Yes, you read that right. Clearly, markets were positioned for the hot CPI. DXY fell:

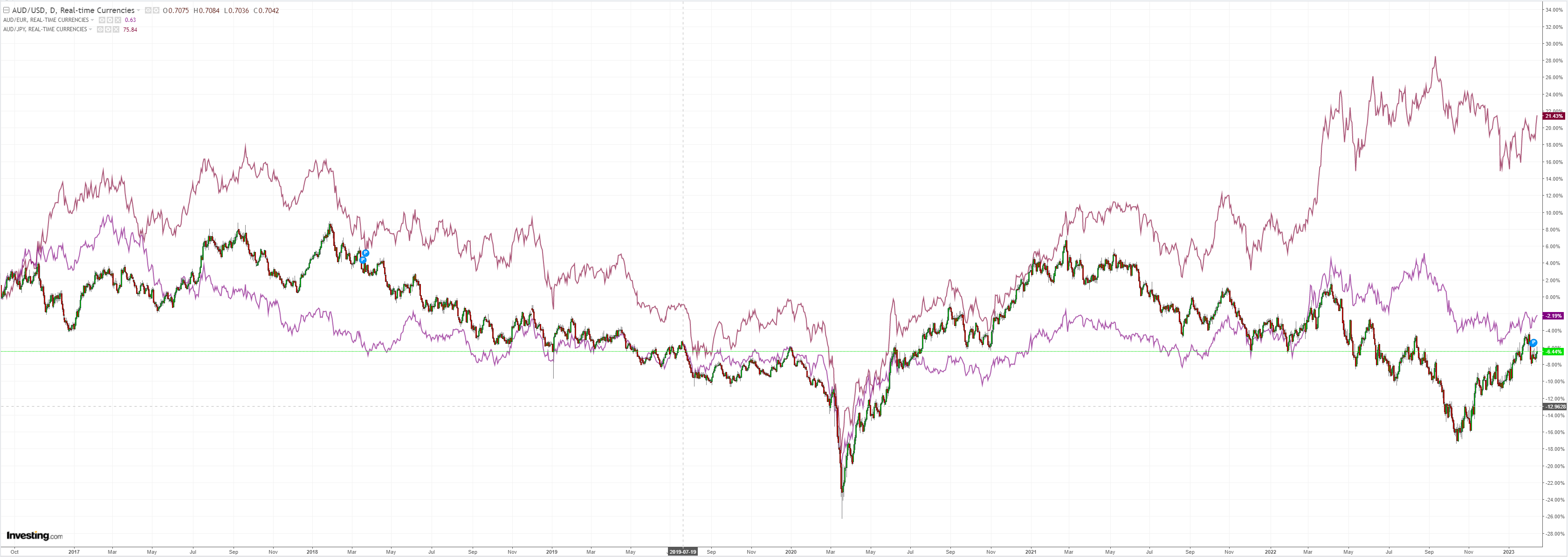

AUD popped:

Oil and gold fell:

Advertisement

Base metals did nothing:

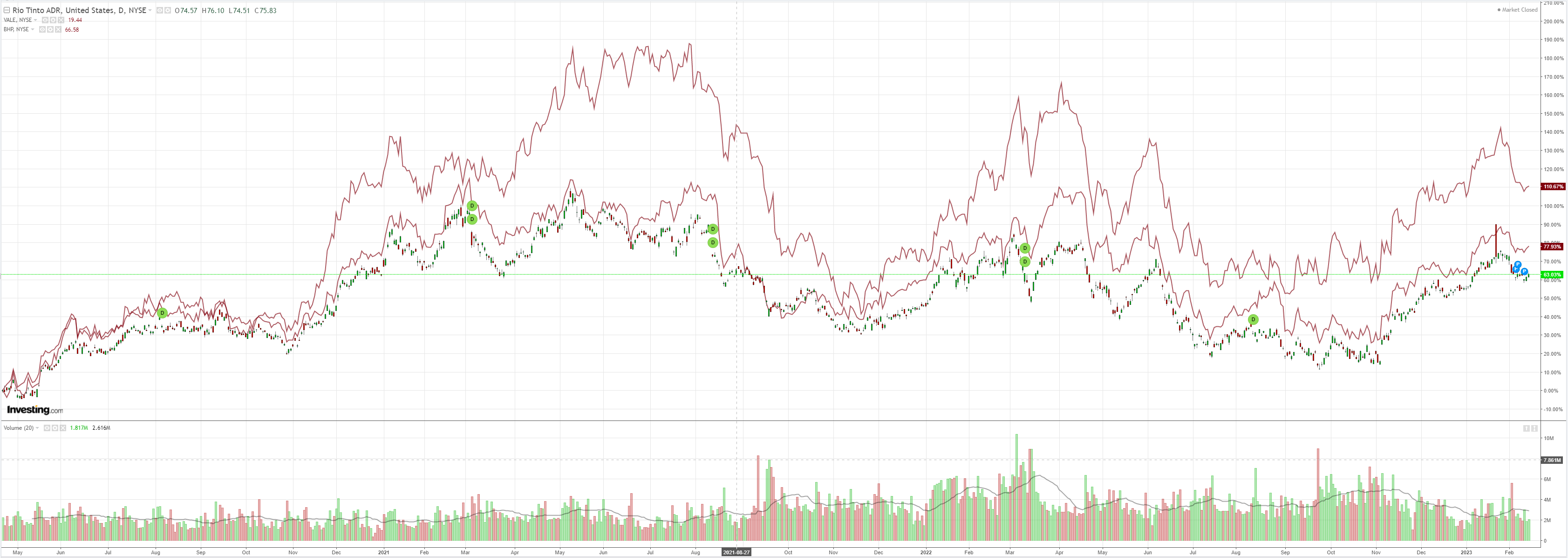

Miners lifted:

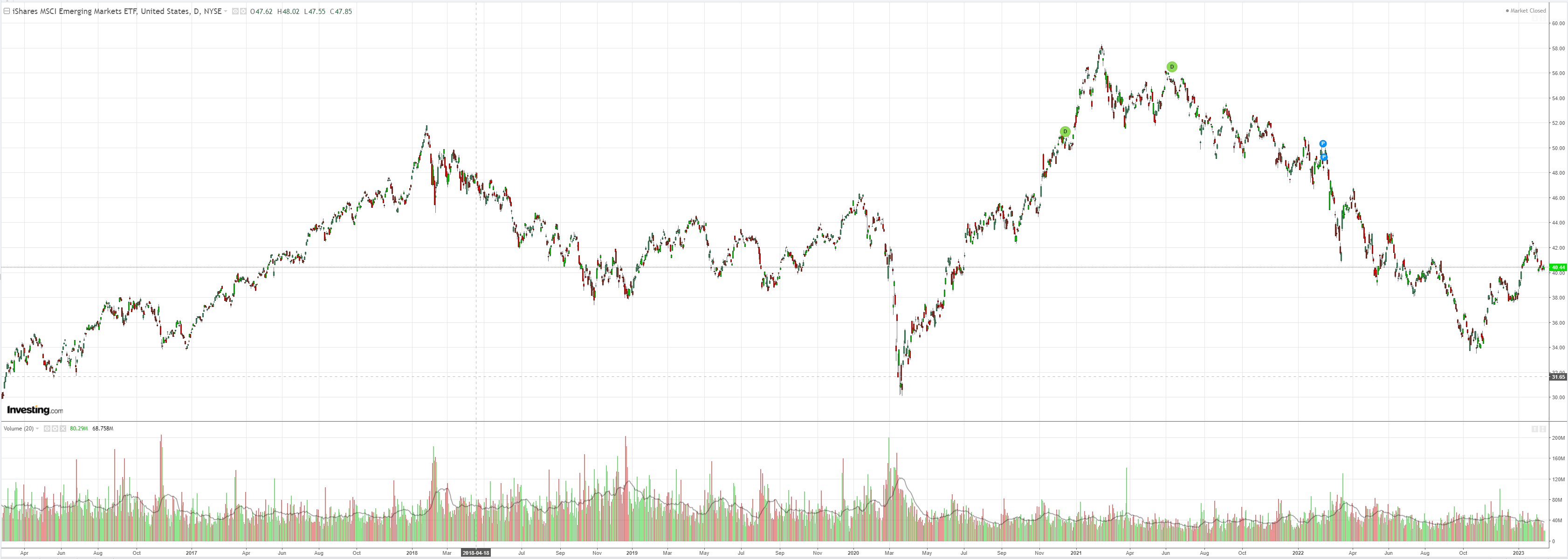

Not EM:

Advertisement

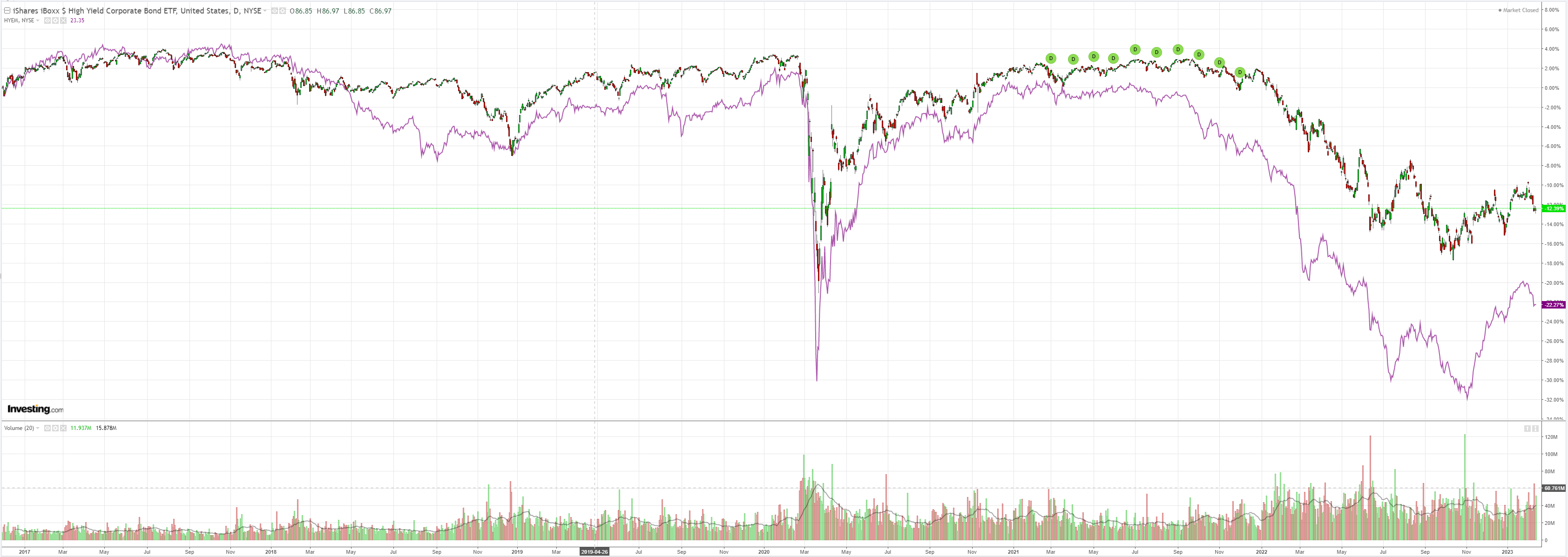

Nor junk:

