By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The Wage Price Index (WPI) rose by 1.0%/qtr in Q3 22 and the annual rate stepped up to 3.1%.

- Private sector wages grew by 1.2% while public sector wages rose by 0.6% over the quarter.

- The WPI including bonuses picked up through the year to 3.8% (from 3.1%).

- The WPI today was consistent with our internal data – Australia is not facing a wage price spiral like in other jurisdictions.

- Our call for the RBA is unchanged – we expect one further 25bp rate hike in December that would take the cash rate to 3.10%, which we believe will be the peak in this cycle (the risk sits with a higher cash rate of 3.35%).

- The focus now shifts to the October labour force survey which will be published tomorrow (17/11)

Wages pressures emerge but are consistent with the RBA’s inflation target

The 1.0%/qtr increase in the WPI over Q3 22 was a touch stronger than our pick and the consensus call of 0.9% today. The annual rate stepped up from 2.6% in Q2 22 to 3.1%. The annual pace of wages growth rose above 3.0% for the first time since Q1 13.

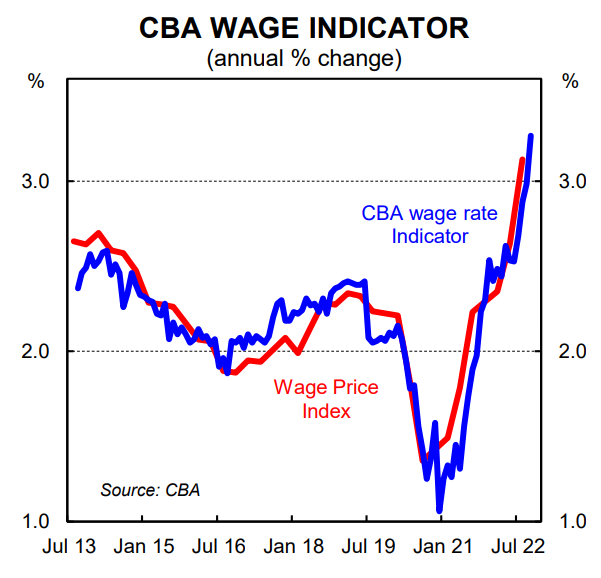

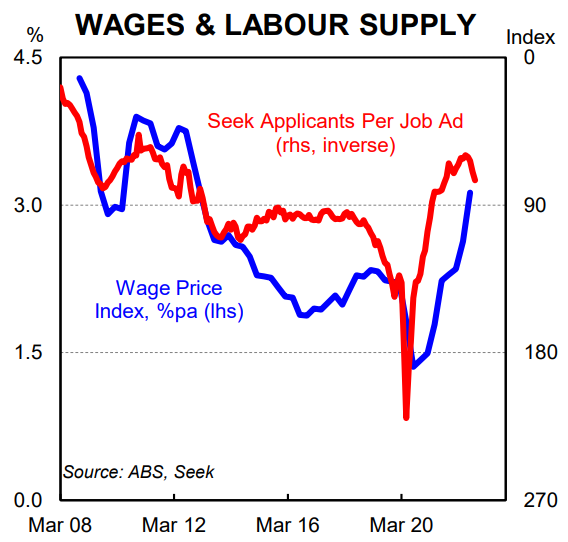

Despite the slight miss, the print today was broadly in line with our internal data which very accurately maps the WPI (see facing chart). It indicates wages pressures in the economy have taken time to emerge given the tightness in the labour market. But they have clearly materialised.

