Roy Morgan Research has modelled the direct impact of the existing 2.75% lift in the Official Cash Rate (OCR), as well as a further expected rate increase in December.

This modelling estimates that over one quarter of Aussie mortgage holders would be classified as ‘At Risk’, define as their mortgage repayments being greater than a certain percentage of household income (i.e. 25% to 45% depending on income and spending).

This would be the highest share of mortgage stressed households since June 2012.

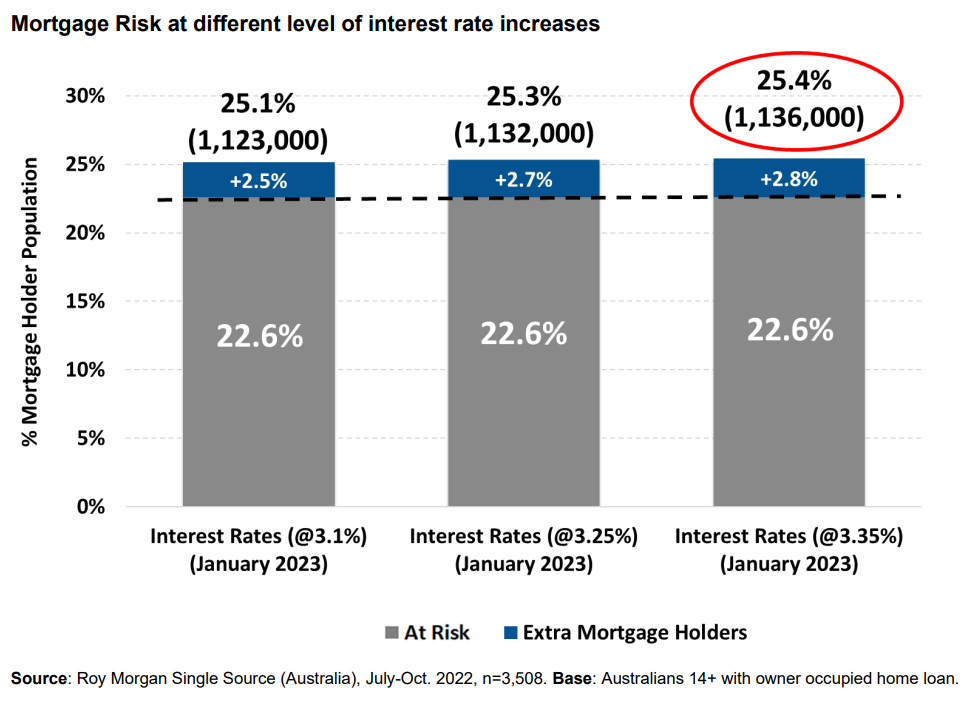

Specifically, Roy Morgan has modelled the impact of three potential interest rate increases in December of +0.25% to 3.1%, +0.4% to 3.25% and +0.5% to 3.35% and projected how these different sized increases would impact the number of mortgage holders that would be considered ‘At Risk’ by January 2023.

If the RBA raises interest rates by +0.25% in December to 3.1% there will be 25.1% (up 2.5% points) of mortgage holders, 1,123,000, considered ‘At Risk’ in January 2023 – an increase of 110,000.

If the RBA raises interest rates by +0.40% in December to 3.25% there will be 25.3% (up 2.7% points) of mortgage holders, 1,132,000, considered ‘At Risk’ in January 2023– an increase of 119,000.

If the RBA raises interest rates by +0.50% in December to 3.35% there will be 25.4% (up 2.8% points) of mortgage holders, 1,136,000, considered ‘At Risk’ in January 2023– an increase of 123,000.

Roy Morgan notes that this is a conservative model, essentially assuming all other factors remain the same. And that the greatest impact on a household’s ability to pay their mortgage is not interest rates, but whether they lose their job or main source of income.

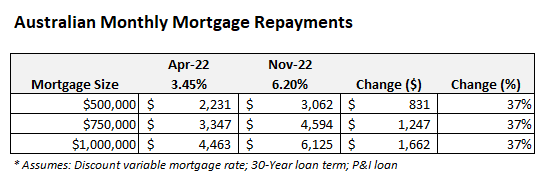

As illustrated in the next table, average variable mortgage repayments have already lifted by 37% versus their level in April immediately prior to the RBA’s first rate hike:

For a borrower with a $500,000 variable mortgage, this represents an $831 increase in monthly mortgage repayments.

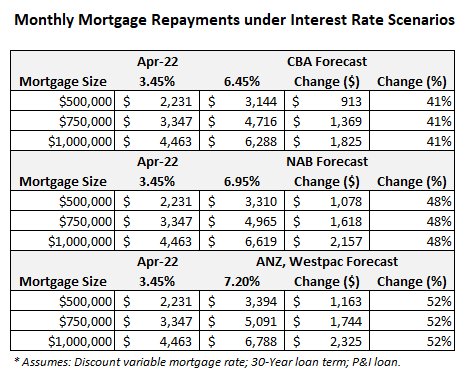

Opinion is divided on the RBA’s moves after December’s expected 0.25% hike. For example, the CBA expects the RBA to remain on hold, whereas NAB expects another 0.5% of tightening, and ANZ and Westpac another 0.75% of hikes.

The below table shows how much variable mortgage repayments would rise if the big four banks’ interest rate forecasts were to come to fruition:

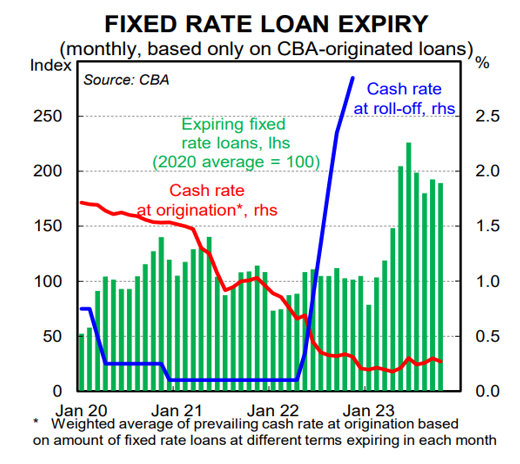

Moreover, roughly 40% of mortgages taken out over the pandemic were fixed at rock bottom rates of around 2.0% to 2.25%. A huge share of these mortgages will expire over the next year and will reset to roughly double or triple mortgage rates, which will push many more mortgage holders into stress.

Given the sheer size of recently underwritten mortgages, it is inevitable that many borrowers will fall into stress given the steepest lift in mortgage rates in this nation’s history.