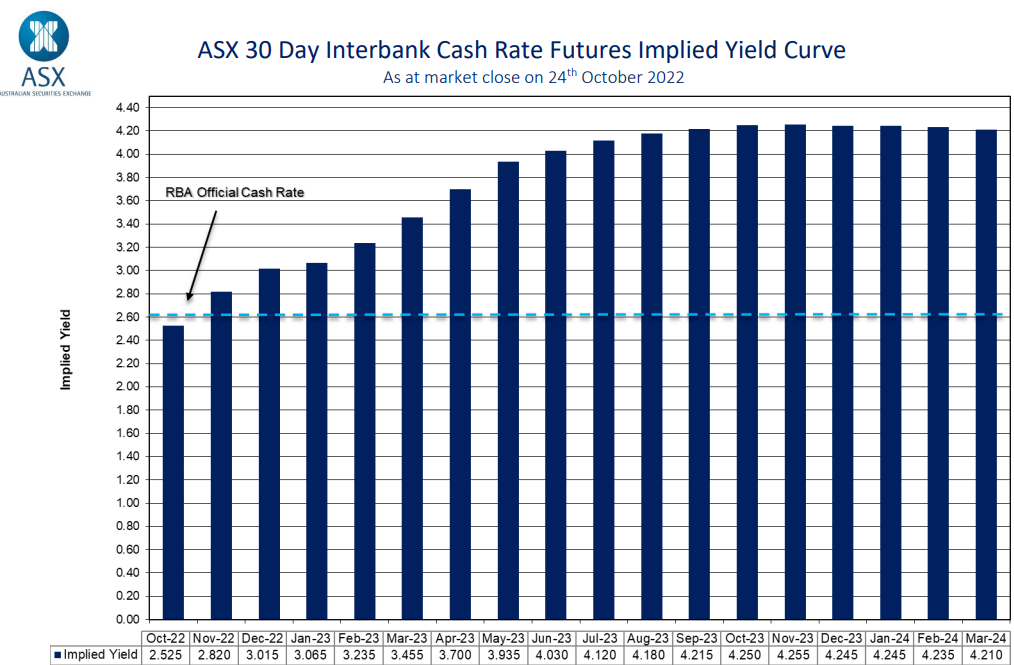

Late last month, the futures market was tipping that the Reserve Bank of Australia (RBA) would lift the official cash rate (OCR) to a peak of 4.25% by October 2023:

October 24: OCR tipped to peak at 4.25%.

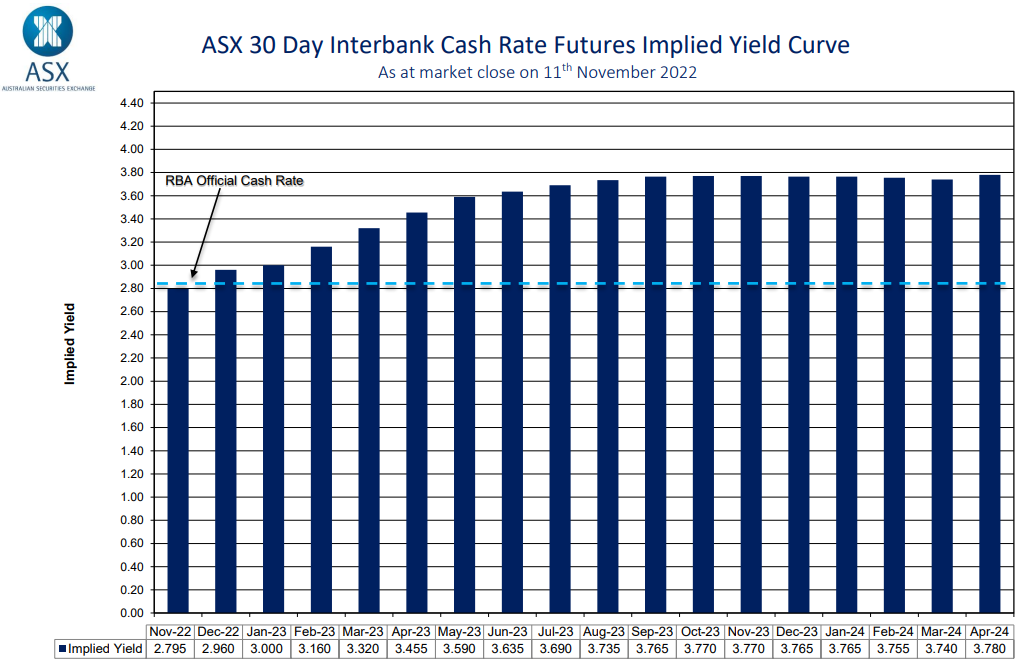

RBA deputy governor Michele Bullock on Wednesday delivered a speech in Sydney whereby she indicated that the RBA was unlikely to follow the US Federal Reserve’s “scorched earth” monetary tightening, noting the RBA has “a flexible inflation target for a reason”:

“You could scorch the earth and get inflation back down very quickly – is that the right thing to do? Or is it better to try and preserve some of the gains while you bring it back down?”

Bullock then appeared before a post-budget Senate estimates committee on Thursday, whereby she suggested that the RBA would soon pause its rate tightening.

Specifically, Bullock stated the RBA was approaching the point where “maybe there might be an opportunity to sit and wait and look a little bit”.

These comments were interpreted by financial markets as ‘dovish’, and resulted in a sharp circa 0.5% downgrade in the expected OCR to a peak of around 3.75% by September 2023:

November 11: OCR tipped to peak at 3.75%.

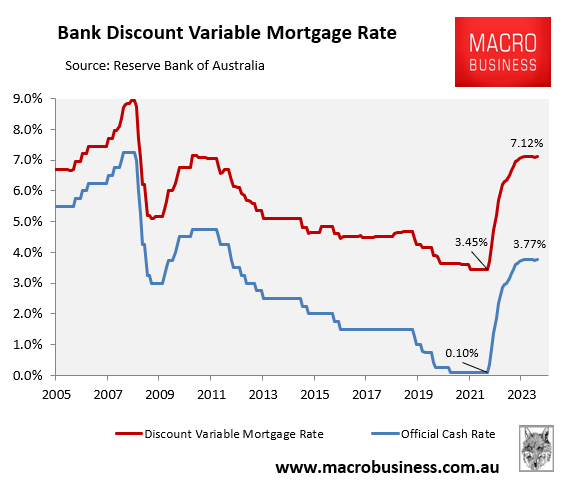

Based on the futures market’s latest OCR forecast, Australia’s discount variable mortgage rate would climb to around 7.10% by September 2023, which is more than double its 3.45% level in April 2022 immediately before the RBA’s first rate hike:

Variable mortgage rates to more than double.

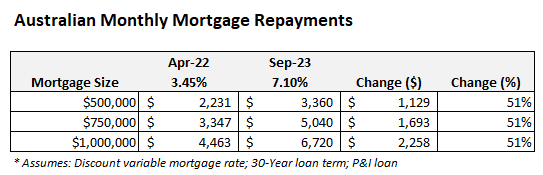

In turn, average variable mortgage repayments would rise around 50% above their pre-tightening level, adding over $1,100 in monthly repayments to a $500,000 mortgage:

The market’s revised interest rate expectations would still represent a hammer blow to mortgage holders and would likely send house prices sharply lower.

Household consumption and ergo economic growth would also take a sharp hit, especially given hundreds of billions of dollars worth of cheap fixed rate mortgages are set to be reset to double or triple mortgage rates next year.

Pass the popcorn!