Nobody is worried about it yet, but oil is grinding higher:

Advertisement

And so are base metals:

Miners cock-a-whoop:

Advertisement

EM stocks find some relief at last:

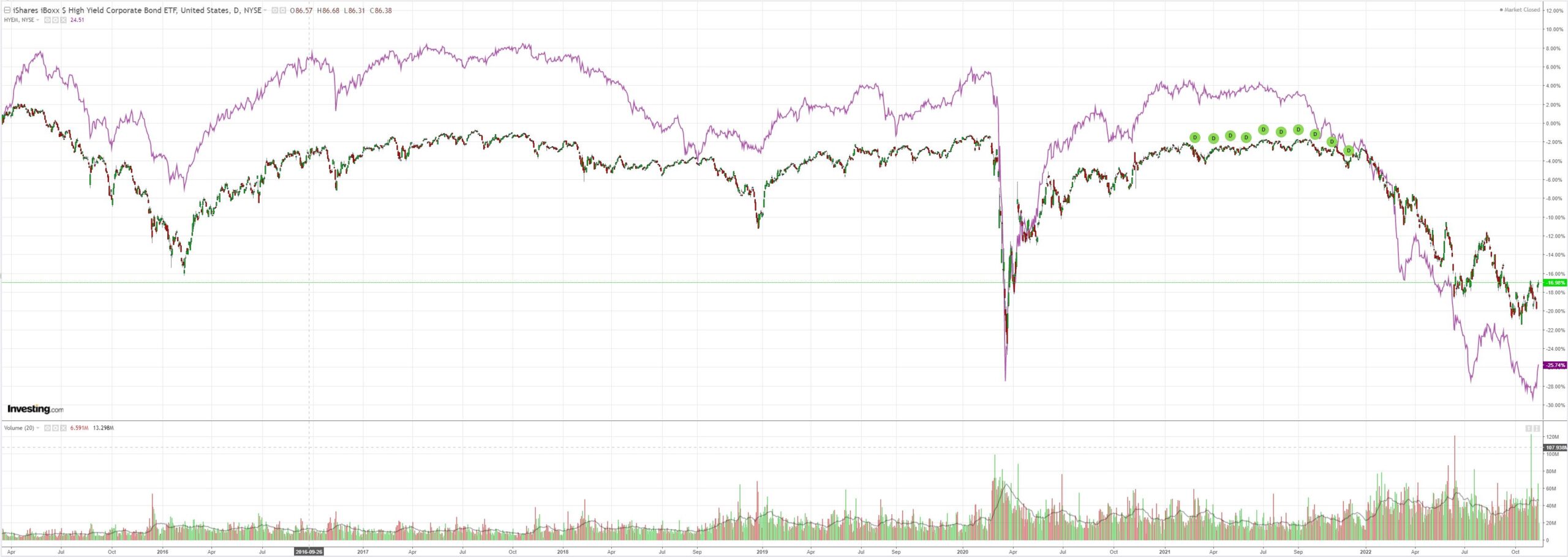

I would hesitate to call the rally credit-led but it is helping:

