There are really stupid arguments around that the RBA must follow the Fed into a major economic accident. BofA nicely captures the lunacy of it:

Mounting pressure for a higher terminal rate

All else equal, members saw the case for a slower pace of increase in interest rates as becoming stronger as the level of the cash rate rises…”-excerpts from the September RBA board meeting Minutes stand to be tested as the international backdrop and domestic challenges make it increasingly difficult for the RBA to deliver a slower pace of hikes in the near-term. We now expect the RBA to deliver 50bps hikes each in October and November with a higher terminal rate at 3.75% due to increased pressure to continue front-loading policy. .

Domestically, inflation is expected to further accelerate when the Australian Bureau of Statistics (ABS) releases third quarter data later next month. The Reserve Bank of Australia (RBA) expects prices to rise just under 8% by end-2022 while the market has penciled in a 7.4% increase in overall prices for 3Q. We expect an annual rate above 8% in 3Q. While wages are anticipated to grow at a slower pace in comparison to prices, tight labor market conditions will ensure that unemployment stays low in the near-term to boost incomes and support spending.

Ongoing focus on the labor market

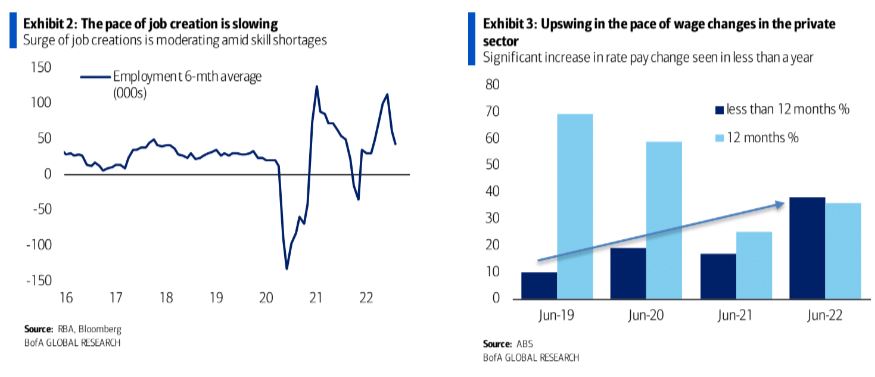

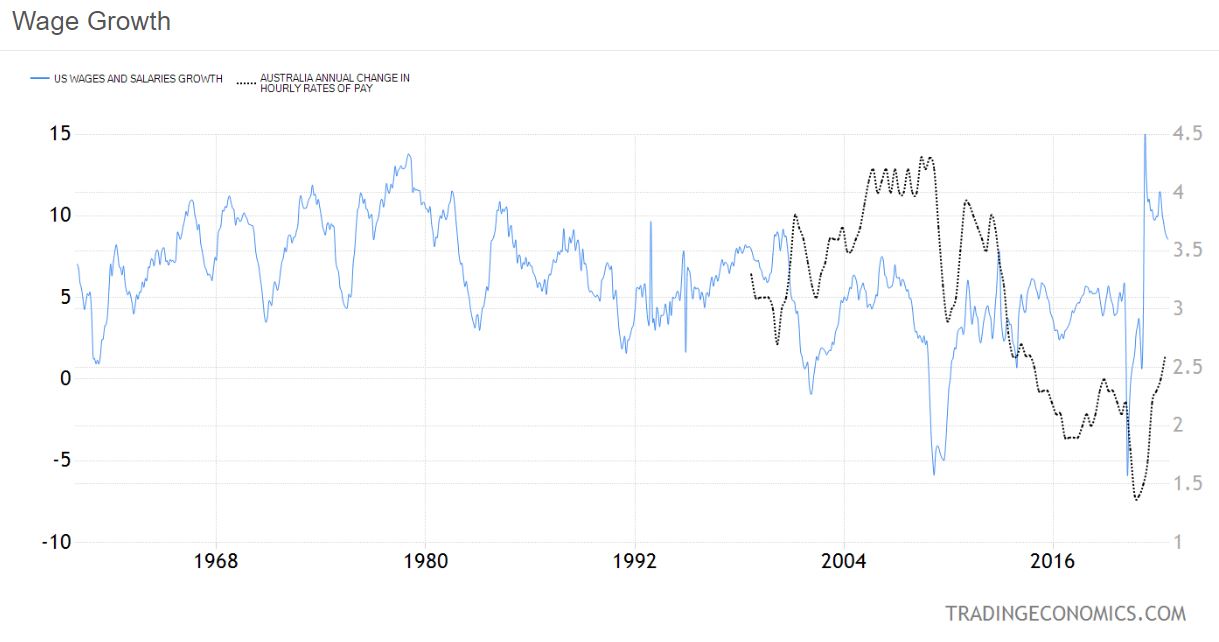

While there is little sign yet of traction from rate hikes on consumer spending, the pace of job creation seems to be moderating (Exhibit 2). This might be due to labor shortages and rising uncertainty over the outlook. We expect the RBA to highlight labor market tightness in its guidance when it meets on 4 October. Although there has been a slight uptick in the unemployment rate since the last meeting, data shows increasing wages pressure across the private sector via an acceleration in the pace of wage setting that is likely to extend into the public sector (Exhibit 3).

At the government Jobs and Skills Summit concluded earlier this month, the Federal government pledged to increase the permanent migration intake from 160,000 to195,000 this year and expedite visas for foreign workers to curb the “over-reliance upon temporary labor” which has resulted in the demand-supply imbalance in the labor market, having contributed to keeping inflationary pressures robust. While the increased supply of skilled labor would help ease the burden on corporates in the long run, it doesn’t necessarily translate to solving the labor market crisis in the near-term. There are471k job vacancies at present compared to 488k unemployed persons. Growth in migration levels might help to limit the potential weakness in the housing market, but will do little to ease the pressure on rents.

Australian wages are growing at 2.6%. Sure, the growth rate is climbing but that’s good! With immigration resuming it is only a matter of time before this peters out so keeping some momentum into the glaringly obvious global bust will help prevent a boom and bust cycle directly into another lost decade of wages weakness.

