DXY rebounded last night as the Fed rug pull began:

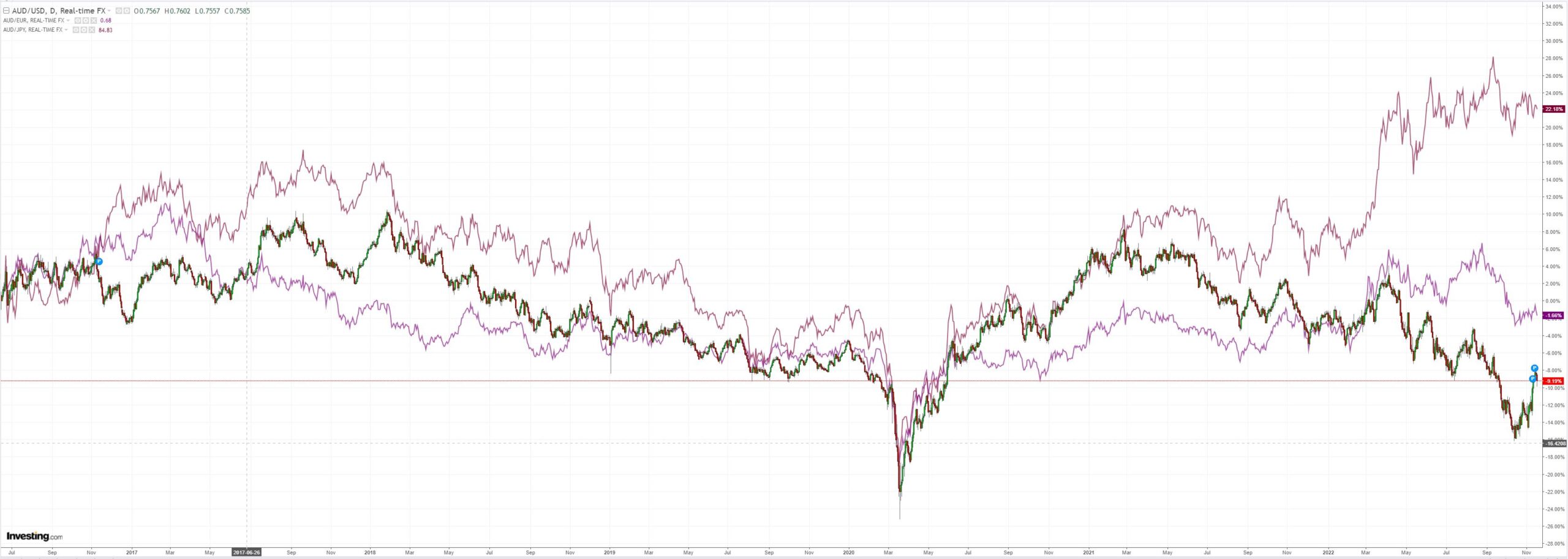

AUD bashed:

Oil is ignoring China:

Advertisement

Base metals rolled:

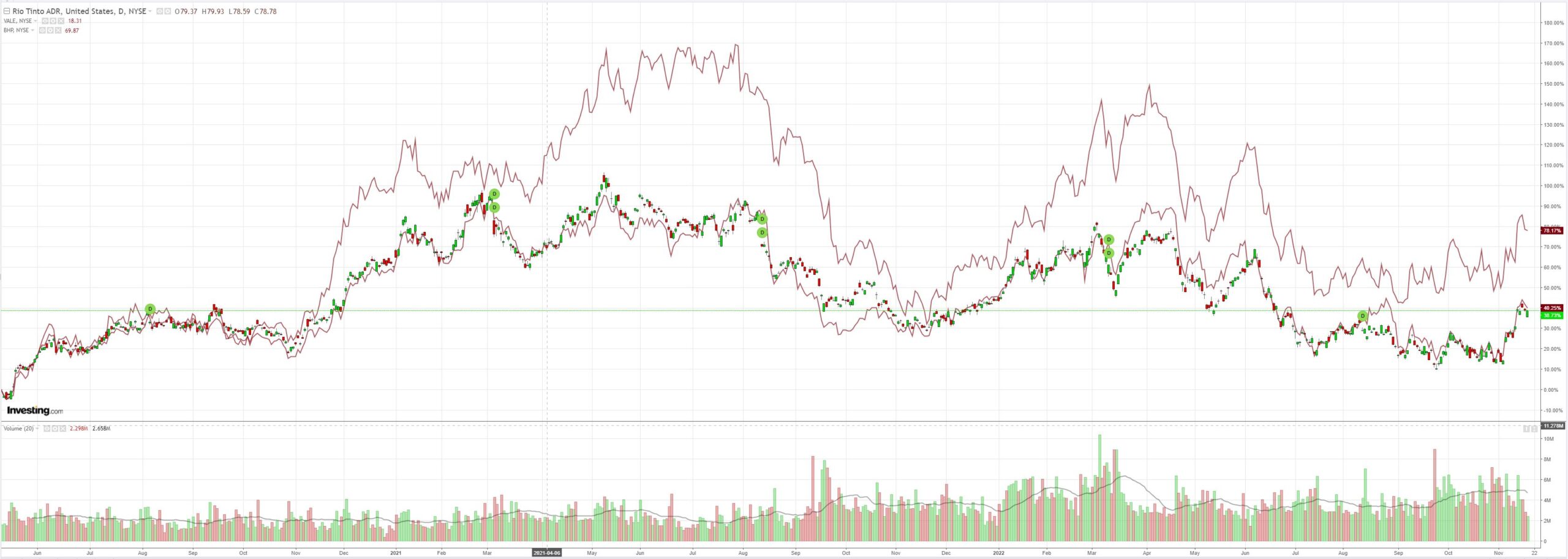

Big miners too:

