Recall that in July’s “Great Housing Debate” against Coolabah Capital’s Chris Joye, Stephen Koukoulas (‘The Kouk’) forecast a peak-to-trough decline in Australian dwelling values of only 7% off a forecast peak in the official cash rate (OCR) of 3.0%:

“Peak to trough is minus 7%… That assumes 300 basis points of rate hikes from the RBA… So a 7% decline…

“It will probably occur in the middle parts of 2023 to the latter part of 2023… In fact the reason for a 7% decline and not much more than that is obviously interest rates have some impact, not the dominant issue clearly”…

Yesterday, CoreLogic released its September house price results, which revealed that “housing values across the combined capitals index are now -5.5% below the recent peak, or in dollar terms, down approximately -$46,100”.

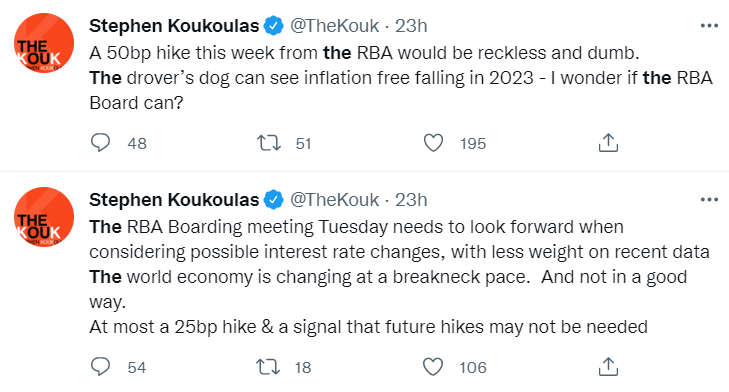

With Australia’s house price correction fast approaching the Kouk’s forecast 7% peak-to-trough decline off an OCR of only 2.35%, he took to Twitter yesterday begging the RBA to halt rate rises:

While I wholeheartedly agree with the Kouk’s latest position on rate hikes, he has until recently been very hawkish on interest rates and implored the RBA to ignore the ‘doomsayers’ arguing against aggressive tightening.

For example, only a fortnight ago, the Kouk argued that 2.25% of rate hikes over five consecutive monetary policy meetings was “normal”, rather than the sharpest rate of tightening in this nation’s history:

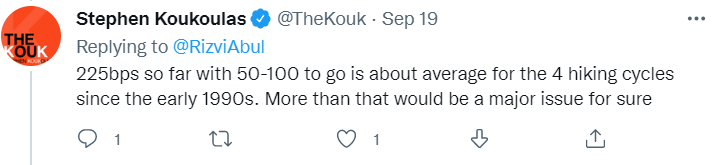

Then when challenged on his “normal” claim, the Kouk said that another 0.5% to 1.0% of tightening “is about average for the four hiking cycles since the early 1990s”:

It seems the Kouk has come to the realisation that his forecasts of a 7% peak-to-trough house price fall and an OCR of 3% are incompatible. If the RBA hikes to 3%, then house prices will necessarily fall much further.