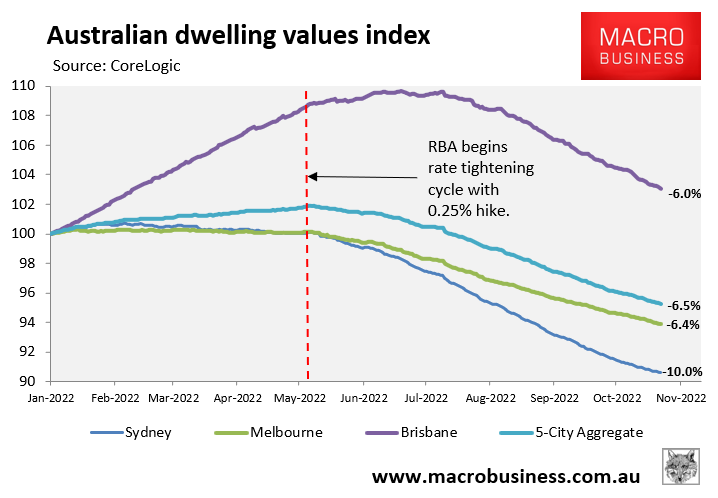

According to CoreLogic’s daily dwelling values index, home values at the 5-city aggregate level have fallen by 6.5% from their recent peak, led by a 10% decline across Sydney:

Sydney leads house price falls.

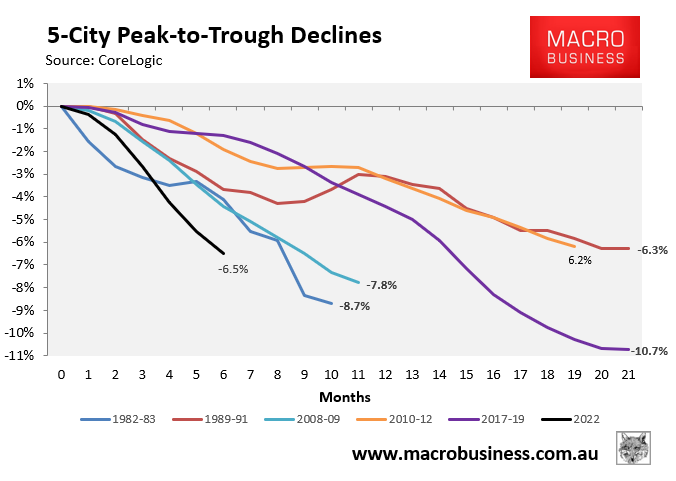

This represents the fastest rate of decline in records dating back to 1980:

Record pace of decline.

