Mortgage borrowing capacity has been obliterated

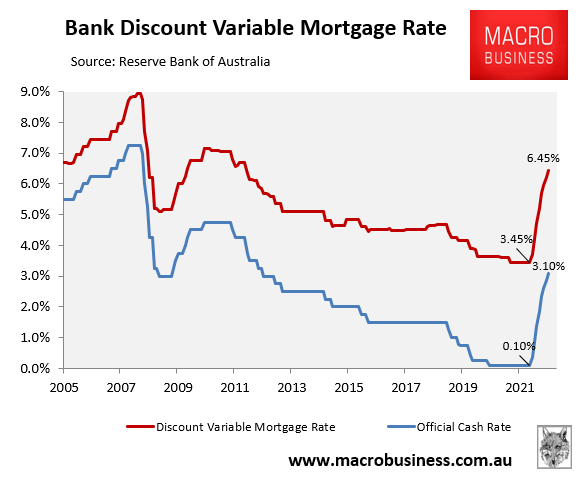

Today’s expected 0.25% increase in the official cash rate (OCR) by the Reserve Bank of Australia (RBA) will raise the average discount variable mortgage rate to 6.45%, up an extraordinary 3.0% from the 3.45% that presided before the first rate hike in early May.

Australian mortgage rates will climb to April 2012 levels if the RBA hikes by 0.25% in December.

This will take variable mortgage rates to their highest level since April 2012.

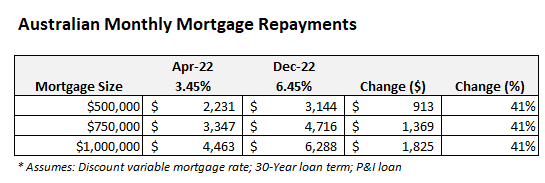

In turn, average variable monthly mortgage repayments will lift 41% above their pre-tightening level. For a borrower with a $500,000 mortgage, this will represent a $913 increase in monthly mortgage repayments:

An extraordinary lift in mortgage repayments in only eight months.

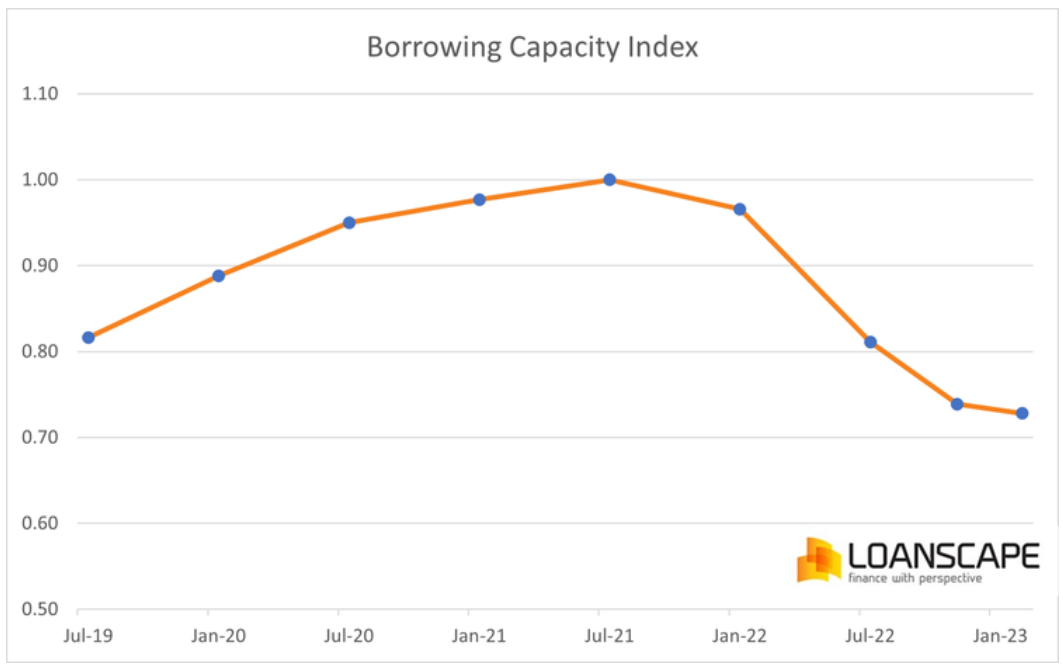

The RBA’s aggressive interest rate hikes have already driven down house prices lower by limiting borrowing capacity and shrinking the amount prospective home buyers can pay. This is illustrated clearly in the next chart from Loanscape, which shows that borrowing capacity has shrunk 27% from its peak in October 2021 when the APRA lifted its mortgage repayment buffer by 0.5% to 3.0%:

Loanscape: Borrowing capacity down 27% before Tuesday’s rate hike.

If the RBA follows through with another 0.25% rate hike later today, it will further reduce borrowing capacity to around 70% of its peak level.

Again, this reduction in borrowing capacity is the main reason why Australian house prices are falling at their fastest pace on record and will continue to do so if the RBA hikes rates further in 2023.

The process also works in reverse. So, once the RBA begins cutting rates in the second half of 2023 to ward off recession, borrowing capacity will rise, which will then push house prices higher in 2024. We could be ‘off to the races’ once more.

Until then, the extreme jump in mortgage repayments and falling house prices is a painful pill for home buyers that took out large mortgages to enter the market over the pandemic.

Many of these borrowers now face negative equity, especially if they purchased in Sydney and Brisbane where house prices have fallen hardest.