By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the headline CPI to increase by 1.6% in Q3 22 (7.0%/yr).

- The trimmed mean CPI on our forecasts will rise by 1.5% (5.4%/yr).

- An outcome in line with our forecasts for both headline and underlying CPI will see the RBA raise the cash rate by 25bp at the November Board meeting.

Overview

High inflation is the main issue for central banks globally. Most major central banks have tightened monetary policy swiftly in an effort to put downward pressure on aggregate demand and in turn inflation. But monetary policy operates with a lag and inflation takes time to respond to changes in interest rates.

The RBA is currently an inflation fighting central bank having delivered an incredible 250bp of tightening in just five months since May 2022. But the RBA became the first major central bank to reduce the size of rate rises in October when the Board increased the cash rate by 25bp, in line with our call (note that this move was a surprise to the market as ~44bp was priced ahead of the meeting). The Board settled on 25bp because of the risks to global and domestic growth and the potential for inflation to subside quickly.

We expect inflation pressures to abate relatively swiftly in 2023. But in the near term the annual rate of inflation will push higher. Indeed the upcoming Q3 22 CPI, due to print on 26 October, is expected to show that inflation pressures remained red hot over the September quarter. This means that monetary policy will be tightened again at the November Board meeting. We consider our forecasts for

both headline and underlying inflation to be consistent with the RBA increasing the cash rate by 25bp at the November Board meeting.

A brief recap of the Q2 22 inflation data

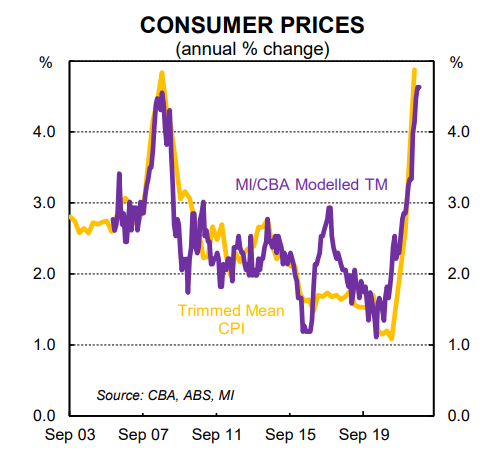

Inflation surged in Australia over the June quarter, as was widely expected. The headline CPI increased by 1.8%/qtr and the annual rate popped higher to 6.1%. For context the headline CPI rose by a larger 2.1% in the March quarter. The trimmed mean, the RBA’s preferred measure of underlying inflation, rose by 1.5%/qtr over Q2 22 to sit 4.9% higher through the year. The ABS upwardly revised the Q1 22 trimmed mean CPI from 1.4%/qtr to 1.5%/qtr which means the quarterly pace of core inflation did not accelerate over Q2 22.

