JP Morgan’s Michael Cembalest with the note:

Tracking the Fed, and where inflation goes from here

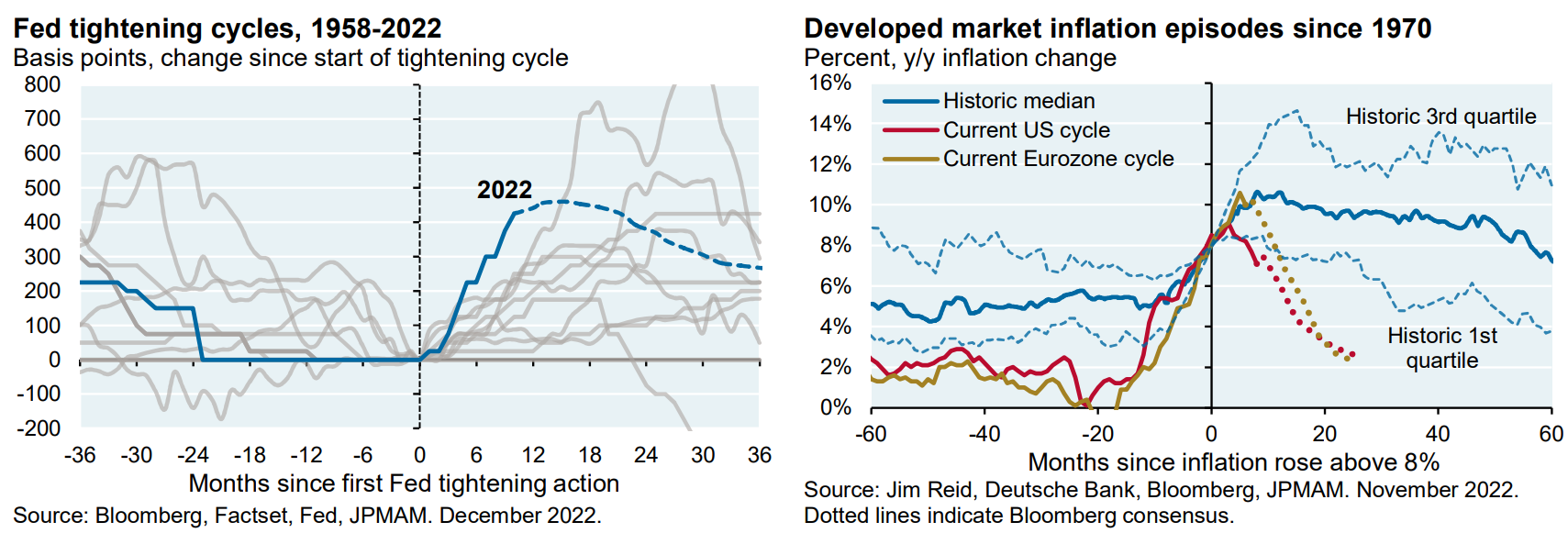

I expect inflation pressures to subside in 2023 and allow the Fed to pause at 5% to see where things go from there, and expect the 10 year US Treasury to remain below 4%. Inflation expectations derived from 10 year TIPS markets are back down at 2.25% from their 3% peak, so the Fed should be able to claim victory on that front after the fastest tightening cycle on record. If inflation cools as much as markets expect, it would be quite unusual: as shown in the second chart, the average developed market inflation spike takes longer to recede.

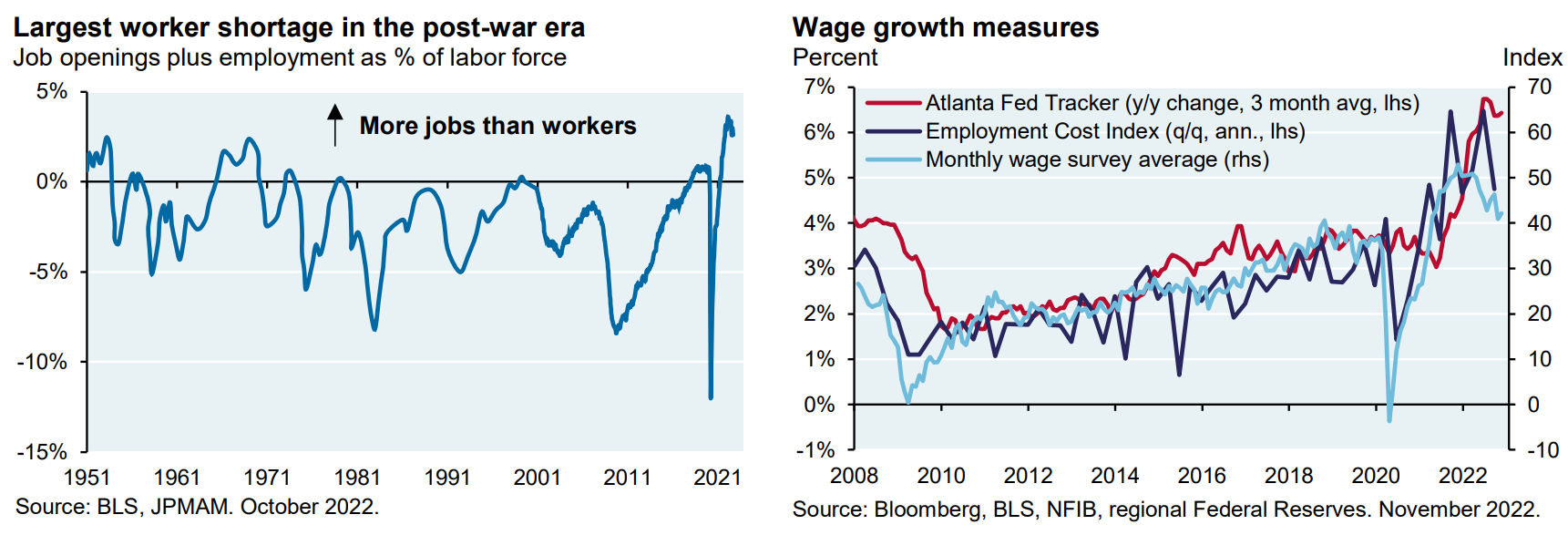

The challenge for the Fed is more related to wages than prices. By some measures, the US has been facing the tightest labor market on record: the highest job shortages in the post-war era, the lowest “job fill” rate, the largest premium for job switchers vs job remainers, etc. Wage growth is beginning to roll over based on measures we look at. So far, the largest layoffs have been in tech and homebuilding; layoffs ex-tech and homebuilding are still at the lowest level in 20 years [according to Challenger data].