Morgan Stanley with the note. I’m not sure why they don’t just come and say it. Prices are crashing month-on-month.

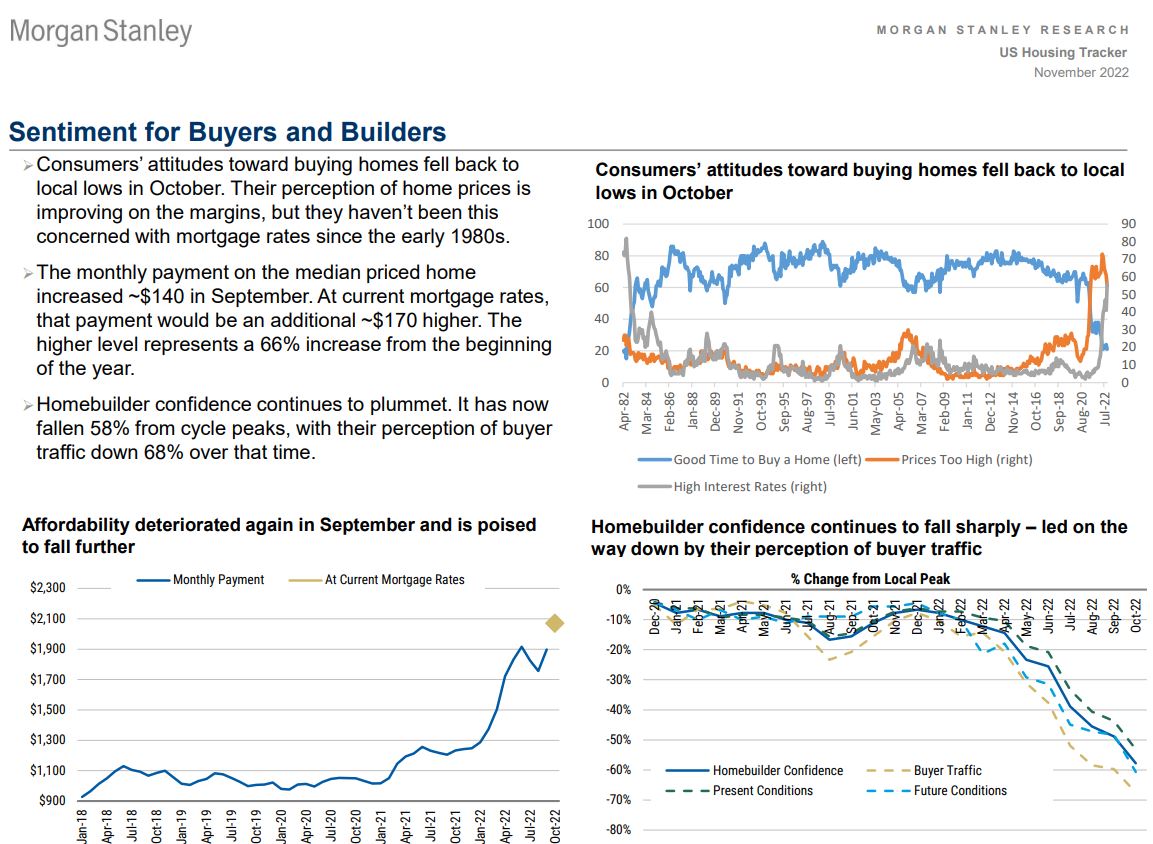

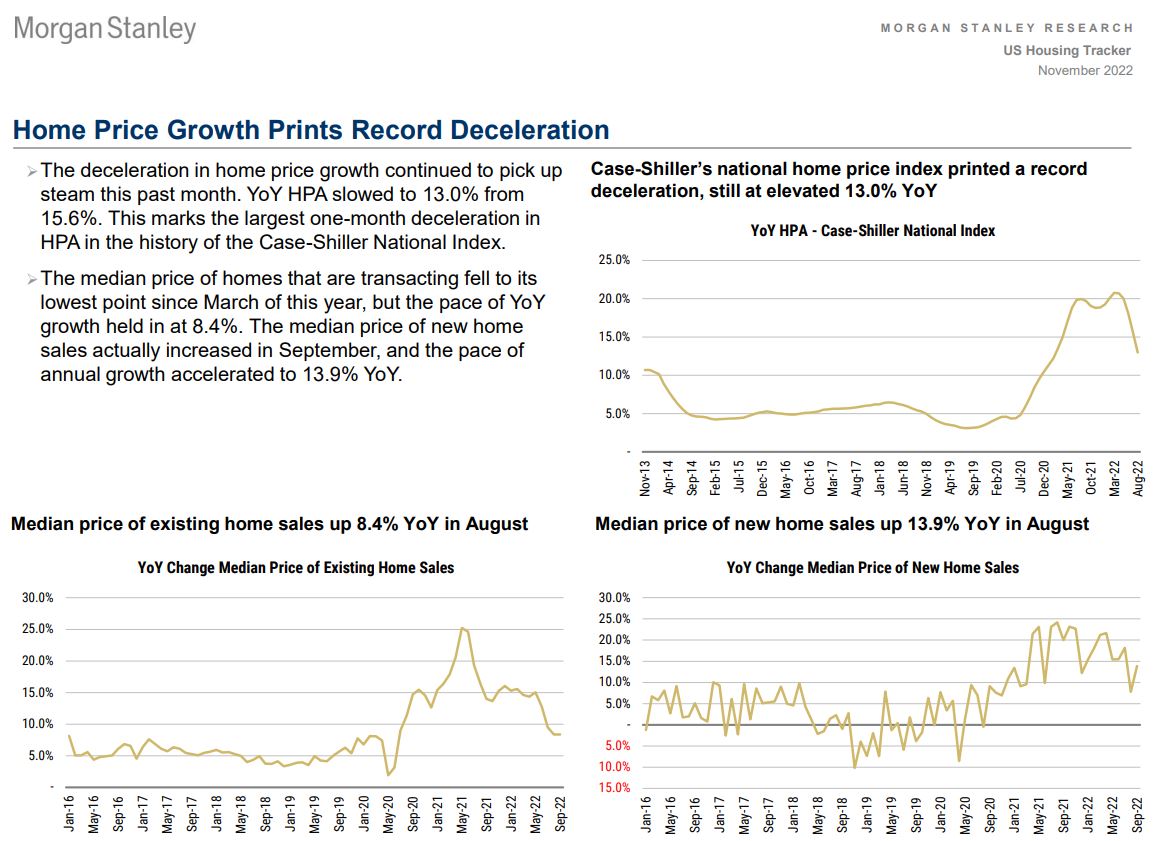

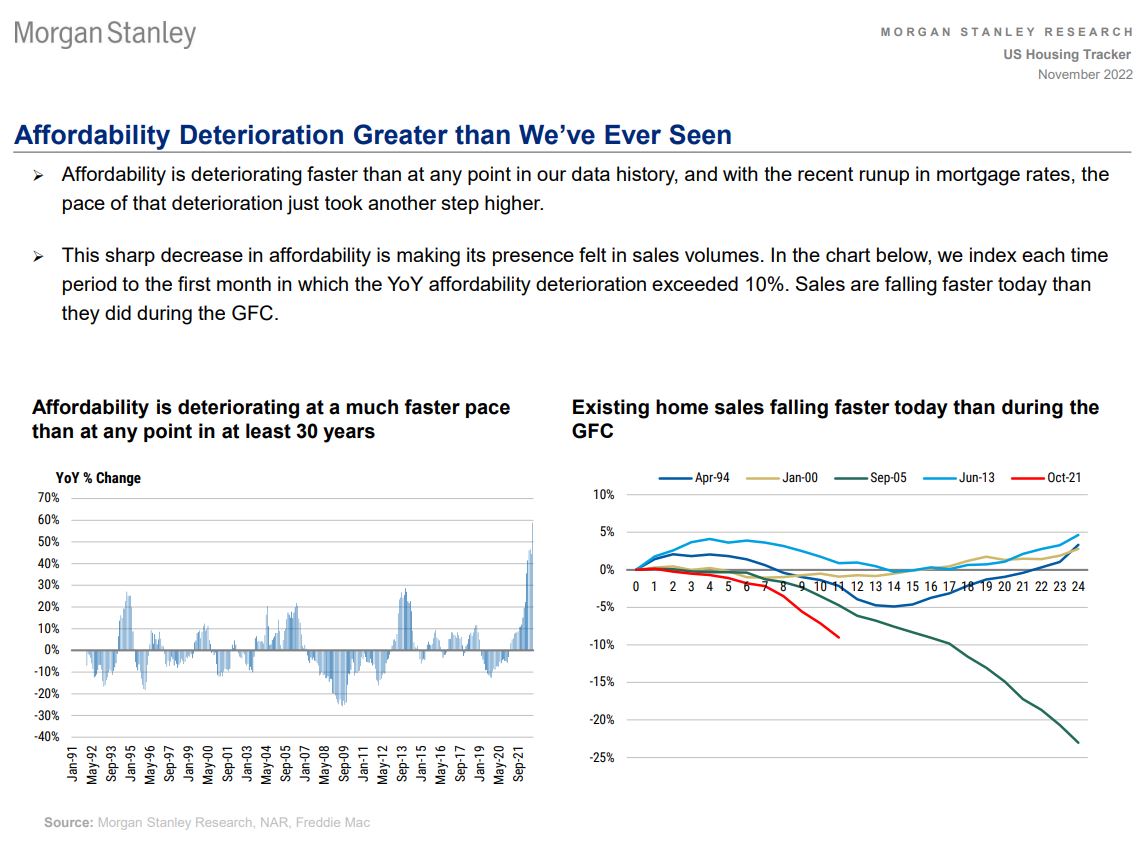

Home Price Growth Slows Meaningfully: YoY home price growth slowed to 13.0% in August from 15.6% in July. This drop in YoY HPA broke the record for the sharpest pace of deceleration that was set just one month ago. While home price growth has slowed, the continued increase in prices combined with the sharp back-up in mortgage rates have led to a renewed deterioration in affordability. The home price slowdown continues to become more geographically pervasive. The monthly payment on the median priced home increased ~$140 in September. At current mortgage rates, that payment would be an additional ~$170 higher. This higher level represents a 66% increase from the beginning of the year. All of the Case-Shiller 20 cities are now showing home prices falling month over month, up from 12 in July and 7 in June. We expect the pace of deceleration in YoY HPA to pick up once again, with our forecast for September YoY HPA to fall to 10.2% from this month’s 13.0% reading.