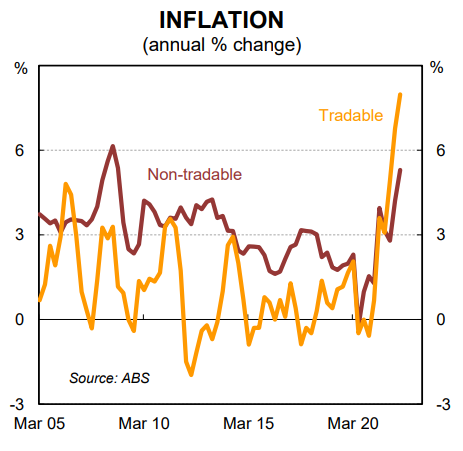

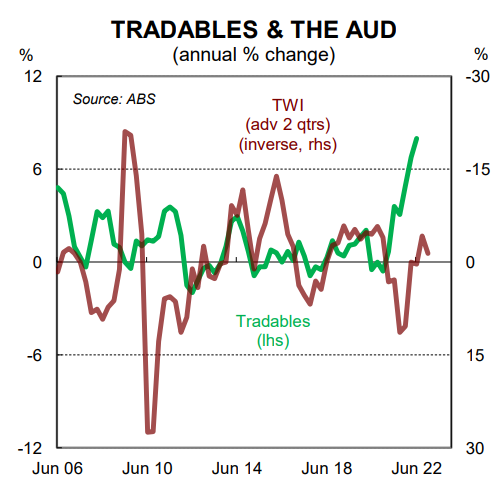

Tradables inflation (i.e. imported inflation) continued to run hotter than nontradables inflation (domestically generated inflation) over the June quarter. Tradables prices rose by 2.7%/qtr to be 8.0%/yr. Non-tradables prices rose by 1.4%/qtr to sit 5.3% higher over the year. Non-discretionary goods and services prices rose by 1.8%/qtr to be 7.6% higher over the year in Q2 22.

Non-discretionary inflation includes goods and services that households are less likely to reduce their consumption of, such as food, automotive fuel, housing and health costs. Discretionary goods and services inflation increased by 1.7% over the quarter to sit at a much lower 4.0% through the year compared to non-discretionary inflation. Discretionary goods and services may be considered ‘optional’ purchases.

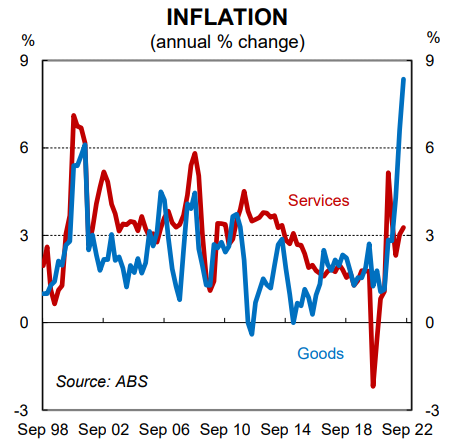

Goods accounted for 79% of the rise in the CPI over the June quarter. Goods inflation sits 8.4% higher over the year while services inflation is ‘just’ 3.3% through the year. Services inflation has a strong positive correlation with wages. As we have remarked on a number of occasions, there is no wage price spiral in Australia like there is in many other jurisdictions.

What to expect in the Q3 22 CPI

The ABS released new monthly CPI data in late September. The data covered the months of July and August 2022. The data was not accompanied by a time series which limits the capacity of economists to fully dissect the information. Notwithstanding the data contained in the release helps us to more accurately forecast Q3 22 CPI (at least in theory, but the proof of the monthly CPI pudding will be in the print next week!).

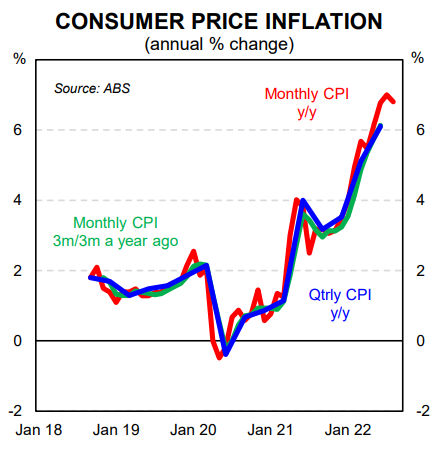

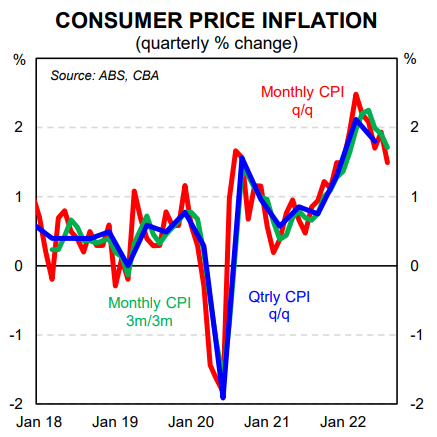

Our forecast is for the headline CPI to increase by 1.6% in Q3 22, a decrease from the 1.8% pace in Q2 22. The annual rate would rise to 7.0%/yr. Such an outcome would mean the quarterly pace of headline inflation has not accelerated, but rather slowed (recall Q1 22 CPI rose by 2.1%/qtr and Q2 22 CPI increased by 1.8%/qtr). Underlying or core inflation looks to be holding at an annualised pace of 6.0% – i.e. ~1.5% a quarter).

