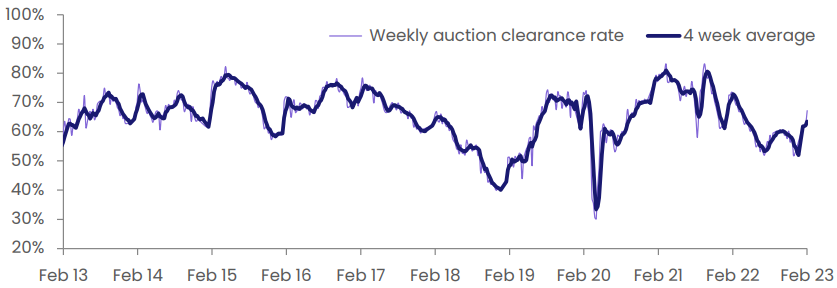

The Australian housing market is enjoying a purple patch, with auction clearance rates and prices rebounding over recent weeks despite another interest rate hike from the Reserve Bank of Australia (RBA).

This weekend’s preliminary auction clearance rate was 69.7%, which follows the previous weekend’s preliminary clearance rate of 70.8%, revised down to 67.2% at final figures:

This weekend’s clearance rate was based on a total of 2393 capital city auctions, which was a 27% decrease in volume from the 3386 auctions held in the same week last year.

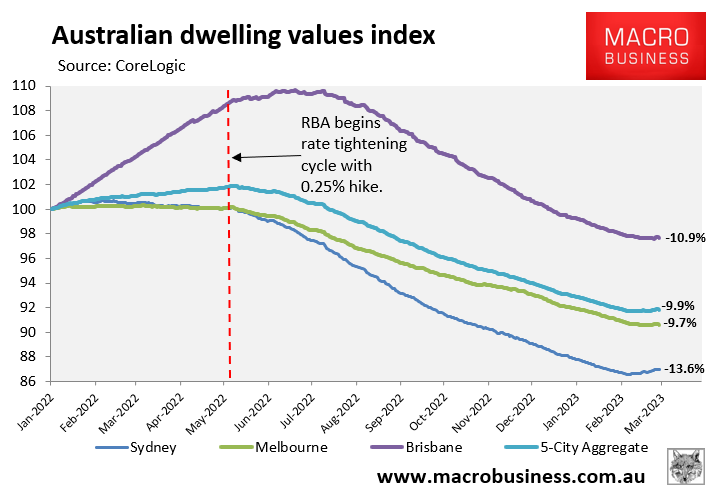

At the same time as auction clearances have rebounded, CoreLogic’s daily dwelling values index is also rising.

Since 7 February 2023, dwelling values at the 5-city aggregate level have risen 0.2% driven by a 0.4% increase across Sydney:

This unexpected rebound has led to speculation that Australia’s housing correction might have come to an end, brought about by an acute shortage of stock, soaring rents, and record overseas migration.

However, SQM Research managing director, Louis Christopher, warns of “false dawn”. That is, should the RBA continue to lift the official cash rate above 4% (from 3.35% currently), then the housing correction will reassert itself and prices could fall another 8%.

“We need to be prepared for the possibility of a ‘false dawn’ in the market where would-be buyers believe the market is turning, but then we see a new weakness in the market due to additional cash rate hikes”, Christopher said over the weekend.

Coolabah Capital’s Chris Joye likewise warned that “the great housing crash has stalled, but is far from over”:

Joye notes that CoreLogic’s daily dwelling values index is not seasonally adjusted. “And CoreLogic finds house prices generally climb between February and May. March is the seasonally strongest month of the year in terms of capital gains”.

The bigger issue, according to Joye, is that “only a portion of the Reserve Bank of Australia’s 325 basis points worth of interest rate increases have been felt by borrowers thus far”.

“The central bank estimates that roughly one-third of all home loan borrowers are on fixed-rate products. To date, these fixed-rate borrowers have not worn any rate changes at all”.

Joye estimates that once you account for the abnormally high share of fixed rate mortgage borrowers, “interest rates have only lifted about 210 basis points since the RBA started tightening monetary policy last May”.

“Put another way, Aussie households have yet to be hammered by about 115 basis points of the 325 basis points worth of RBA rate increases (or 35% of the total move)”.

Once nearly 900,000 fixed rate borrowers (representing $350 billion worth of mortgages) reset to variable rates this year, they “will be smashed by a huge increase in their cost of capital, which in most instances will jump from about 2% to 6%”.

Joye notes that borrowing capacity has already been slashed by one third on the back of the RBA’s 3.25% of rate hikes. And when the RBA inevitably hikes several more times in the months ahead, borrowing capacity will shrink further.

Accordingly, Joye is holding to his forecast that Australian house prices will “decline in 2023 with total peak-to-trough losses in the order of 15% to 25%”.