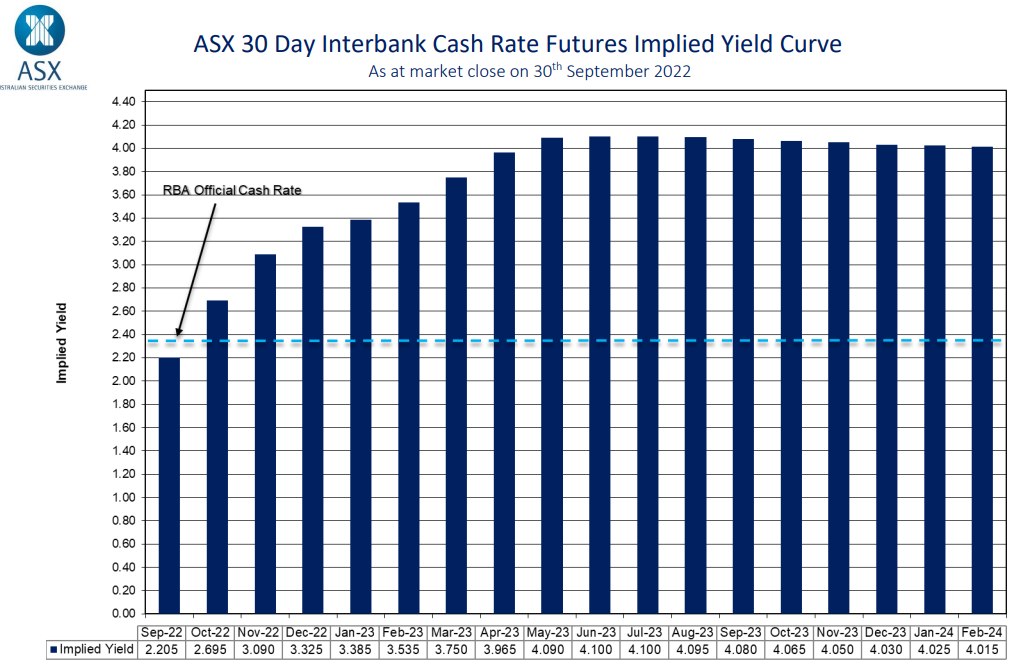

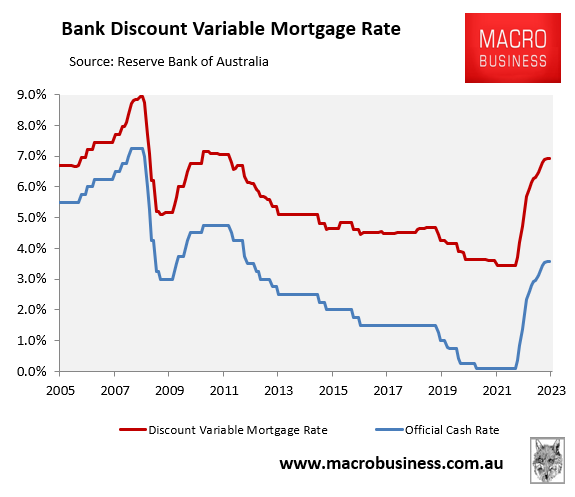

On Friday, the bond market tipped the official cash rate (OCR) would peak at 4.10% in mid-2023, which would have seen Australia’s average discount variable mortgage rate soar to 7.45% – the highest level since October 2008:

Bond Market uber hawkish on 30 September.

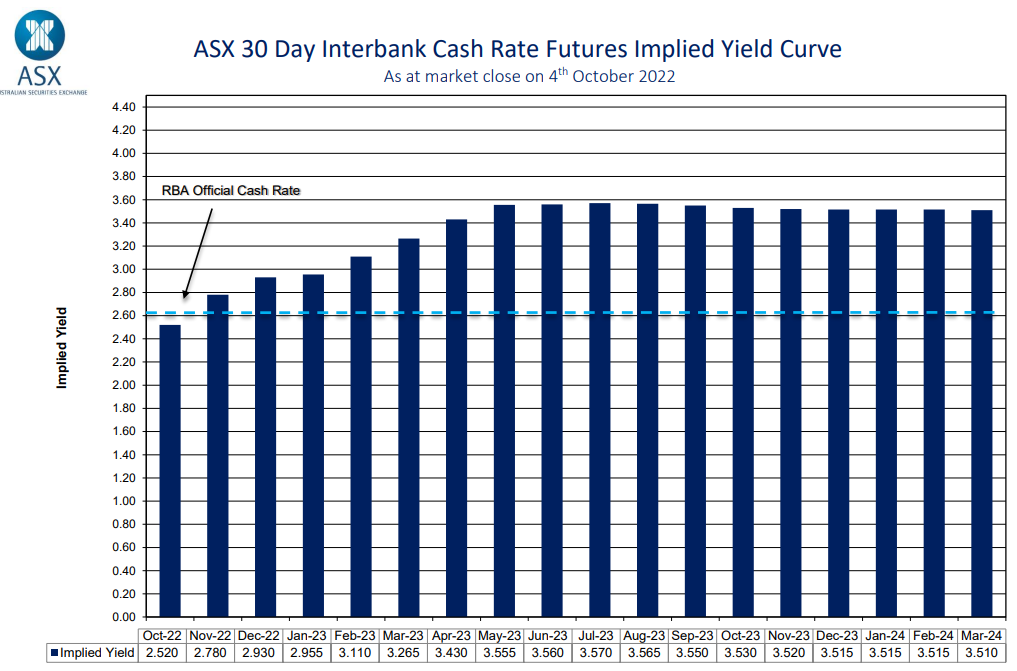

After Tuesday’s ‘shock’ 0.25% increase in the OCR by the RBA, the bond market has slashed 0.55% from its pricing, now tipping a peak OCR of 3.55%:

OCR forecast takes a haircut.

An OCR of 3.55% is still far too bullish given it is a full 0.95% above the current OCR level. It would also see Australia’s average discount variable mortgage rate climb to 6.9%:

Bond market pricing suggests peak mortgage rate of 6.9%.

In Tuesday’s monetary policy statements accompanying the OCR decision, the RBA noted that “higher inflation and higher interest rates are putting pressure on household budgets, with the full effects of higher interest rates yet to be felt in mortgage payments”. It then stated that “the Board expects to increase interest rates further over the period ahead”.

This to me suggests that we will probably see one or two more 0.25% hikes before the RBA is done, which suggests a peak cash rate of around 3.1%.

Time will tell. However, I still fully expect the RBA to be cutting rates mid next year as the global economy plunges into recession and the local economy stalls.

After these cuts are delivered, the housing market will then begin a new up cycle and we’ll be off to the races.