Advertisement

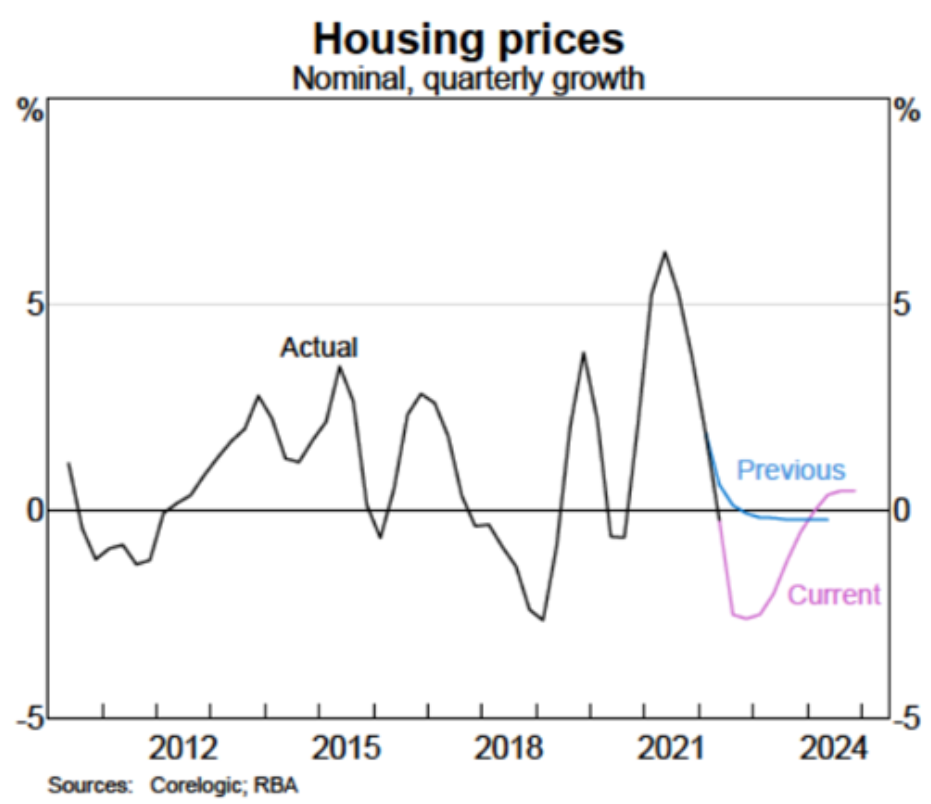

Now Coolabah Capital’s Chris Joye has released analysis of Reserve Bank of Australia (RBA) house price forecasts, which shows that the RBA forecasts this housing correction to be the largest on record:

In July, the RBA had radically modified its house price forecasts, commenting that “the profile for housing price growth had been downgraded”:

“Housing prices unexpectedly declined in the June quarter, and the higher path for interest rates has pushed down the profile relative to the previous [May] Statement [on Monetary Policy]. In addition, we have applied some downward judgement to our housing price profile to reflect downward momentum in the housing market. House prices are now expected to decline by 11% by mid 2023″…

The upgraded August forecast, which is the pink line, forecasts a record 11% drop in national house prices, which is now much closer to our 15-25% forecast from October 2021…

Advertisement

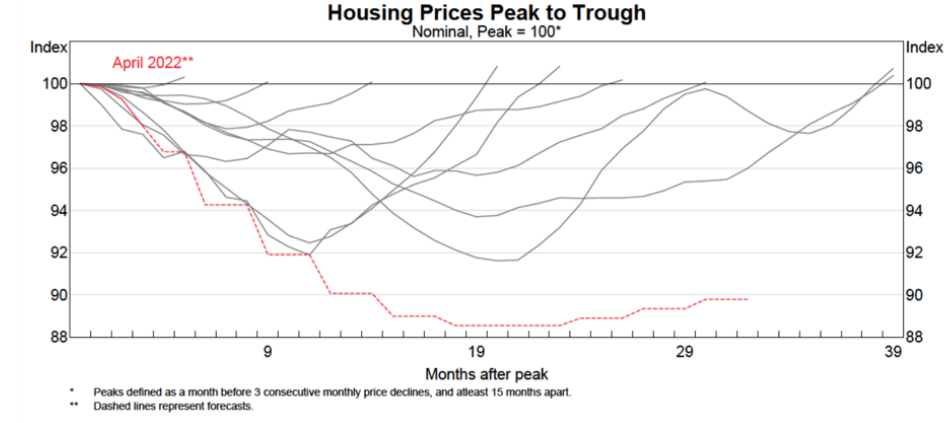

In separate analysis, the RBA also forecast that real dwelling values would decline by 20%, which would be the largest on record:

“In real [inflation-adjusted] terms, prices are forecast to decline by almost 20 per cent (Graph 4). This is also the biggest decline since at least 1980. The previous real‐terms decline that comes closest to that forecast is the 1982 episode.”