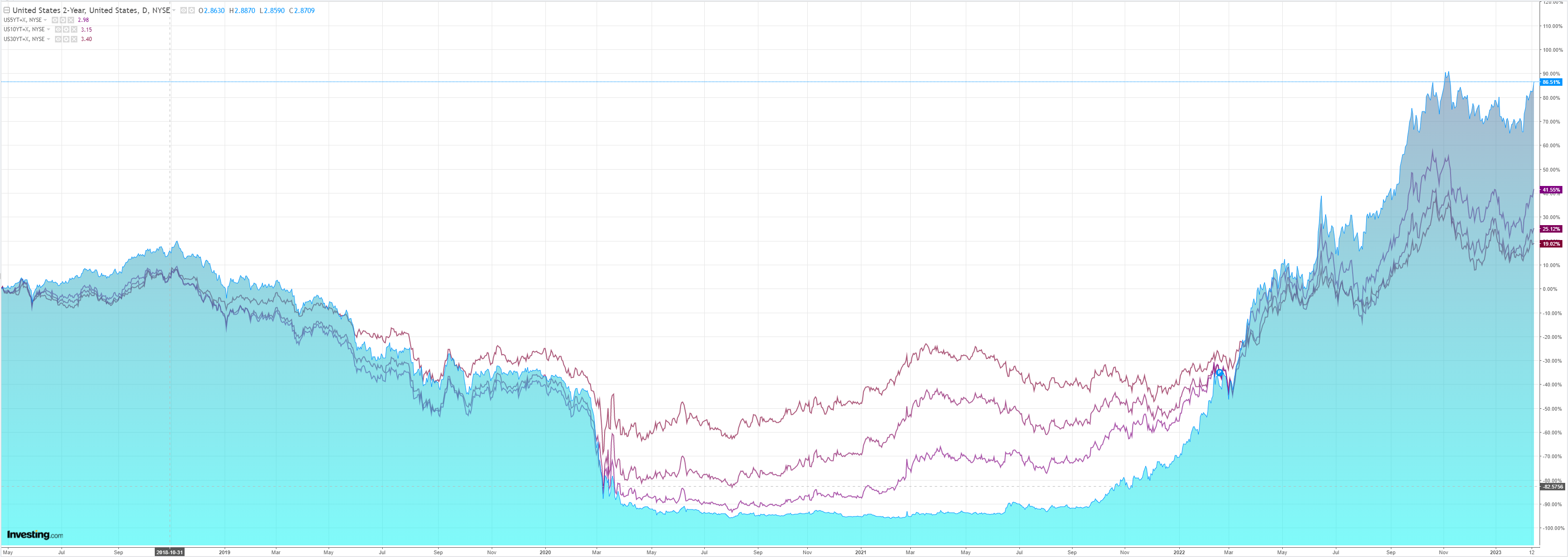

As the Treasury curve was smashed:

But stocks only go up:

Advertisement

BofA with the report:

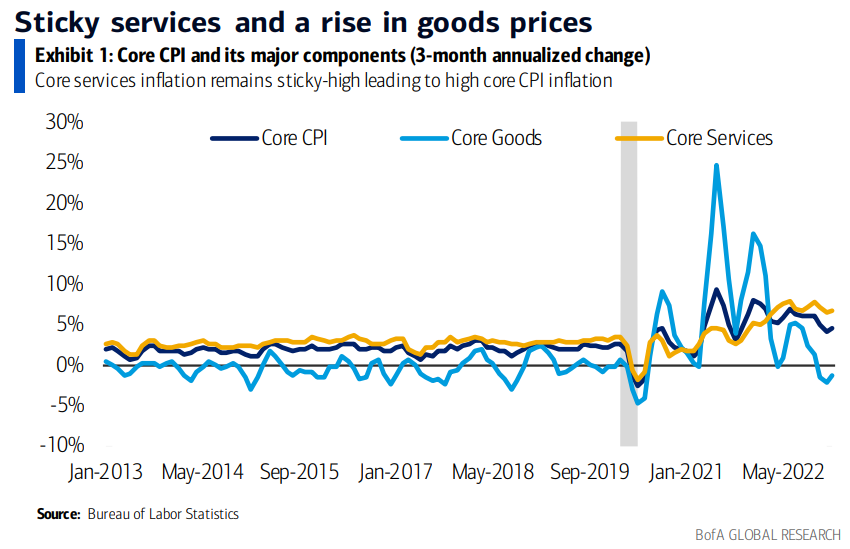

The January CPI report was in line with expectations. Headline CPI inflation increased by 0.5% m/m in January (+0.517% unrounded). As a result, the y/y rate ticked down slightly to 6.4% from 6.5% previously, and the NSA index came in at 299.171. Core CPI meanwhile rose by 0.4% m/m (+0.412% unrounded), or 5.6% y/y. Over the last three months core CPI has increased at a 4.6% annualized rate, accelerating slightly from the 4.3% pace in December.

In our view, there is not a lot of new information in this report. The Fed will need to see moderation in services inflation before having confidence that 2% is achievable. Today’s report did not drastically alter the risks around the policy outlook. We still see risks tilted to a terminal above our baseline estimate of 5.0-5.25% on account of labor markets and risks around services inflation staying sticky.

The details

The increase in headline CPI was largely driven by two components: energy and shelter. Together these components accounted for three-fourths of the 0.5% increase. Energy prices rose by 2.0% m/m driven by higher gas prices and shelter inflation rose by 0.7% m/m. The former was stronger than we expected, while the latter was roughly in line with our expectations. Additionally, food prices rose by 0.5%, in-line with the revised trend in 4Q.

Meanwhile, Core inflation was also driven by shelter inflation, which accounted for 32bp of the 41bp increase. Within core inflation services remained sticky at 0.5% m/m, in line with our expectations. Over the last three months, core services prices have risen by 6.8% annualized, well above the pre-pandemic pace. Granted much of the increase in core services reflects the ongoing strength of shelter inflation, which increased by 0.7% m/m. Within shelter Owners’ equivalent rent (OER) and rent rose by 0.7%, in line with our expectations. However, lodging away from home surprised relative to our forecasts with a 1.2% m/m increase.