The upshot is that Australia’s inflation ‘problem’ is not getting worse. Indeed things will improve from an inflation perspective over 2023 as the lagged impacted of rate hike slows domestic demand growth in the economy.

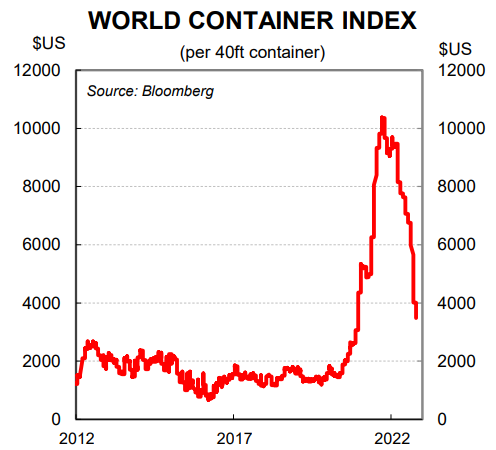

The global picture also looks better on the inflationary front which has implications for Australia. Commodity prices have fallen significantly over the recent past, shipping costs are declining and delivery times have shortened. In summary the supply side of the global economy is gradually improving at a time when the demand for goods will slow. The US is in a different place to Australia given high

wages growth is driving services inflation. But in Australia the monthly CPI indicates services inflation remains reasonably well contained (consistent with annual wages growth of ~3.0%).

While broadly strong, the detail in the upcoming CPI is anticipated to paint a mixed picture as government policies influence out-of-pocket costs for households.

There will be evidence of a cooling in the inflationary pulse from a headline perspective – most notably due to the impact from lower fuel prices and an easing in new dwelling construction inflation. Reduced supply chain disruptions and lower freight costs should also see some easing in tradable goods inflation. But weather and other supply-related disruptions are likely to lead to a tick-up in food inflation. We expect food inflation pressures to dissipate in 2023.

A key source of uncertainty is how some government policies have affected measured price changes in utilities. Government electricity rebates in some states (notably in WA and Qld) will see prices paid by consumers fall. But the exact timing and take-up of the rebates will affect the extent to which electricity prices fall. In Victoria, the rebate is in the form of direct cash payments to households’ bank accounts so we don’t expect this to be measured nor to detract from the CPI (see here for a detailed analysis on the impact of petrol and energy prices on the CPI from Belinda Allen).

On the other hand, the unwinding of some child care support schemes, the end of vouchers for domestic travel and for dining out, and some payback after periods of free public transport in NSW and Tas in Q2 22 will support inflation in the quarter.

Alongside the Q3 22 CPI release will also be the September monthly CPI indicator. The ABS provided a partial media release last month ahead of the RBA Board’s October meeting, but will provide a full set of numbers next Wednesday.

The detail

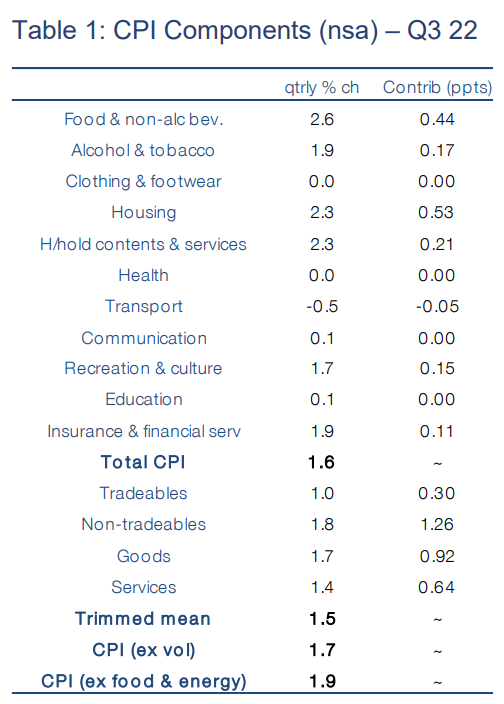

See Table 1 below for our detailed forecasts for the Q3 22 CPI basket.