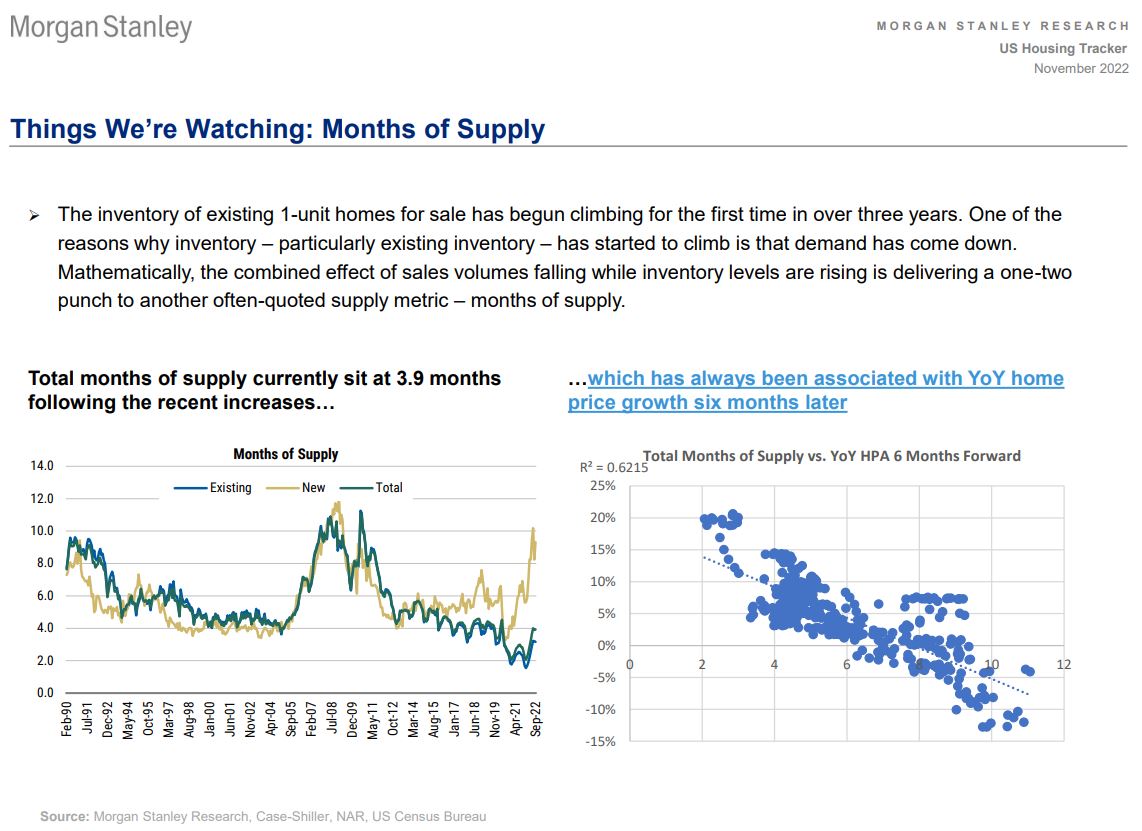

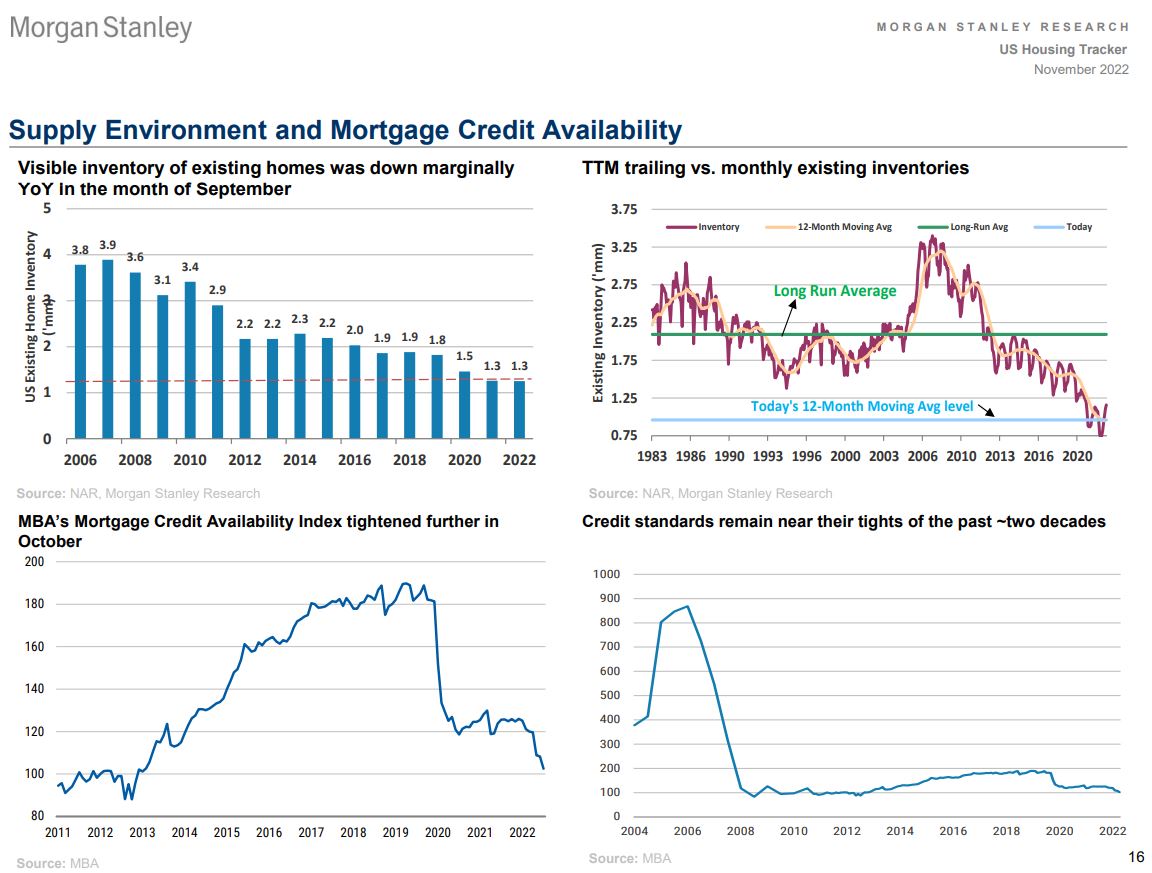

Demand and Supply: The increase in mortgage rates made itself apparent in sales volumes this month. Pending home sales plummeted, falling 24% MoM and 30% YoY to their weakest levels for September since 2010. Purchase applications continue to weaken each month and were down 40% YoY in October. Through 3Q, existing home sales are down 13% YTD while new home sales are down 14%. While supply is growing as demand dwindles, the pace of that growth continues to moderate and the absolute number of homes for sale remains close to its historical lows set earlier this year. We expect the pace of growth to remain slow as the lock-in effect keeps current homeowners in their homes. Total months of inventory remain in restrictive territory at just 3.9. Single-unit starts continue to drop as builder confidence declines, finishing 3Q 2022 18% lower than 3Q 2021. YTD, single-unit starts are down 6%. As the drop in starts has lengthened, the backlog of homes under construction has started to decrease, though at this point the declines are marginal, down 3% since May.