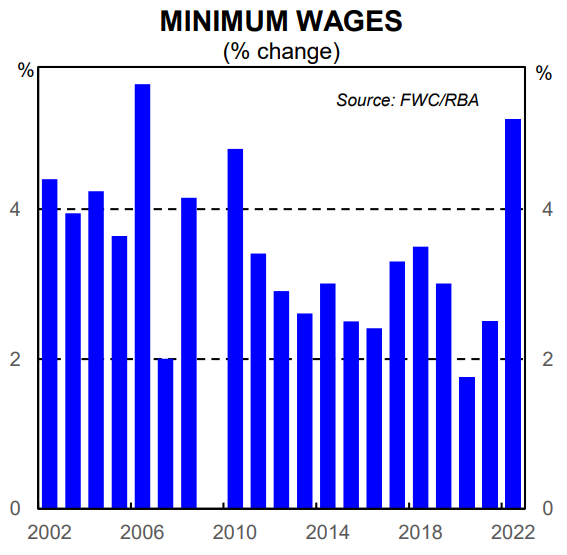

Context is very important when analysing today’s wages publication. The labour market was at its peak tightness over the September quarter. The big lift in the Annual Wage Review of between 4.6% and 5.2% by the Fair Work Commission was handed down. The flow of migrants and foreign workers had only just started to lift from a suppressed level. And the RBA’s rapid and aggressive rate hikes had not had any time to impact spending and by extension the demand for labour.

In short it was the ideal time for a worker to get a pay rise. And most of the action around pay adjustments each financial year in Australia occurs in the September quarter. With that backdrop in mind a 1.0%/qtr lift in wages over Q3 22 is welcome news rather than cause for concern.

Australia is not facing a wage price spiral like has been observed in other jurisdictions, notably the US (mainly due to differences in the supply of labour during the pandemic period and some institutional features of the wage setting process in Australia).

Wages growth has finally approached the desired levels. The RBA welcomes a lift in annual wages growth to 3.5-3.75% as that is consistent with the inflation target of 2-3%. It is worth noting that the RBA has forecast wages growth, as measured by the WPI, to reach 3.9% by end-2023.

The quarterly increase today annualises to ~4.0% which is a little above the optimal level for wages growth to settle. But the bigger than usual lift in the Annual Wage Review boosted the quarterly rate. In addition bargaining conditions for workers will not improve from here as the economy slows in 2023 due to the significant amount of monetary policy tightening put through by the RBA. On our forecast profile the unemployment will gradually rise over 2023. As that occurs it will be tougher for workers to push for bigger increases in salary, particularly as labour supply rises with the return of foreign workers.

We expect annual wages growth to continue to climb over 2023. But our expectation for the quarterly prints to be ~0.9% means we expect wages growth to remain at levels consistent with the inflation target.

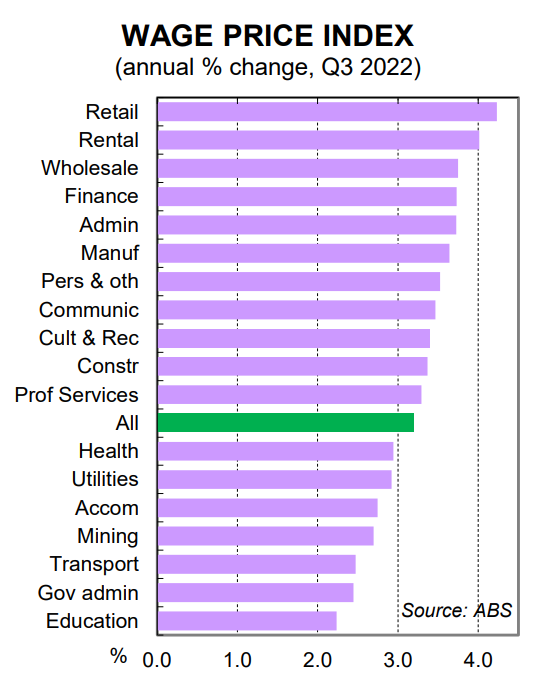

The strength in the wages data today came from the private sector. The 1.2%/qtr increase in private sector wages was strong. The ABS notes that, “the average size of hourly wage rises for private sector jobs recording a wage movement increased to 4.3%, up from 2.9% the same time last year.”

The increase in the minimum wage helped push private sector wages higher. According to the ABS this was most apparent in retail trade, administrative and support services, accommodation and food services, public administration and safety and health care and social assistance industries.

In contrast public sector wages increased by 0.6%. Wage increases for public servants have been held down by long standing wages caps. Many of these are currently now being revised.