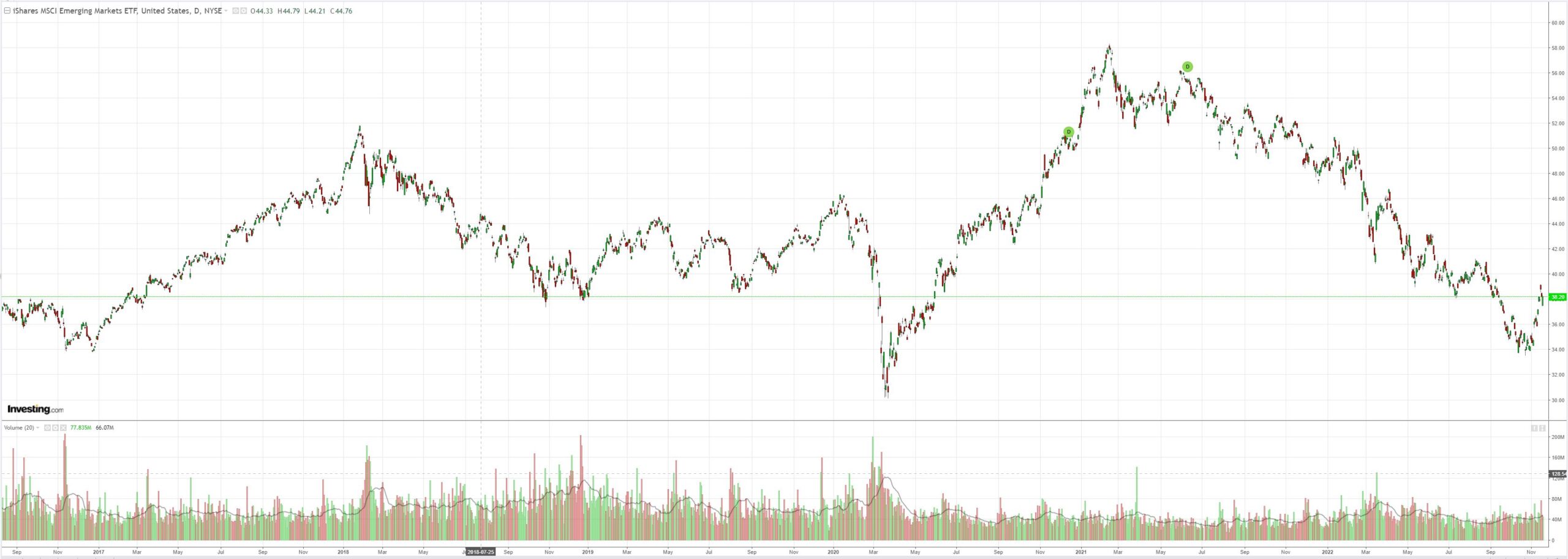

EM cracked:

Advertisement

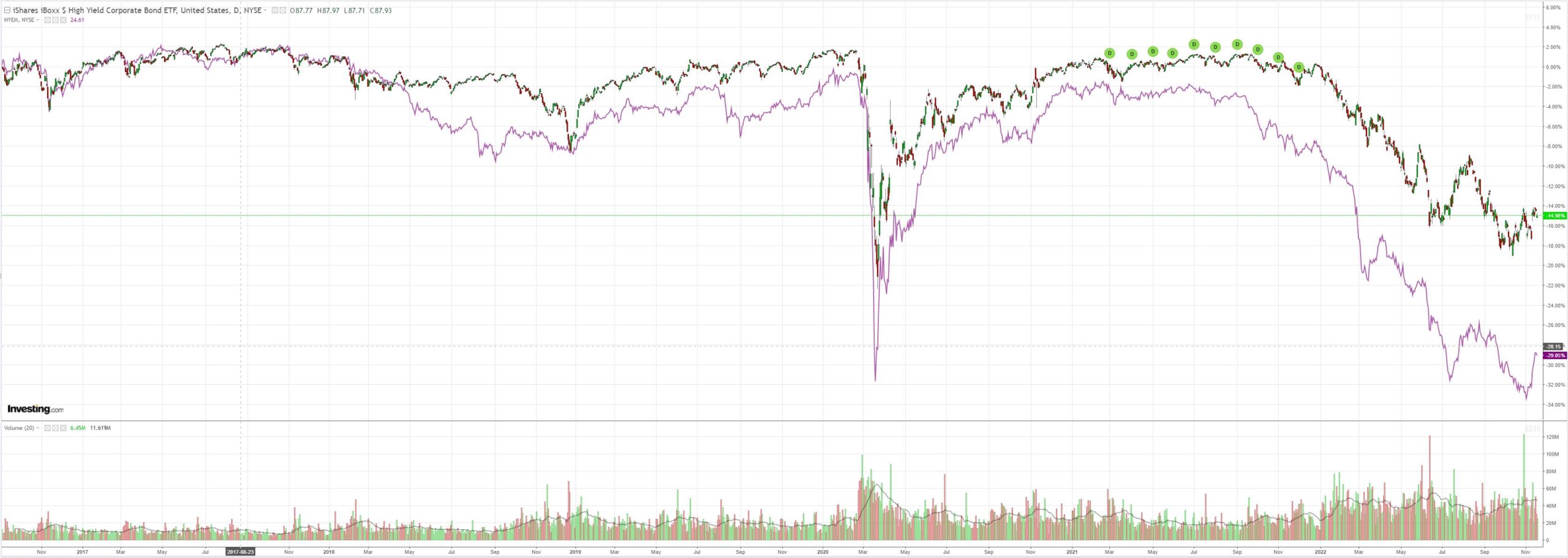

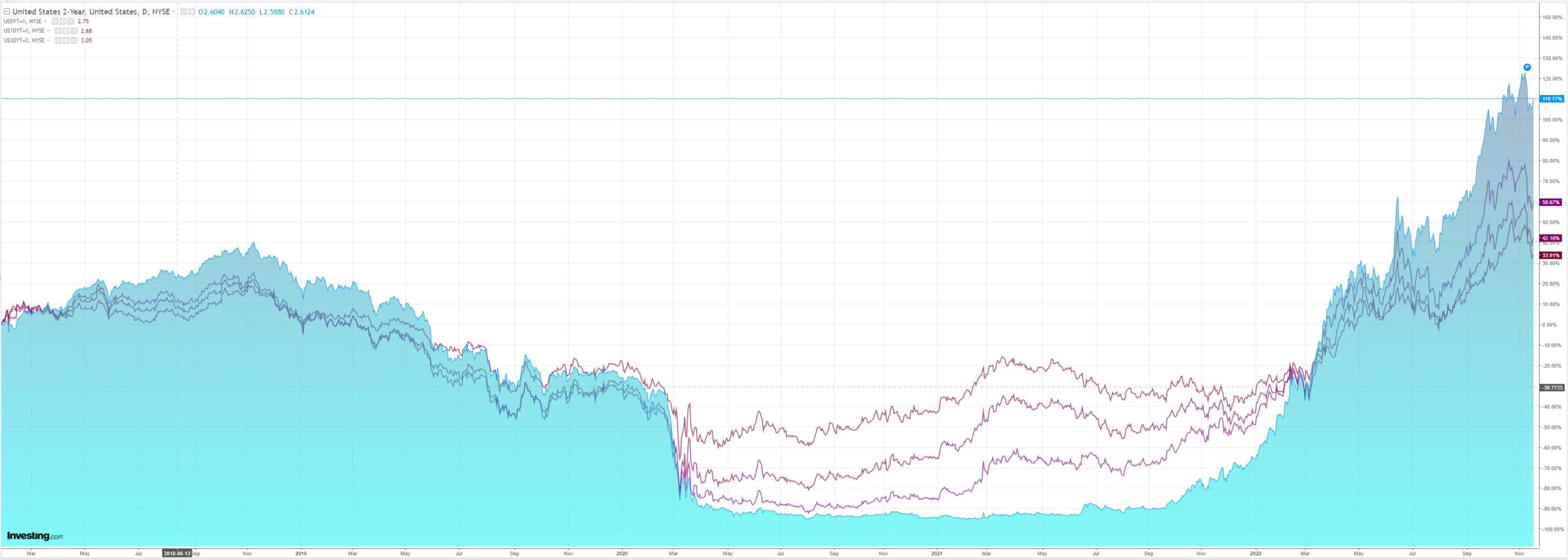

The Treasury curve inversion just keeps getting worse:

Stocks were hit:

There may be a little more juice in this bear market rally lemon but not much. James Bullard wrecked it:

Advertisement

Even under a “generous” analysis of monetary policy, the Federal Reserve needs to keep raising interest rates given that its tightening so far “had only limited effects on observed inflation,” St. Louis Fed President James Bullard said on Thursday.

Bullard said the Fed’s target policy needs to rise to at least a range between 5.00% and 5.25% from the current level of just below 4.00% to be “sufficiently restrictive” to curb inflation, though he would defer to Fed Chair Jerome Powell regarding how much higher to move rates at upcoming policy meetings.

