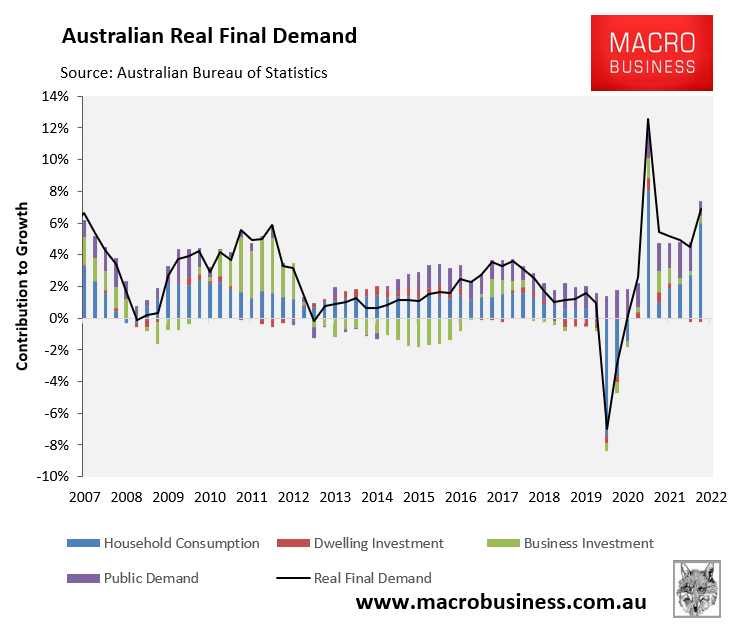

Last week’s Q3 national accounts showed that household consumption was the overwhelming driver of Australia’s economic growth, accounting for all of the nation’s 0.6% final demand over the quarter and nearly 90% of growth over the year:

Household consumption drove the economy in Q3.

Indeed, household consumption typically drives the economy, accounting for around 55% of final demand in a typical quarter. Thus, where household consumption goes, the economy usually follows:

Where household consumption goes, so does the economy.

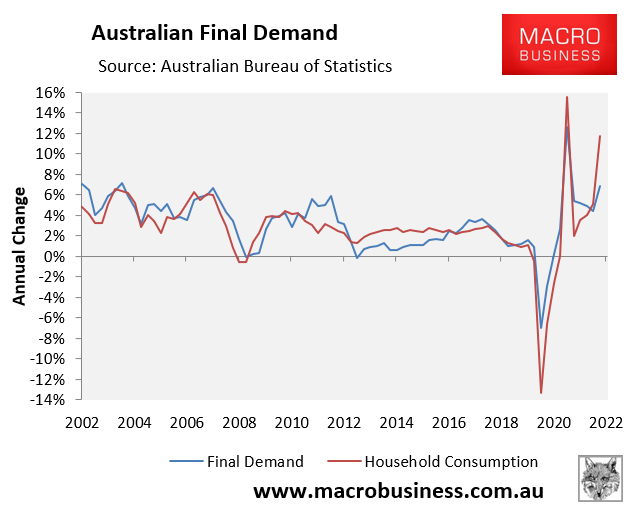

This presents a problem for 2023 given household consumption growth is already fading:

Household consumption growth fading.

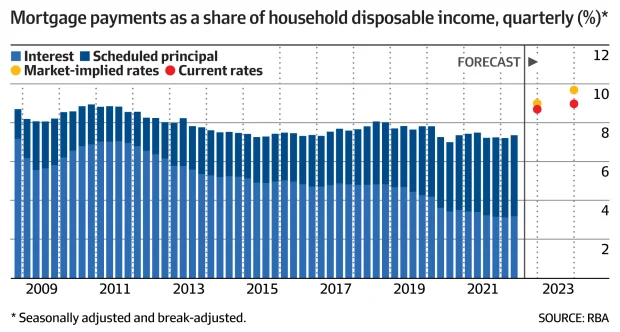

This is to be expected given the Reserve Bank of Australia (RBA) aggressive monetary tightening, which has delivered a 300 basis point rise in the official cash rate (OCR) in only seven Calender months – a record increase.

The latest Statement of Monetary Policy (SoMP) from the RBA noted that “housing mortgage payments were set to rise further in the period ahead” due to “the increase in home loan interest rates that had already occurred over the year” in addition to “the effect of fixed interest rate loans rolling off over time”.

As shown in the below chart from The AFR, aggregate mortgage repayments will rise to around 9% of household disposable income by the end of this year, beating the previous high recorded 12 years ago:

Australian principal and interest mortgage repayments to hit record by end 2022.

The big four banks’ current OCR forecasts are as follows:

- CBA: 3.35% by February 2023, then dropping to 2.85% by December 2023.

- NAB: 3.6% by March 2023, remaining steady into 2024.

- Westpac: 3.85% by May 2023, then dropping to 2.85% by November 2024.

- ANZ: 3.85% by May 2023, then dropping to 3.5% by November 2024.

Financial markets are also tipping a peak OCR of 3.6% by August 2023.

Therefore, based on these forecasts, the OCR will rise by between 0.25% and 0.75% from its current level of 3.1%.

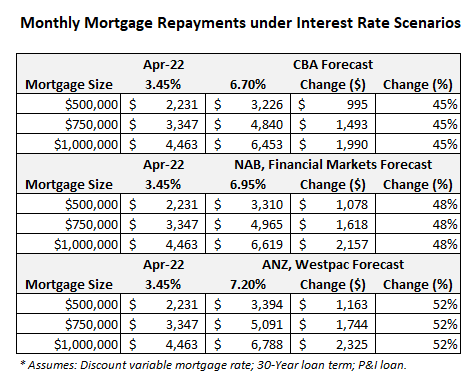

The impact on Australian mortgage holders from the above forecasts is illustrated in the below table, compared against interest rate settings in April 2022 immediately before the RBA’s first rate hike:

Depending on the OCR forecast, average variable mortgage repayments will rise by between 45% and 52% from their April 2022 pre-tightening level, adding between $995 and $1,163 in monthly repayments to a $500,000 mortgage.

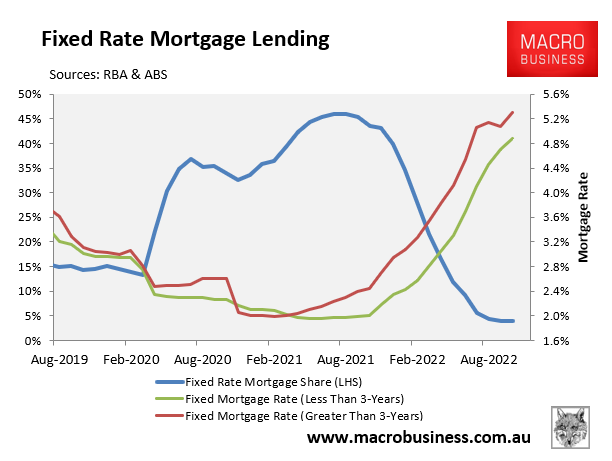

To add further insult to injury, the share of Aussie home buyers that took out fixed rate mortgages surged over the pandemic from a long-term average of around 15% to an all-time high 46% in mid-2021:

Fixed rate mortgage time bomb.

Nearly one-in-four mortgages (by value) will switch in 2023 from ultra-low fixed rates originated at around 2% to rates that are more than double these levels.

As a consequence, monetary conditions will tighten further in 2023 even without additional OCR hikes from the RBA.

The inevitable impact will be that household consumption will crater next year as more income is diverted away from spending towards debt repayments.

In turn, the Australian economy will slow to a crawl, driving the economy into a likely per capita recession.