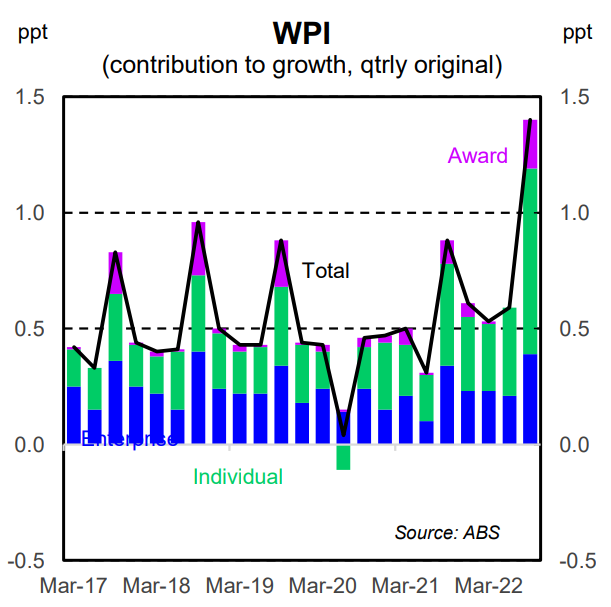

The WPI including bonuses stepped up through the year to a solid 3.8% (from 3.1% in Q2 22). The data is not seasonally adjusted so we don’t focus on the quarterly read and it is the annual rate that matters. It appears that some firms are making greater use of bonuses and discretionary payments rather than adjusting base pay upwards. Such an approach avoids ‘locking in’ higher pay.

This is very important when considering the outlook for inflation. Firms that have used bonuses and other one off payments to reward, retain and attract workers rather than upwardly adjusting base pay have not had a permanent upward adjustment in input costs. As demand in the economy slows these payments can be wound back. A wage price spiral occurs when base pay is resetting upwards in line with inflation, not when greater use of discretionary payments are made when the economy has boomed, as has been the case in 2022.

The WPI has its limitations. And it is not the only measure of labour costs. But the WPI is still the benchmark for wages growth in Australia. It enables us to better understand what is occurring across the economy with respect to wages inflation in a way that most of the other survey measures of labour costs do not (they are influenced by changes in superannuation, headcount, hours worked, absenteeism, job shifting, promotions and discretionary payments).

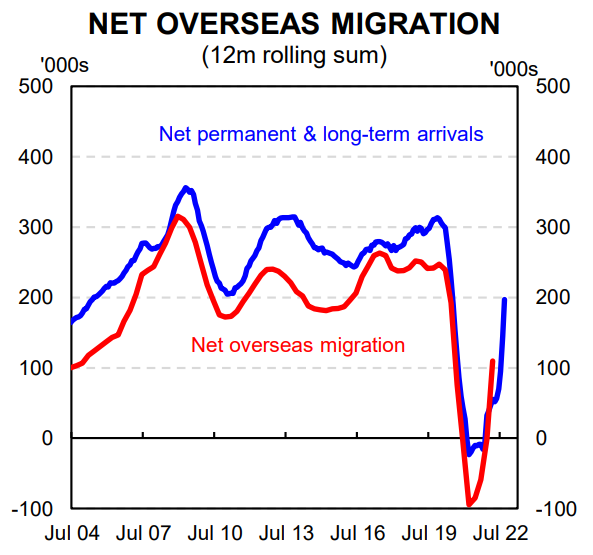

We are confident that we are past the peak tightness in the labour market. Most of the key job vacancy measures have retraced from their cyclical peaks. And according to Seek job applications per advertisement have risen over the past few months (see facing chart). The increase in applicants per job makes sense given the significant lift in long term and permanent arrivals over recent months.

Our RBA call is unchanged. We expect one further 25bp rate hike in December that would take the cash rate to 3.10%, which we believe will be the peak in this cycle (the risk sits with a higher cash rate of 3.35%).

It is worth highlighting what the RBA said about wages in the November Board Minutes – “So far, medium-term inflation expectations and wages growth remained consistent with inflation returning to target …. “Members noted that wages growth had not reached levels that would be inconsistent with the inflation target. While future trends were uncertain, wages growth remained below that in a number of other advanced economies”.

The data today will not shift the RBA’s thinking on wages growth. The data is broadly in line with their expectations (their implied profile was likely centred on a quarterly increase of 0.9% in Q3 22 so the miss is not significant).