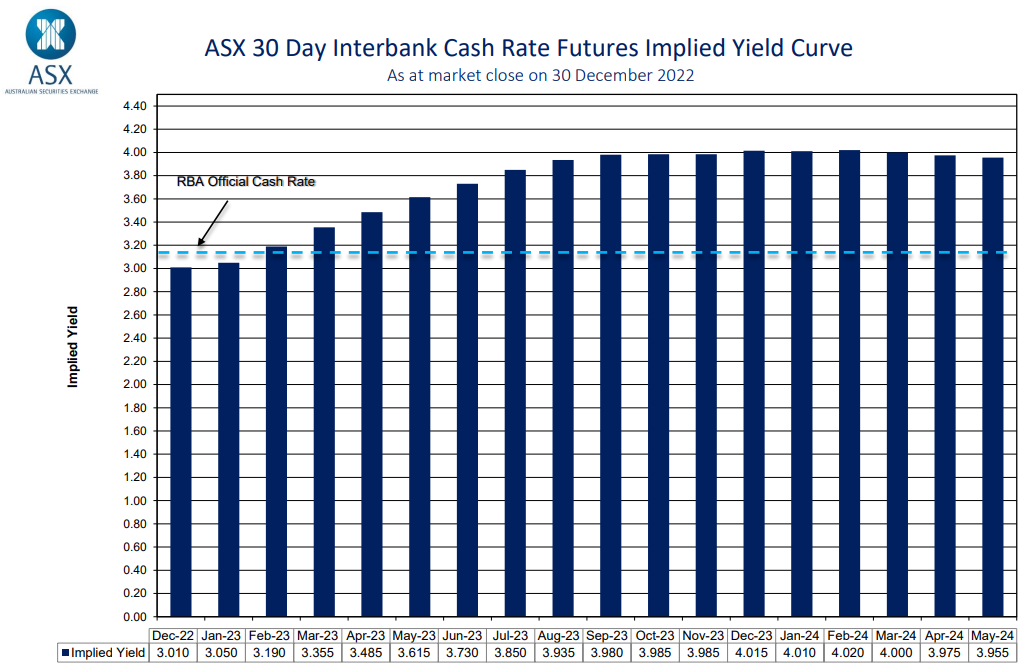

The futures market has lifted its projection for Australian interest rates, now tipping a peak official cash rate (OCR) of 4.0% by the end of 2023, up from 3.6% just before Christmas:

The futures market’s new OCR projection is at odds with Australia’s economists. The general consensus of 34 leading economists is that the Reserve Bank of Australia (RBA) will increase the cash rate two more times in the current monetary policy tightening cycle to 3.6%.

Most of the economists expect the RBA to increase the cash rate by 25 basis points at its first board meeting for the year in February. Although five economists, including AMP Capital’s Shane Oliver and Stephen Koukoulas, believe the RBA should pause its rate hikes immediately.

Opinion is also divided on when the RBA will begin reducing the cash rate. For example, Shane Oliver, Gareth Aird, Craig Emerson, Bob Cunneen and Paul Brennan forecast that the first rate cut will occur in the second half of 2023; although many do not expect the RBA to start doing so until 2024.

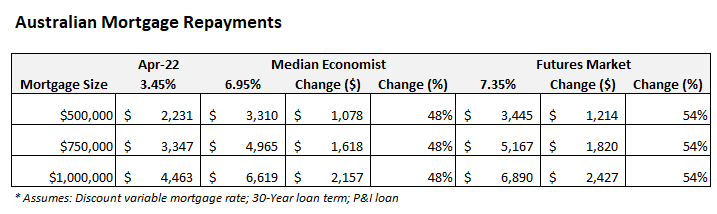

The below table illustrates the impact on mortgage holders from the futures market’s and the median economist’s forecasts:

The economists’ 3.6% peak OCR would see average variable mortgage rates rise to 6.95%, which would lift mortgage repayments 48% above their April 2022 pre-tightening level. This would add around $1,080 to monthly repayments on a $500,000 variable rate mortgage.

The futures market’s 4.0% peak OCR would see average variable mortgage rates lift to 7.35%. This would increase mortgage repayments 54% above their April 2022 pre-tightening level, adding around $1,200 to monthly repayments on $500,000 variable rate mortgage.

It is also worth reiterating that monetary conditions will tighten further in 2023 even without additional rate hikes from the RBA.

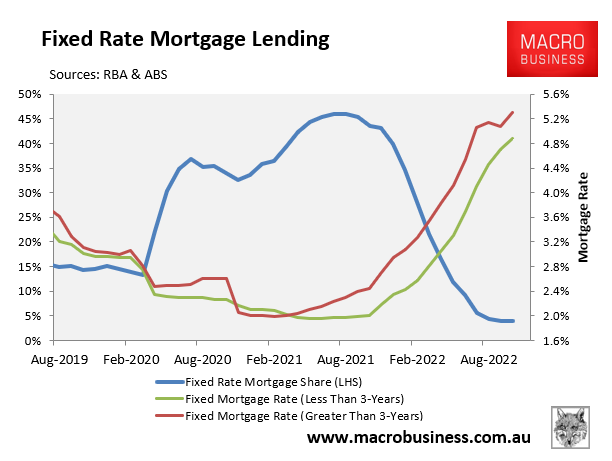

This is because the share of Australian home buyers that took out fixed rate mortgages surged over the pandemic from a long-term average of around 15% to an all-time high 46% in mid-2021:

Nearly one-in-four mortgages (by value) will switch in 2023 from ultra-low fixed rates originated at around 2% to rates that are more than double these levels.

The inevitable impact is further house price falls and cratering household consumption as more income is diverted away from spending towards debt repayments.