Last week, the Reserve Bank of Australia (RBA) surprised interest rate hawks by only lifting the official cash rate (OCR) by 0.25%.

This signaled that the RBA was nearing the end of the rate tightening cycle, even though the minutes explicitly noted that “the Board expects to increase interest rates further over the period ahead”.

In the immediate aftermath, the bond market shaved its OCR forecast by 0.55%, tipping a peak of 3.55% by mid-2023.

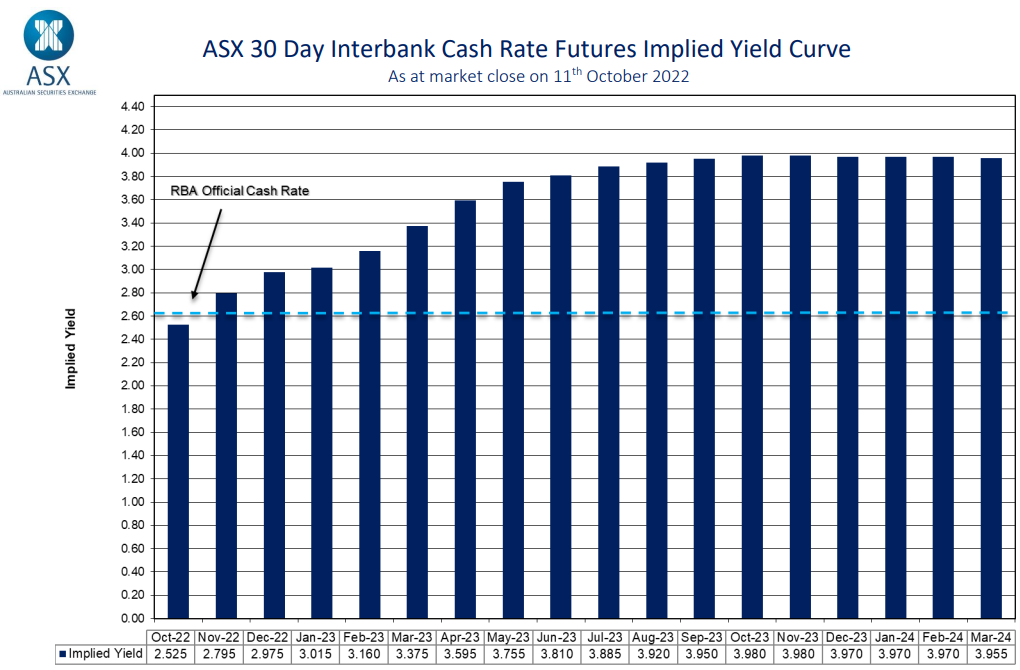

Fast forward a week and the bond market has once again turned hawkish. It now tips the OCR to peak at around 3.95% in a year’s time with rates to remain at this high level until at least Q1 2024:

Bond market ramps OCR forecast.

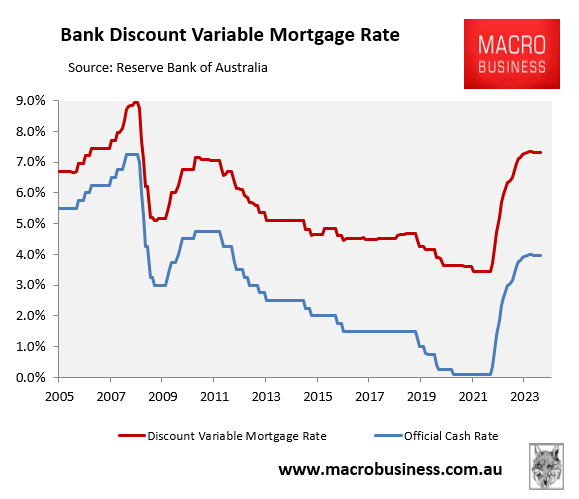

An OCR of 3.95% is a full 1.35% above the current level. It would see Australia’s average discount variable mortgage rate soar to 7.3%, which would be the highest level since October 2008:

Bond market: discount variable mortgage rate to soar to 2008 levels.

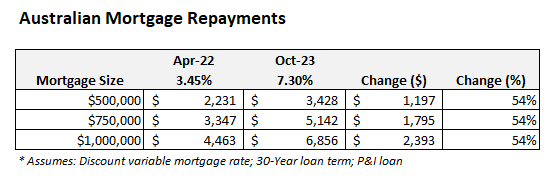

If the bond market’s forecast came to fruition, average mortgage repayments would soar 54% above their April 2022 pre-tightening level:

Such a sharp increase in mortgage repayments would be suicidal for the economy, since it would crunch household disposable income and significantly reduce consumption spending – the economy’s main growth driver.

It would also come on top of the fixed rate mortgage reset, which will tighten monetary conditions absent further rate hikes from the RBA.