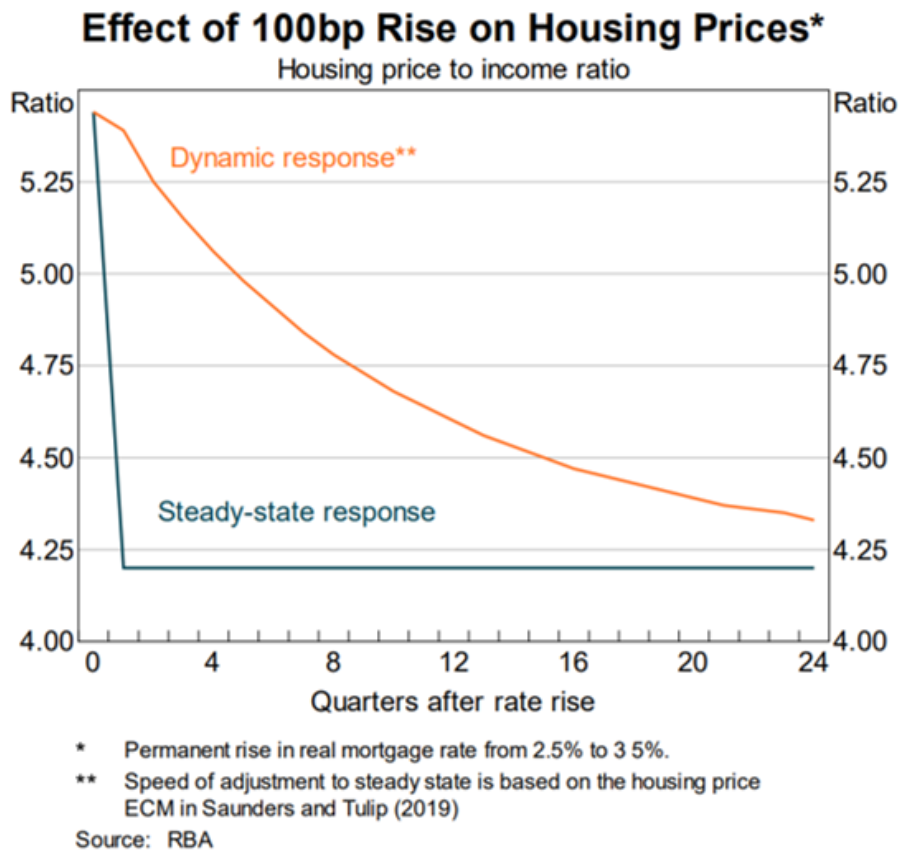

Joye also notes another internal RBA research paper that examined the impact of changing mortgage rates on house prices using a variant of the Saunders-Tulip model. This paper models that “a 100 basis point increase in the mortgage rate from 2.5 to 3.5 per cent” estimates “[house] prices gradually decline toward their new steady state level, 22 per cent lower than the pre-shock level”:

Advertisement

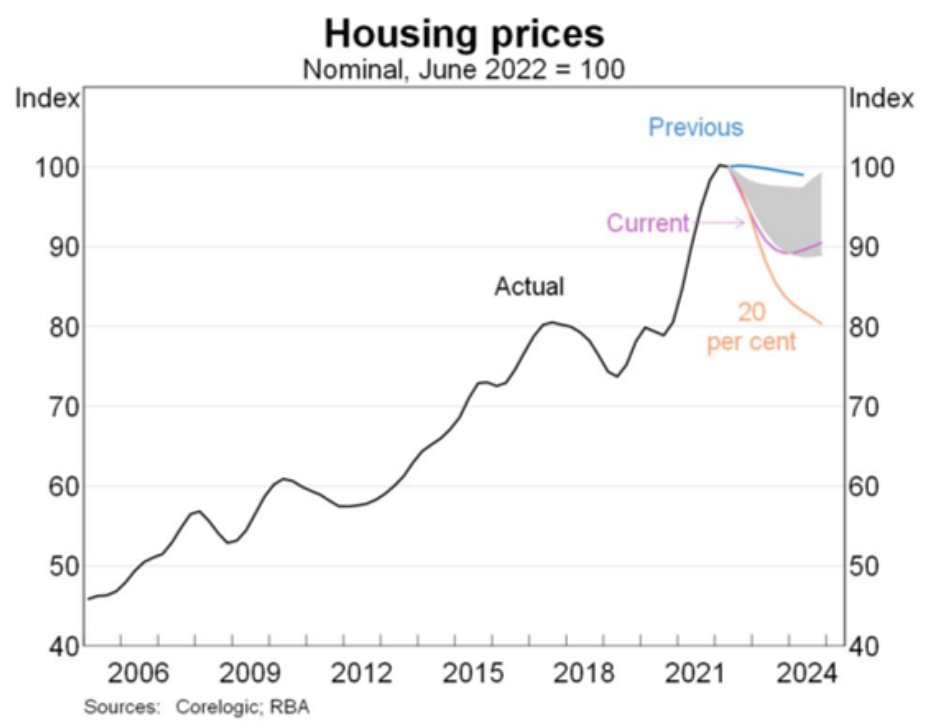

Finally, the RBA developed a downside scenario using the same Saunders-Tulip model whereby they adjusted their assumption regarding households’ expectations of future house price growth. This estimated a 20% peak-to-trough nominal decline in Australian dwelling values:

We’ve constructed a downside housing price scenario within the Saunders Tulip framework by assuming people become pessimistic about the outlook for housing prices. That could be a response to ongoing price declines, or could be prompted by higher interest rates. Specifically we adjust the expected capital appreciation term to be -1.5% pa rather than the long run average of 2.6% pa. In this scenario, housing prices decline by 20 per cent peak-to-trough by the end of 2024. So this is roughly twice as large as what we’ve assumed in our baseline, and sits below the range of estimates from our suite of models and most market economists.

Advertisement

Chris Joye has done an excellent job here parsing the RBA’s Australian house price forecasts.

The key takeaway is that Australian house prices are facing a record decline that will likely smash prior episodes.

Nobody should be surprised by this result given the RBA is delivering the most aggressive interest rate increases in this nation’s history.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.