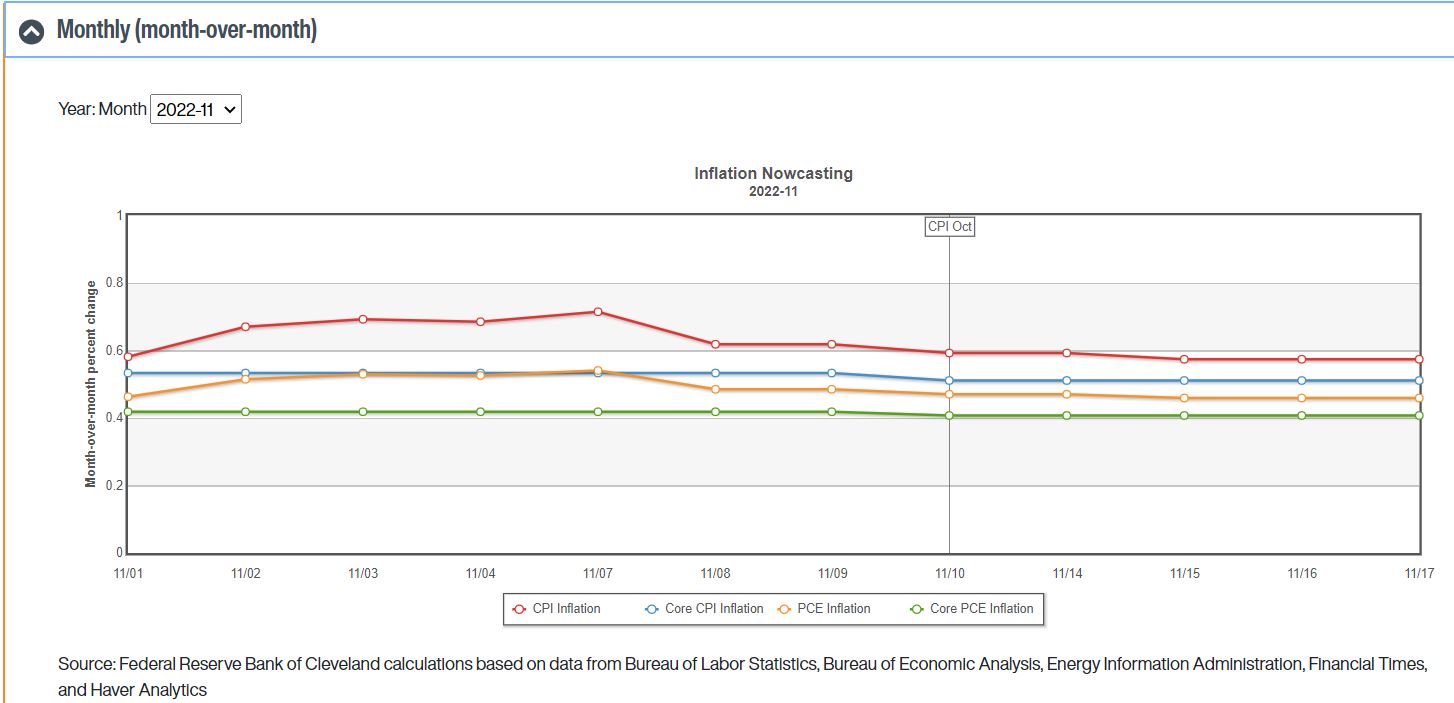

The Fed’s inflation nowcast for CorePCE is unmoved:

Nomura’s Charlie McElligott sums it all well:

Advertisement

Looks like a lot of the de-grossing is done, and that some folks are actually again emboldened to lay those key cogs of the 2022 legacy “FCI Tightening” trades back out thereafter their recent repricing(having gotten their doors blown-off in the ‘momentum shock’ trend-trade unwind this past week), with US Dollar again rallying near HOTD as I type,while USTs and Equities are simultaneously fading weaker and reversing earlier overnight gains.

At the core of the “reversal of the reversal” is the chief “FCI Tightening” proxy US Dollar again firming after surprisingly strong US data yesterday, in addition to almost certaintactical profit-taking from “renter” Longs in G10 pairs and Chinese Yuan—where Hoe Lon Leng notes that there is abunch of restocking in USDCNH Upside(like 7.30 strikestuff)as a preferred as tail-hedge that carries well(FWIW, also been seeing people monetize large chunks of their FXI / KWEB / ASHR Upside the past two days, selling out ofCalls / Call Spreads).

