The AFR’s Economics editor, John Kehoe, claims the Reserve Bank of Australia (RBA) is “still behind the curve on inflation” and must hike interest rates much harder:

Australia has an inflation problem like most of the world, and worse is still to come as surging electricity and gas bills hit household budgets harder next year…

The RBA remains behind the curve in slaying inflation and will need to continue to ratchet up interest rates well into next year…

There is an argument for an almighty shock and awe move next week to convince the public that the RBA is determined to crunch inflation and avoid inflation expectations getting out of control. The bank will likely continue hiking interest rates in February and beyond after taking a holiday break in January…

Of utmost concern to the RBA will be the broadening inflation pressures across a wide range of goods and services, including energy, housing and food.

I couldn’t disagree more.

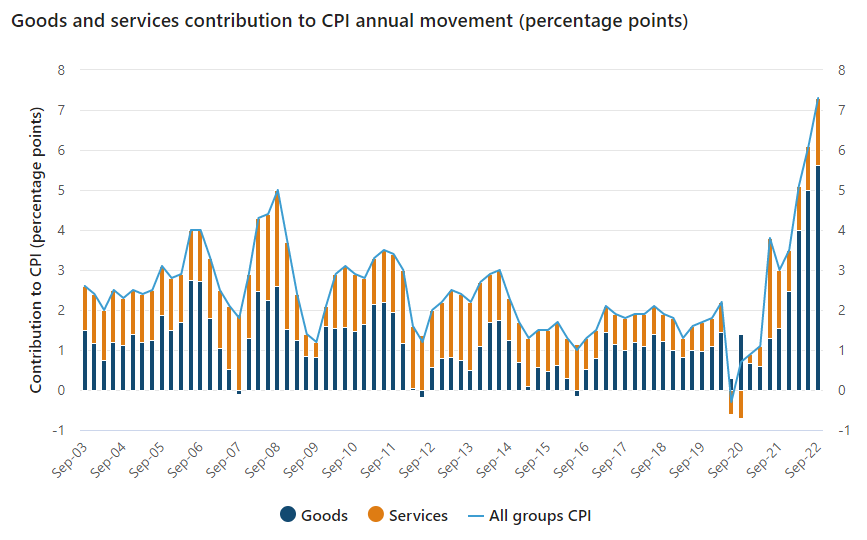

Over three quarters of Australia’s CPI growth was from goods, whereas services (which comprises 80% of the economy) continued to experience only moderate inflation:

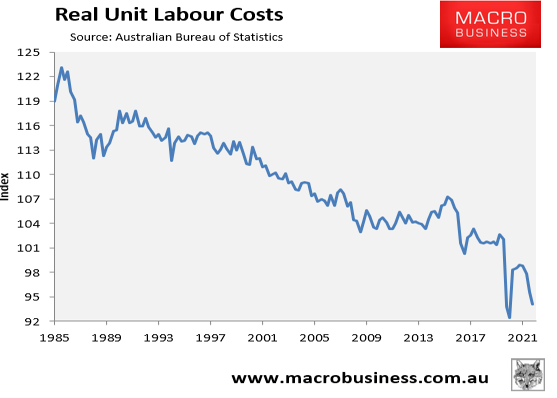

Services inflation is most tightly linked to wage growth, which remains modest and actually disinflationary given Australia’s falling real unit labour cost:

Thus, the broadest measure of demand-driven inflation remains well in check.

Instead, most of the inflationary pressures are imported or weather related, which has driven up goods inflation.

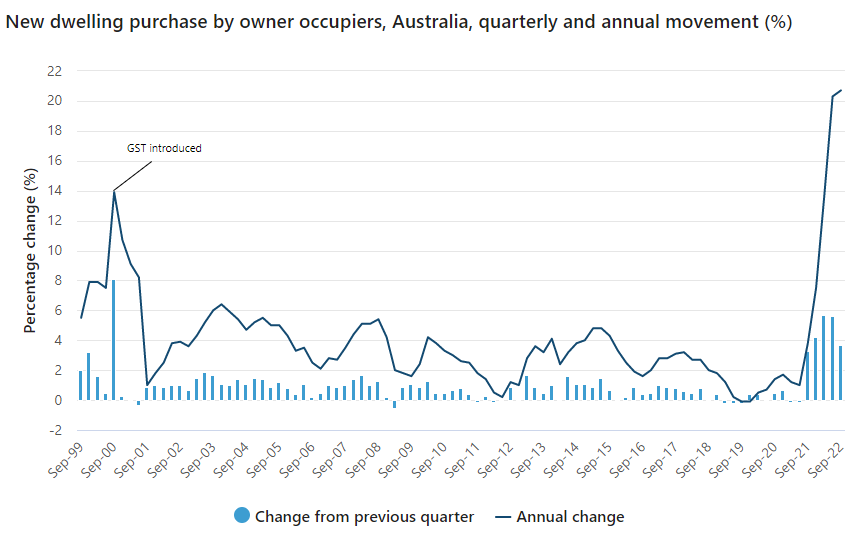

The biggest source of domestic non-tradable inflation was “New dwelling purchase by owner occupiers (+3.7%)”, which has soared 21% over the past year:

