largely on what happens with interest rates:

“It’s possible we have seen the initial shock of a rapid rise in interest rates pass through the market and most borrowers and prospective home buyers have now ‘priced in’ further rate hikes. However, if interest rates continue to rise as rapidly as they have since May, we could see the rate of decline in housing values accelerate once again”…

The most important factor influencing housing markets will be the trajectory of interest rates, which remains highly uncertain. The cash rate has surged 225 basis points higher through the tightening cycle to-date; interest rates have not risen at this fast a pace since 1994, when households were arguably less sensitive to a sharp rise in the cost of debt.

“In the September quarter of ’94, the ratio of housing debt to household disposable income was just 46.8. The impact of a higher cost of debt is far more meaningful now, with a housing debt to household income ratio of 143.7 recorded in March 2022,” Mr Lawless said.

A new owner-occupier borrower taking out a $750,000, 30-year mortgage on principal and interest terms, is already paying approximately $943 more per month than they would have pre-rate hikes. Another 50 basis point rise in mortgage rates would (approximately) add $228 per month under the same scenario.

Financial markets are now pricing in a peak in the cash rate around 4.1% between June and August of next year, while private sector economists are generally less bearish, with Bloomberg recently reporting a median forecast of 3.35% as the peak cash rate in the first quarter of next year…

Once interest rates stabilise, housing prices are likely to find a floor.

That is a sound assessment from Tim Lawless. If the RBA continues to hike rates, then it will further crimp borrowing capacity, reducing buyer demand and pushing down house prices.

How deep the correction goes depends on the aggressiveness of the RBA.