The main features of our call are as follows:

- a pick-up in food inflation of 2.6%, up from the 2.0% increase the prior quarter on the back of weather and other supply-related disruptions;

- a slight 0.7% increase in utilities as water and gas prices rise by more than the electricity rebates;

- a pick-up in rental inflation to 1.2% offset by easing (but still high) dwelling construction cost growth of 3.6%;

- a large 4% decline in petrol prices detracting 0.2 percentage points from the CPI, and more than offsetting higher urban transport fees and other transportation items;

- a flat outcome for clothing & footwear prices;

- a 1.7% lift in recreation and culture prices, partly reflecting some payback from the impact of vouchers on out-of-pocket expenses for domestic holiday travel & accommodation the prior quarter; and

- a large 7% lift in childcare prices as the end of child care subsidies and before and after school care vouchers reverse the 7.3%/qtr fall in Q2 22.

Our expectation is that the sharp fall in fuel prices and a flat outcome for clothing & footwear should see tradable inflation ease from its 2.7%/qtr pace in Q2 22. Higher prices for meals out & takeaway and child care stemming from the end of vouchers will support higher non-tradeable inflation. Goods inflation is again likely to print higher than services inflation. A key driver of services inflation is wages

growth, which has risen gradually.

Inflation data and the RBA

The RBA’s expectation for inflation to peak at 7¾%/yr in Q4 22 implies quarterly increases of ~1.8% in CPI over the September and December quarters. It is possible, however, that the RBA’s implied profile is not ‘smooth’ (i.e. they expect a different quarterly configuration over Q3 and Q4 22). The RBA forecasts underlying inflation to be 6.0%/yr in Q4 22 which is consistent with quarterly increases of 1.5% over the September and December quarters.

An outcome in line with our forecast would be consistent with a 25bp rate hike at the November Board meeting. We believe a rate hike is locked in on Melbourne Cup Day. But the hurdle for the RBA to go back to a larger than normal 50bp rate increase having slowed the pace of tightening down in October is very high.

The September labour force data certainly does not lend weight to a bigger than 25bp rate rise next month, which means it would require a massive upside surprise on the Q3 22 CPI for a 50bp rate rise to even be on the table in November.

The inflation outcomes next week will of course feed into the RBA’s updated inflation forecasts which will be released in the November Statement on Monetary Policy (SMP). These forecasts will be previewed in the Governor’s Statement accompanying the November Board decision. If the CPI prints broadly in line with our expectations the RBA is unlikely to make any major surgery to their inflation

profile from the August SMP.

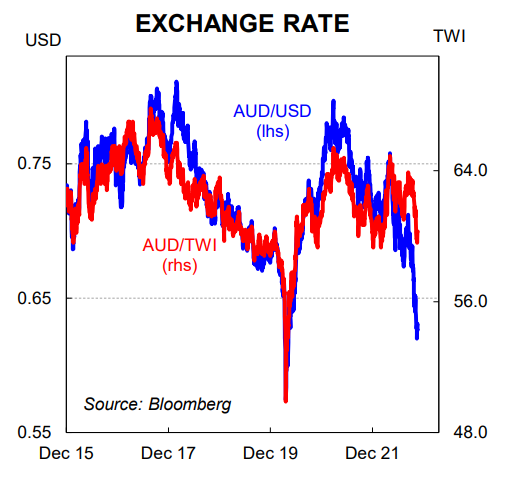

Finally we note that the level of the exchange rate is unlikely to cause the RBA to alter their inflation profile in any material sense. The October Board Minutes noted, “the Australian dollar had depreciated further against the US dollar, but had appreciated slightly over 2022 on a trade-weighted basis. Members noted that the trade-weighted exchange rate typically has a greater bearing on imported

inflation than bilateral rates.”

This is something we have written about frequently over the last two months. Indeed we arrived at very much the same conclusion as the RBA did in the October Minutes. Namely that the TWI matters the most for imported inflation and the AUD has held up on a TWI basis.