Wages are not driving Australian inflation at all. They are holding it back as excess profits are pushing up prices. The inflation we have in Australia is going to fade of its own accord as the global recession arrives. A falling dollar is not going make this worse as global demand craters.

Advertisement

As well, the US has completely the opposite problem. Its participation was clubbed by the pandemic (given going out meant death for many) and wage growth exploded above 10%. It is still at 6.7%, nearly triple that of Australia:

Moreover, if you are going to argue that all else is no longer equal for the RBA because the must tighten then you must also point out that the other major change is mushrooming market stress. Not just stocks but deep credit markets:

Advertisement

Treasuries are historically illiquid.

FRA-OIS is through the roof.

China is seeing marginal funding stress.

UK is borderline an emerging market.

IG and HY spreads are blowing out worldwide.

Why doesn’t Tony Morris read his own bank’s research? Something is about to break:

Following the BOE action on Wednesday, the 10yr Gilt yield dropped an incredible 60bpsintraday, allowing the US 10yr to rally by 25bps, an extreme 4x st dev daily move. This still left us with 10yr at +30bp since last Wednesday. Index spreads are +60bp on the week to 547, although this reflects stale index pricing on Wednesday. With HYG +2ptson the day; so realistically we closed about 20bps tighter. Truly remarkably, high quality has outperformed for the week, with IG 25bps ahead of HY in total returns, and BBs60bps ahead of CCCs. LQDflows:-$1.4bn on Monday; +$1.3bnon Wednesday.

Our Credit Stress Indicator (CSI) has jumped 4pts on the week to close at 74th pctle. This level exceeds the June peak of 71 and stands borderline critical zone, which we estimate to be north of 75. Most CSI components have deteriorated away from issuance input, which was already at historical peak stress going into this. Low quality distress, dispersion, and debt/EVs are all above June peak levels now.

…With credit stress approaching critical levels, now is the time to put emphasis on risk management. This means slower pace of rate hikes at immediate upcoming meetings and a potential pause subsequently, to allow the economy to fully adjust to all the extreme tightening already implemented, but still working its way through the financial system’s plumbing. Failure to do so raises the risk of credit market dysfunction, which, if occurred, would be difficult to contain and fix.

Advertisement

The RBA’s reputation is already trashed among overseas investors after it abandoned yield curve control years early. That’s why the Aussie curve is so stupidly steep. It’s an RBA idiocy premium in the long end. It would be darkly amusing indeed if the RBA interpreted this as a signal that inflation is strong because growth prospects are.

If the bank now rushes into more hikes on the eve of a global bust, guaranteeing that it arrives in Australia with greater force, then Phil Lowe will also lose any credibility he has left at home.

Take a chill pill. Australia does not need to hike.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.