Westpac with the note.

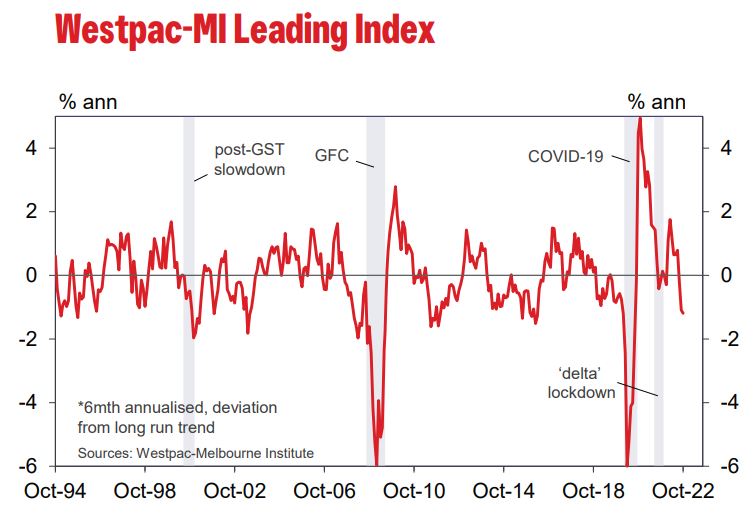

- Growth rate falls to new post-pandemic low of –1.19%.

- Signal consistent with sustained weak growth in 2023.

- Key drivers of the slowdown are: monetary policy tightening; falling commodity prices; and softness in jobs growth as capacity constraints bite.

As the growth rate continues to fall – albeit at a much slower pace than we saw last month – we continue to get further support from the Leading Index that growth will slow substantially in 2023.

Westpac has been of the view that growth will slow from around 3.4% in 2022 to 1% in 2023. The Reserve Bank recently moved their own growth forecast for 2023 more into line with our own view – from 1.8% to 1.4%.

The Leading Index growth rate has seen a sharp turnaround over the last six months, going from running 1.19% above trend in April to 1.19% below trend in October. Three components account for the 2.38ppt swing: the yield spread, which has seen sharp narrowing as policy tightening has driven up short term rates (–0.93ppts); commodity prices, which have seen a significant reversal in AUD terms (–0.89ppts); and aggregate monthly hours worked, which have seen a clear moderation as post-COVID reopening runs its course (–0.58ppts).

Significant drags from other components (US industrial production, –0.19ppts; and the S&P/ASX 200, –0.19ppts) have been ‘neutralised’ by a stabilisation in dwelling approvals (adding +0.27ppts) and a slight improvement in the Westpac-MI Unemployment Expectations index (+0.12ppts). That said, neither of these last two supports looks particularly convincing with both dwelling approvals and consumers’ labour market confidence looking set for a further deterioration in coming months. Consumer sentiment more generally – captured by the Westpac-MI Consumer Expectations Index component – remains extremely weak but is relatively unchanged since mid-year, having a neutral impact on the leading index growth rate (+0.01ppts).

The Reserve Bank Board next meets on December 6. We expect that the Board will decide to raise the cash rate by a further 0.25%.

The Reserve Bank lifted its forecast for underlying inflation from 6.0% to 6.5% in response to the surprise lift in the level and breadth of inflation we saw in the September inflation report. Additional other factors, including electricity prices, have also led the Bank to lift inflation forecasts for 2023 from 4.3% to 4.7% while it now does not forecast getting inflation into the 2–3% band until 2025.

Despite this deteriorating inflation outlook, the minutes to the September meeting hint at a more dovish approach going forward. Westpac expects that a mooted pause in the tightening is unlikely to occur in 2022 or the early months of 2023 as the Bank continues to underperform its inflation objectives.

Inflation in Australia in 2022 is now forecast to exceed that in both the US and Canada, casting doubt on the RBA’s assessment that ‘Australia is different’.