Morgan Stanley with the note:

Tesla has shed $600bn of value in just 3 months. As the ‘ambassador’ of EVs, Tesla’s valuation raises questions for investment returns and capital formation across the sector. Is it time to consider alternative technological paths in addition to EVs? We view this as a buying opportunity, reit. OW.

A few thoughts on EVs heading into 2023…

1. Big auto blinking? It was far easier to take EV hegemony for granted at 0% Fed funds and when Tesla was a trillion $ company. Are we sure batteries are the only (or ultimate) path to decarbonizing transport? Is the technology cheap enough? Is our electric grid ready? Are the enabling policies viable? Stories like Porsche (covered by Harald Hendrikse) investing in eFuels as a ‘dual path’ / complementary technology to EVs is worth watching.

2. Deflation: Look for Tesla to use its cost and scale advantage as a competitive force. Tesla’s price cuts started in China and we expect them to quickly spread to Europe and the US. While circular in nature, lower EV prices are important for the next leg of mass adoption, but depress the returns of many of the companies expected to compete against Tesla.

3. Transparency: We anticipate Ford’s ‘Model e’ unit (to be disclosed 1Q23) will clearly display that legacy EVs are not profitable today. We believe Ford’s divisional re-organization may be an important moment for the industry in understanding the trade-offs of capital allocation and margin loss vs. terminal value preservation in legacy autos. While the intercompany transfer pricing and impact of government incentives may take a while to sift through, we expect a more open and balanced understanding of the risk/reward for EVs.

4. Respect: It’s time to recognize the wisdom of Toyota. Akio Toyoda, leader of the world’s largest and highest valued legacy auto company, Toyota (covered by Shinji Kakiuchi), refers to the ‘silent majority’ of auto executives who question over-committing to EV strategies at the sacrifice of other decarbonizing technologies. The vocal majority of auto industry followers (this author included) had criticized Toyota’s resistance to keep up with EV launches from competitors. While Toyota will eventually achieve scale in EVs, the later/follower approach may prove optimal over time.

5. Jumping the ‘electric shark?’ We would prepare for the application of IRA for legacy OEMs to disappoint vs. current high expectations. We ask investors to imagine the narrative of tens of billions of $ of taxpayer funds to help give vertically integrated and high scale players like Tesla an even greater advantage over high-employing traditional OEMs. Think about it.

6. Attrition: With respect to emerging (non-Tesla) EV startup strategy we believe ‘hunkering down’ to manage the pace of cash burn is a winning strategy. We anticipate more challenging capital markets environment may limit the number of EV players that can achieve sustainable scale.

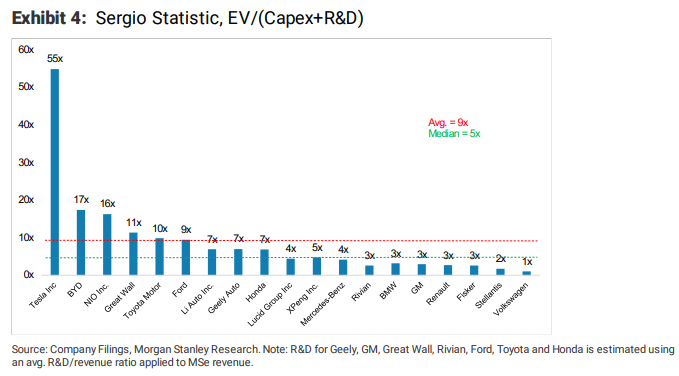

7. Forced capital discipline. Volkswagen (covered by Harald Hendrikse) spends its entire enterprise value in combined capex + R&D in just ~1 year. How long companies spend at this rate? In our view, it’s the capital not deployed that can frequently create the most value in auto stocks. In 2023, we think legacy automakers like GM and Ford have an opportunity to reconsider the quantum and timing of their EV investment plans last established during a very different economic and interest rate environment of 2020/2021.