Advertisement

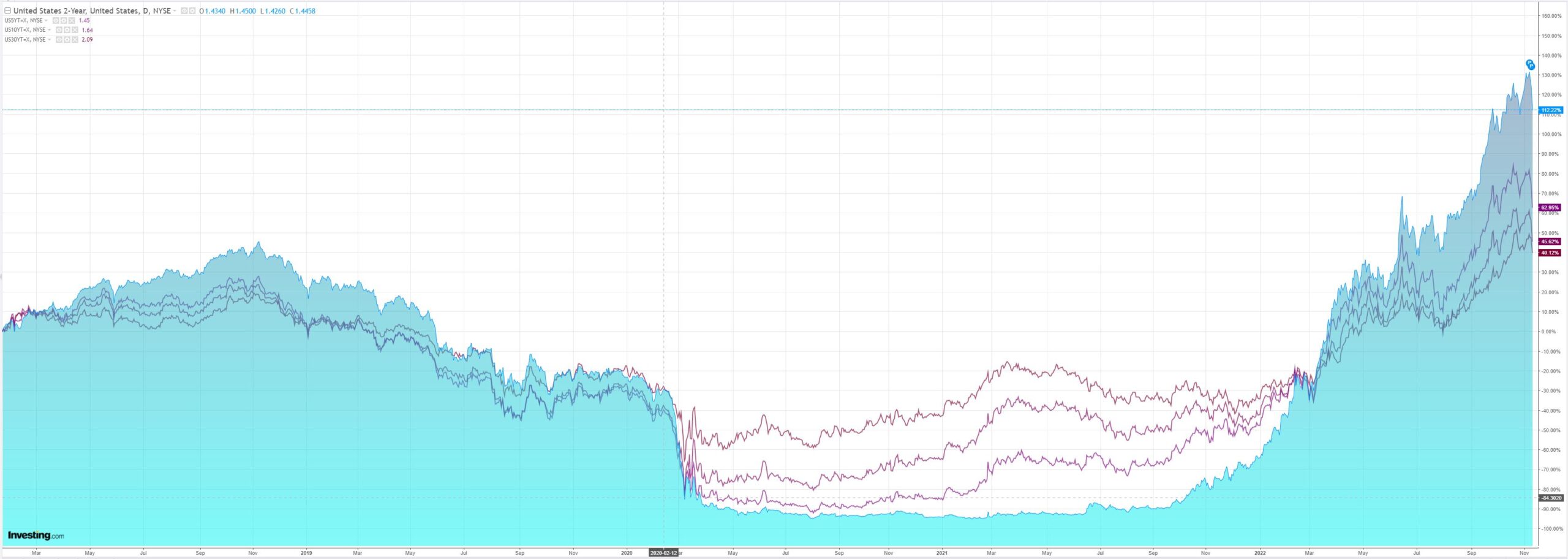

The Treasury curve steepened:

Stocks made further gains:

For me, the Chinese easing of zero-COVID would be better described as a move away from angry zero-COVID. The 20 news measures appear directed more at curbing official lockdown excesses.

Advertisement

There’s a lot of wood to chop before we get any substantial reopening.

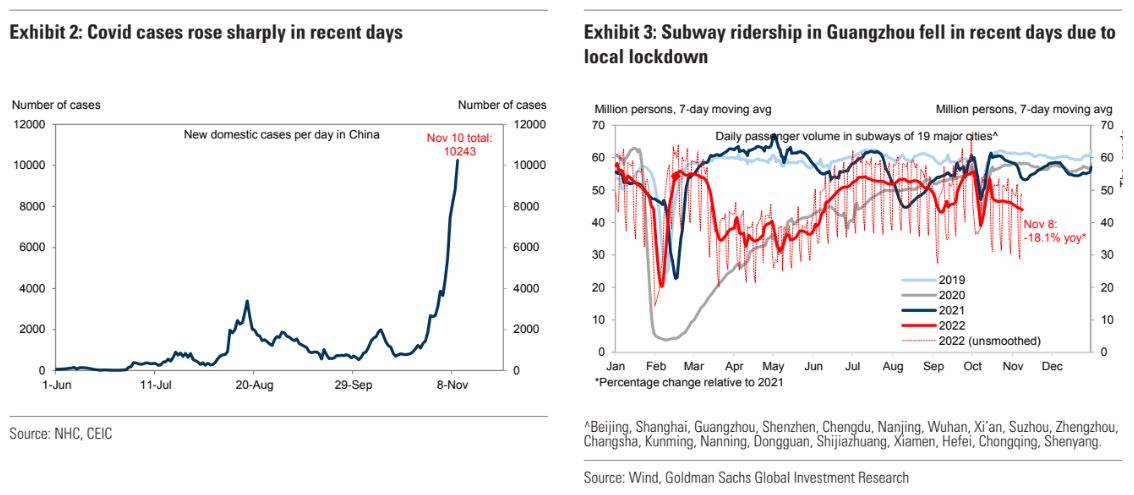

We’re going to see a test in short order of how much of this is finessing zero-COVID versus an end to zero-COVID on any useful timeline. Goldman:

Despite the fine-tuning in Covid control measures today, policymakers reiterated their stance to “firmly stick to the dynamic zero-Covid policy”, and acknowledged the risk that“Covid resurgence could escalate further”, especially in the middle of the winter flus eason and when the Lunar New Year travel season begins in two months. As discussed previously, we expect the central government would need local officials to stay vigilant on Covid control until the country has done all the required medical preparations (e.g.,vaccinating its elderly population, stockpiling Covid pills, and expanding medical facilities)as well as communication preparations (e.g., alleviating fears of Covid infections among the population). Although we see the rationale in lifting restrictions such as requiring residents to do multiple PCR tests within a day, the impact of such changes on domestic economic activity is likely to be limited as long as the zero-Covid policy remains.

Advertisement

In short, China is going to have to lock down a bunch of tier-one cities soon or its plague is going to escape the noose and the zero-COVID reopening will turn chaotic. I can’t see the PRC going for that.

Conversely, it has also launched its 16-point plan to rescue realty which is going to breath life into commodity restocking for a while, whether it actually works or not.

So, two scenarios are present. The first is that China does accelerate into reopening (controlled or chaotic) and a restock of many things, especially commodities, gets underway.

Advertisement

This will be clearly inflationary, very much so as oil follows on. So, it will mitigate against the Fed slowing its hiking campaign quickly. US inflation is slowing but it’s not slow!

Or, China remains committed to zero-COVID and reopening in 2023 will be slow and painful and not very supportive of global growth.

Either way, once past this furious short-squeeze, I still don’t see the end of the bear market in stocks, bonds, and the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.