So much for Jay Powell’s immaculate disinflation. DXY is up and roaring:

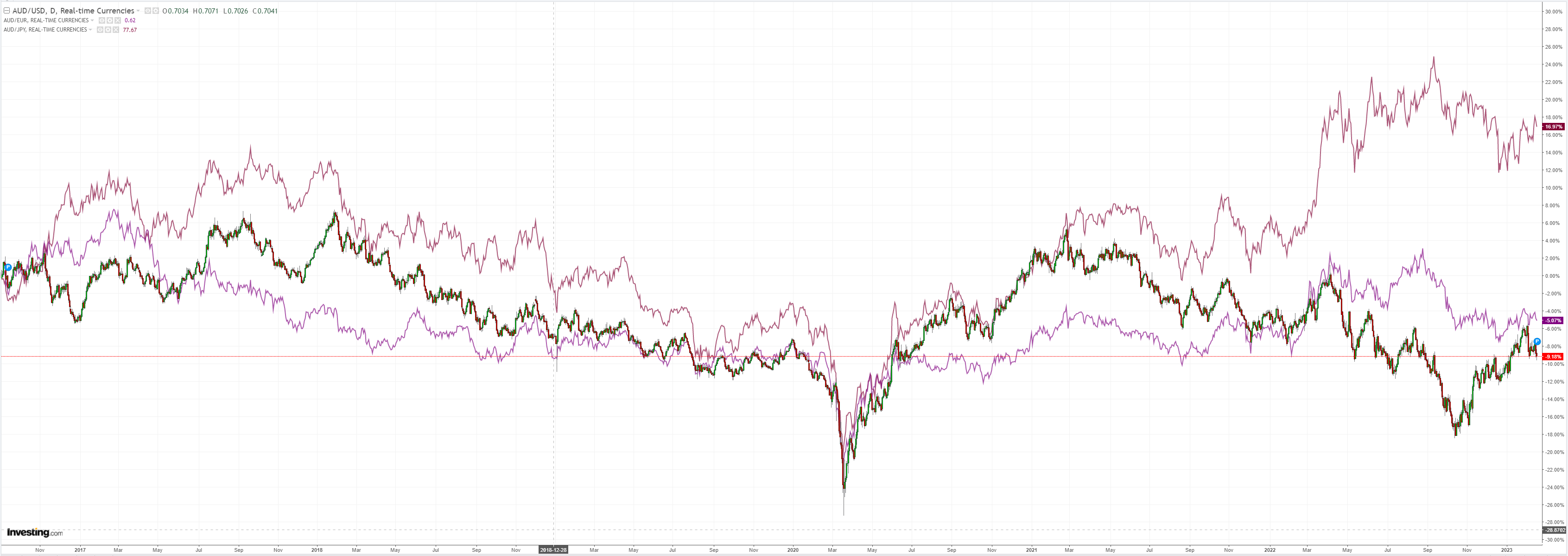

AUD is at the neckline of a head and shoulders top:

Advertisement

Gold knew:

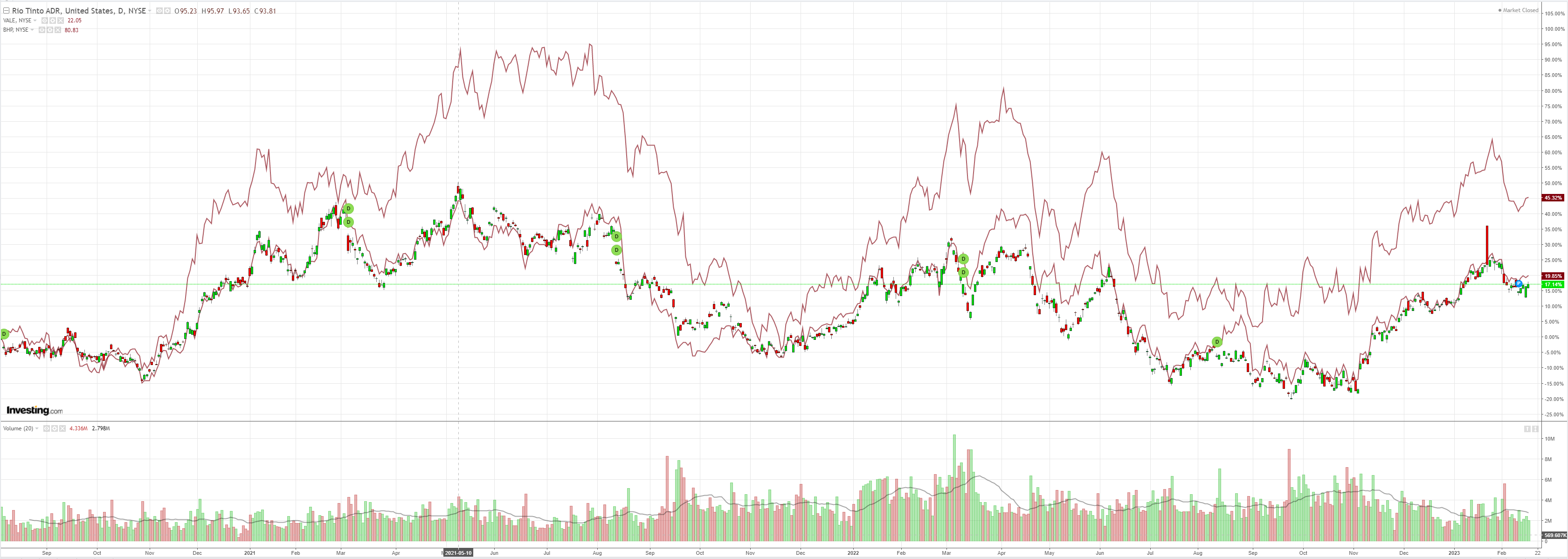

Metals were OK:

Miners too:

Advertisement

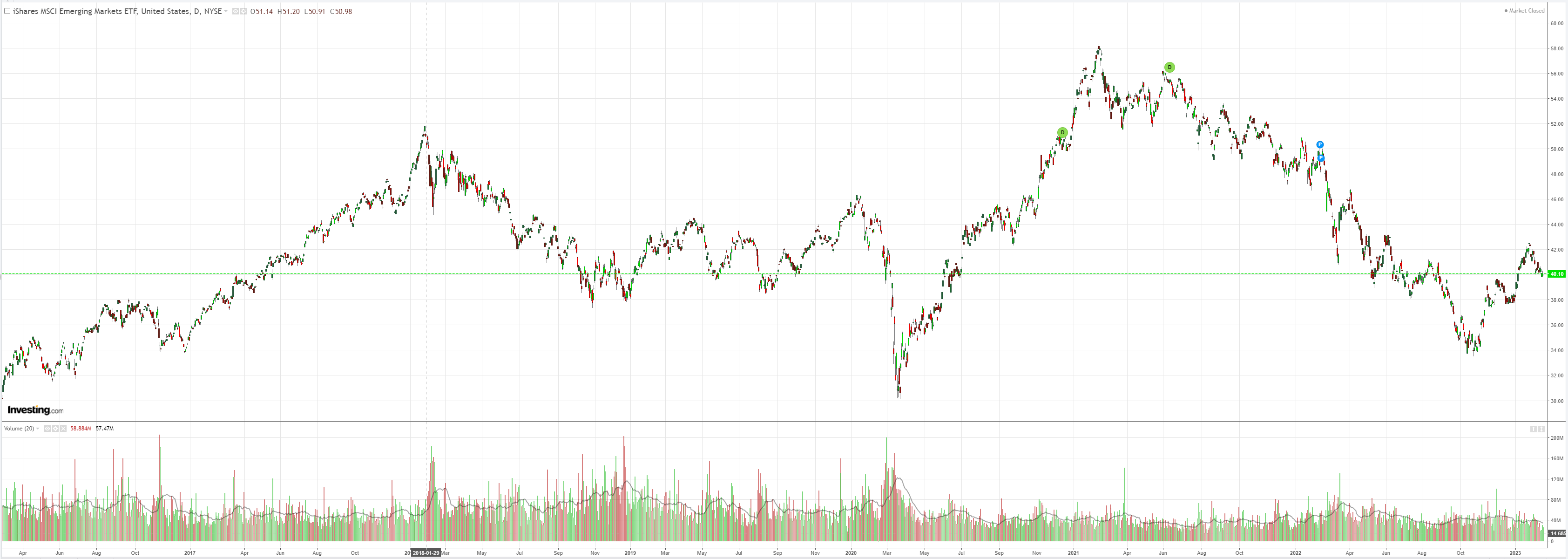

But not EM stocks:

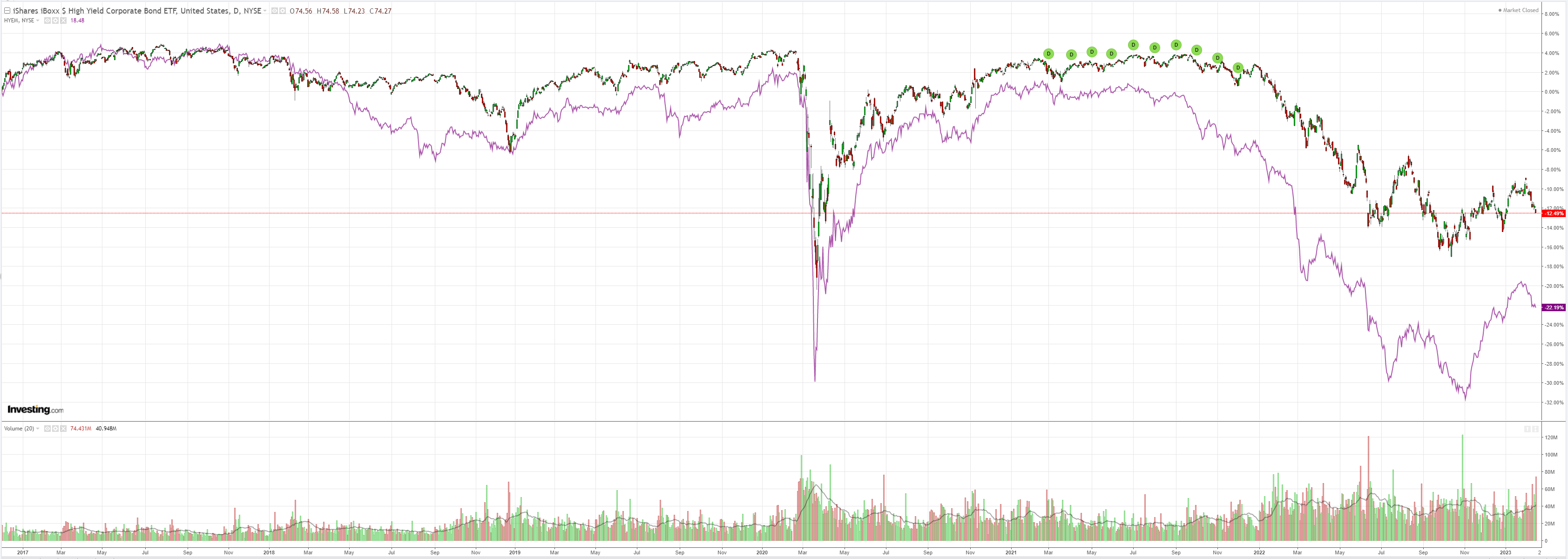

Nor junk:

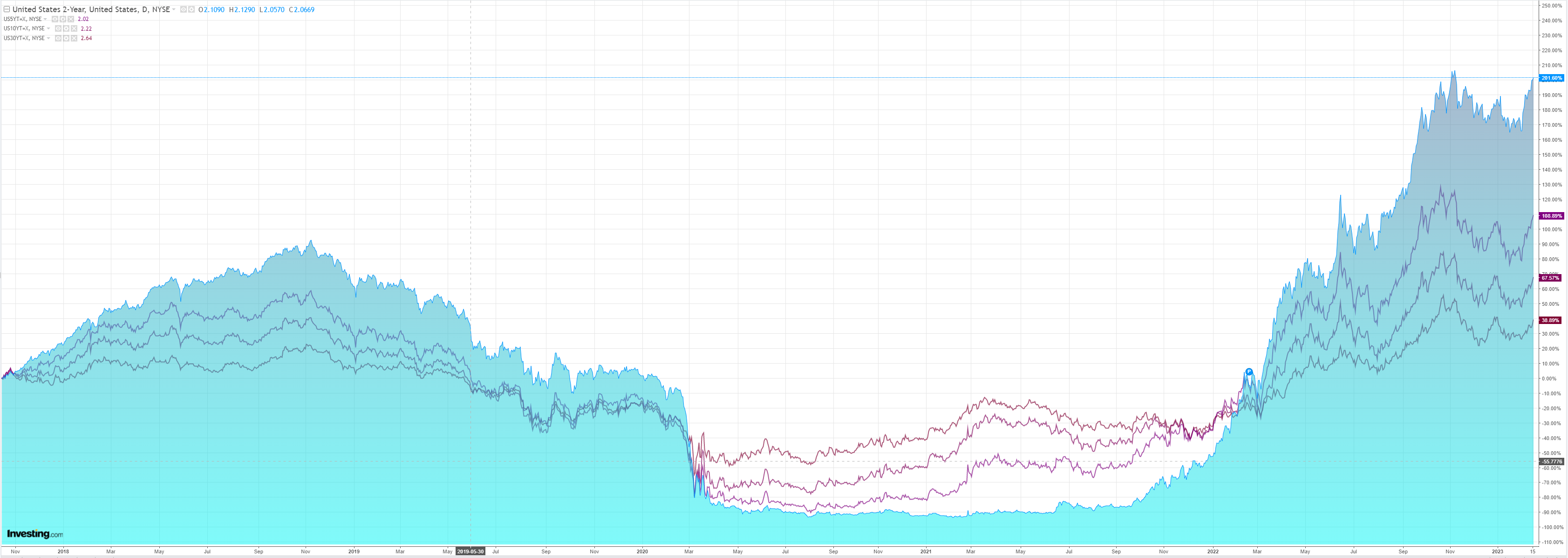

The Treasury curve steepened as the entire price deck threatens to back up anew:

Advertisement

Which smacked stocks upside the head:

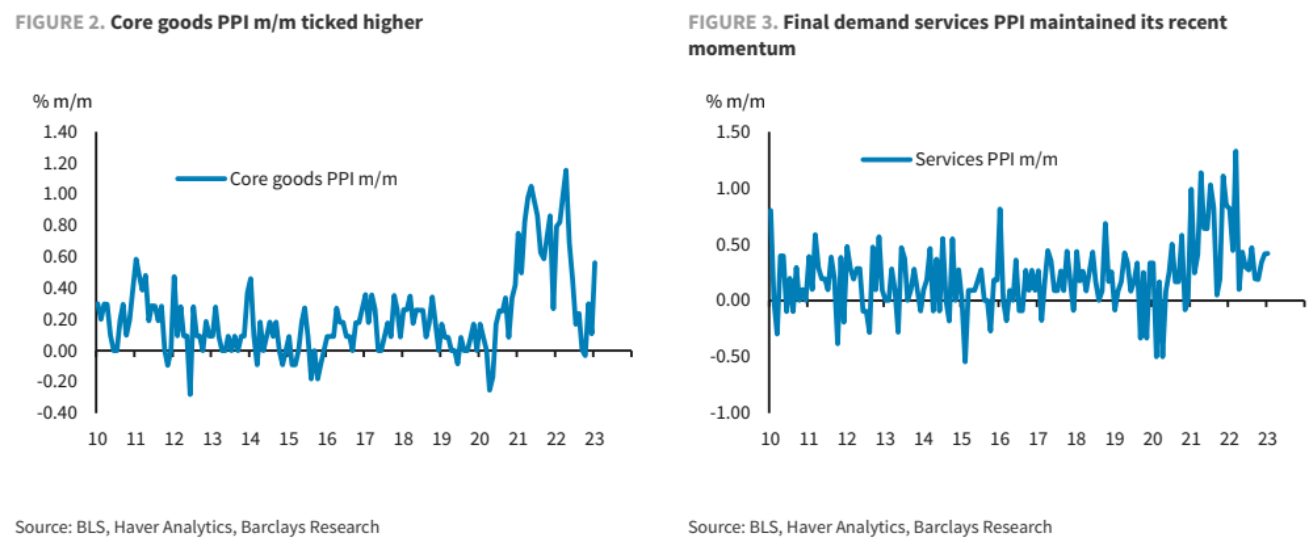

US PPI came in hot. Barclays:

Advertisement

The headline PPI rose 0.7% m/m, sa (6.0% y/y) in January, led in part by a surge in energy costs. That said, PPI inflation excluding food and energy also firmed, rising 0.5% m/m (5.4% y/y). US producer prices accelerated across the board in January

Final demand PPI rebounded 0.7% m/m (6.0% y/y) in January, following a revised 0.2% m/m decline (6.5% y/y) in December. This print was firmer than our and consensus forecasts (0.4% m/m). Core PPI, which excludes food and energy, was up 0.5% m/m (5.4% y/y), also stronger than forecasts (Barclays/consensus: 0.4% m/m). Excluding food, energy, and trade margins, final demand PPI was up 0.6% m/m (4.5% y/y), the largest monthly move since March 2022. Estimates after translating to PCE weights were similar, with the overall index rising 0.7% m/m, and the core index (excluding food and energy) up 0.5% m/m.

And the Fed panicked with Mester and Bullard deploying the jawbone for a 50bps hike next meeting.

Markets don’t buy it yet, with only a 13% chance:

Advertisement

But the Fed needs financial conditions to tighten again:

Most notably, it needs the stock market to fall because that is what is driving the re-acceleration in consumption:

Advertisement

The Fed pivoted too early and now it is pivoting again. AUD, EM, Europe, and commodities to the woodshed!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.