Outside of shelter. Medical care services fell by 0.7% m/m owing to a 3.6% drop in health insurance and a 0.1% decline in professional services. This was much weaker than our expected 0.1% m/m decline. Meanwhile, other services generally accelerated this month with transportation services rising by 0.9% m/m, education, and communication up 0.5% m/m and recreation services up 0.7% m/m. The Fed will likely take little comfort in these readings as it looks for signs that services inflation ex-housing is moderating.

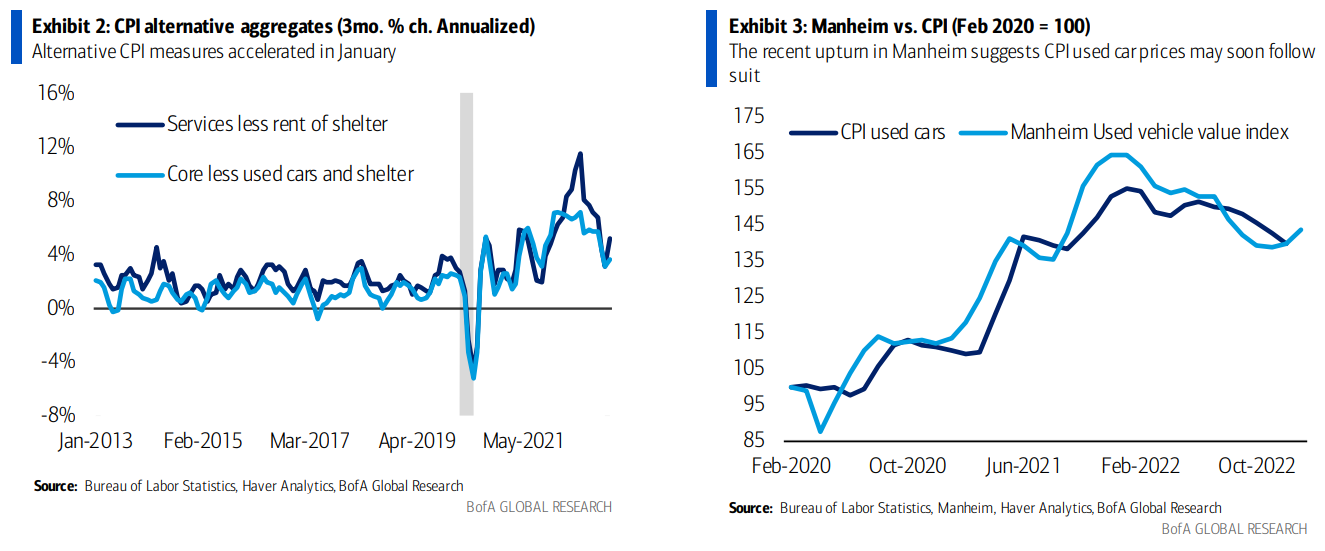

While core services inflation was broadly in line with our expectations, core goods inflation was stronger than we expected, rising by 0.1% m/m. This broke a streak of three consecutive decreases in core goods prices. Used car prices did fall again (-1.9% m/m), but that streak may be coming to an end soon based on data from Manheim (Exhibit 3). Additionally, the weight of used cars was reduced in the latest update. Therefore, it should be less of a swing factor moving forward. Excluding used cars, core goods rose by 0.5% m/m and 3.5% annualized over the last three months. While this is a noticeable deceleration, it is well above the pre-pandemic pace. Additionally, it suggests that goods price deflation is not broadening outside of used cars as we have been anticipating.

Fed implications

In our view, there is not a lot of new information in this report. Core services was solid at 0.5%, driven by still-solid shelter at 0.7% and strong services ex-shelter. On net, the disinflation we are seeing remains narrow, driven by a few key core goods components, and it has yet to broaden. The Fed will need to see moderation in services inflation before having confidence that 2% is achievable. We still see risks to our terminal rate forecast of 5.0-5.25% as being tilted to the upside on account of labor markets and risks around services inflation staying sticky.

Sounds right to me. The expected Fed pivot is dead. The curve is the most inverted since 1981. Yet there are atill higher US yields ahead.

At some point, this is going to dawn on stocks and the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.