The resilience of the US economic data sits at the core of this renewed confidence in taking some shots again on “FCI tightening” trades, as we see the Bloomberg USEconomic Surprise index reaching highs last seen in mid-May ’22, as data continues to beat expectations on the margin—Labor, Retail / Wholesale and Surveys / Biz CycleIndicators bearing the concentration of the gains(while Housing, Industrials and Personal / Household sectors continue to drag)…”Good (data) is Bad (for assets)”…

In my mind, it all keeps coming-back to this recent NY Fed research paper concept of R* (neutral rate for the real economy) simply sitting in a totally different universe from R**(neutral rate for financial stability)…It now seems abundantly clear that “markets” cannot handle much more rate hiking after a decade + of duration- and leverage-binging, as evidenced by the list of “market breakages” experienced over the past 12 months…but in the meantime, the real US economy(admittedly outside of Housing and structurally-shrinking Manufacturing sector)keeps banging along, where in peak (cringe) anecdotal fashion, restaurant ressies are “no offer,” luxury malls like Short Hills are packed with lines out of some of the most high-end retailers doors, airports are foaming at the mouth and airline tickets are running 2-3x’s ‘sanity levels,’ there is no locate on new Range Rovers in New Jersey until 2024….and all while New Yorkers are apparently lifting $21k Taylor Swift tickets for next Summer.

And this is why “High for Longer” continues to persist (Fed “Terminal” projections back to 4.99% this morning—but our house view is that it’s gonnahave to push through 5.50-5.75, while GS took their Fed projection up yday as well)…it’s the same thing: the Inflation is going to soften down to 4-5% on pure base-effect math—but it’s not going to head back to 2% target if you don’t see actual job losses mount…bc right now, Labor and Wage gains are just too strong (hot off the press this morning:https://abc7ny.com/nyc-minimum-wage-restaurant-delivery-workers-grubhub/12461113/).

Right on message:

Fed’s Bullard Says More Hikes Needed to Get to Restrictive Levelo Policy rules that he presents show 5%-7% restrictive rates

Tightening has had limited effect on inflation so far, he says Turning back to market,it certainly seems like people are taking off some of their US Equities “risk rentals”which have rallied so violently over the past week since the CPIdownside surprise…and thematically, have even begun to lay back into their Shorts in all the trash that exploded 20% over the week–hence, US Equities Long Term Momentum factor +3.1% and Low Risk factor +3.0% again yday, respectively,as they feel the recent move has “overshot” particularly on the “expensive” /“unprofitable” stuffEquities still feel fragile.

The “sign of possible regime change” I highlighted in the last note—where US Equities Index Option Skew has steepened for 5 out of the past 6 days while Stocks violently rallied, standing in stark contrast to the perpetual flattening in Skew to 0%ile over the course of 2022 YTD—I believe has been a function of folks actually needing to hedge again, because they were starting to actually put on some exposure again after this violent “force-in” rally that very few people actually wanted to happen.

And also as previously mentioned in recent weeks, my spidey senses too have been tingling with thispersistent VIX Upside being sought for 6 consecutive weeks in size,most of it “wingy” / “crash” stuffSo all of this said,yday was a stark reminder of the power of the longer-term YTD legacy US Eq Vol regime—Spot down, Vol down, Skew flatter and Vol of Vol absolutely RINSED—as old habits die hard,especially with the coincidental year-end timing ahead of the Holidays and World Cup…incentivizing further de-risking before the liquidity andbalance-sheet deployment “goes to zero”Index Options positioning is now too “closer to home” after the recent “Put destruction / Call grab” bonanza—US Equities (positive) $Delta impulse across SPXSPY, QQQ andIWM now is up to 77%ile since 2013after having sat near 1%ile just a month ago (up +$600B from 1 week ago—how’s that for rocket fuel).

But as we see Spot selloff this morning, we now see SPX back at “Gamma Flip” level as we speak (3918),while both QQQ and IWM have pushed back into “Short Gamma” territory.

Beautifully put. I will only add that the distinction between r* and r** can hold only so long as consumers don’t pay attention to asset prices, supported by the stimulus tail and rising wages.

But they, too, are conditioned by several decades of credit excess (in Australia at least) and it is only a matter of time before the two r*s converge.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.