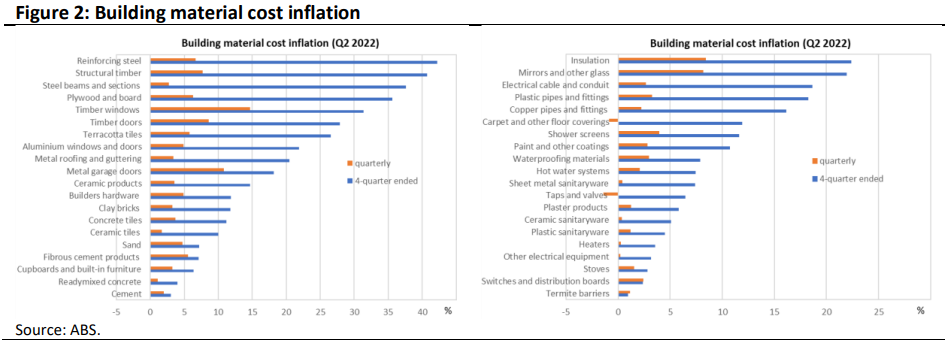

This inflation has been driven by soaring materials costs, most of which are imported or impacted energy, which has inflated the cost of new homes:

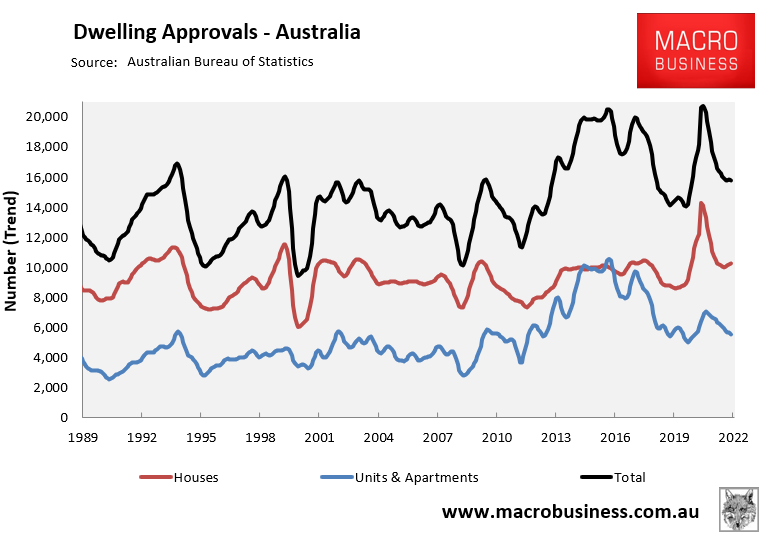

Dwelling approvals have already collapsed:

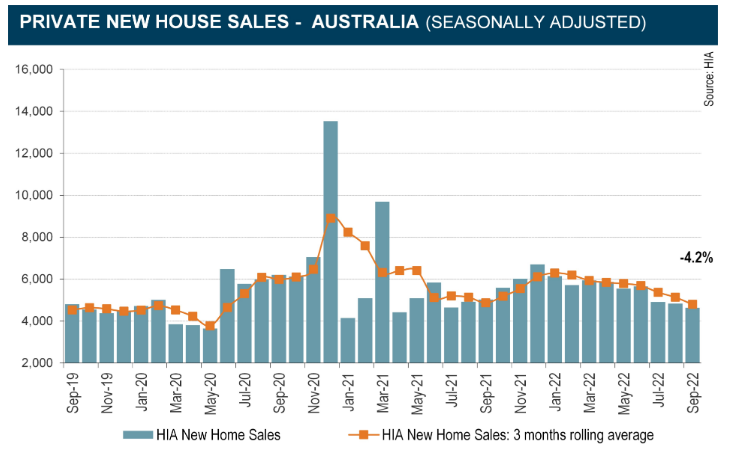

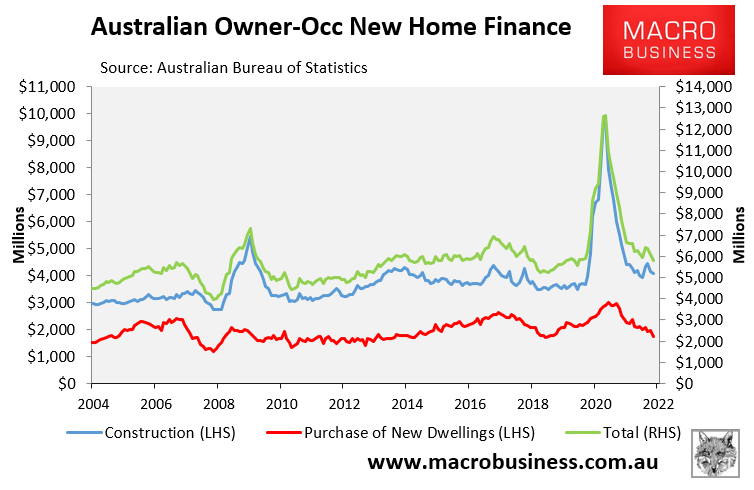

As have new home sales and new home finance:

So, excessive demand is not the problem given it has already dived in response to rate hikes.

Ultimately, the factors driving up Australian inflation are mostly imported, weather-related, or due to failures of government policy (e.g. gas and electricity prices). Whereas the broadest measure of demand-driven inflation – wages – remains weak.

Therefore, Australia’s inflationary troubles will not be resolved by simply hiking rates into the stratosphere, which will only succeed in plunging the economy into a nasty recession while inflation remains high.

Instead, the Albanese Government needs to do its job and help the RBA by fixing the east coast energy market through direct intervention, such as via super profits taxes, domestic gas reservation, and/or price caps and export levies.