By Gareth Aird, head of Australian economics at CBA

Key Points:

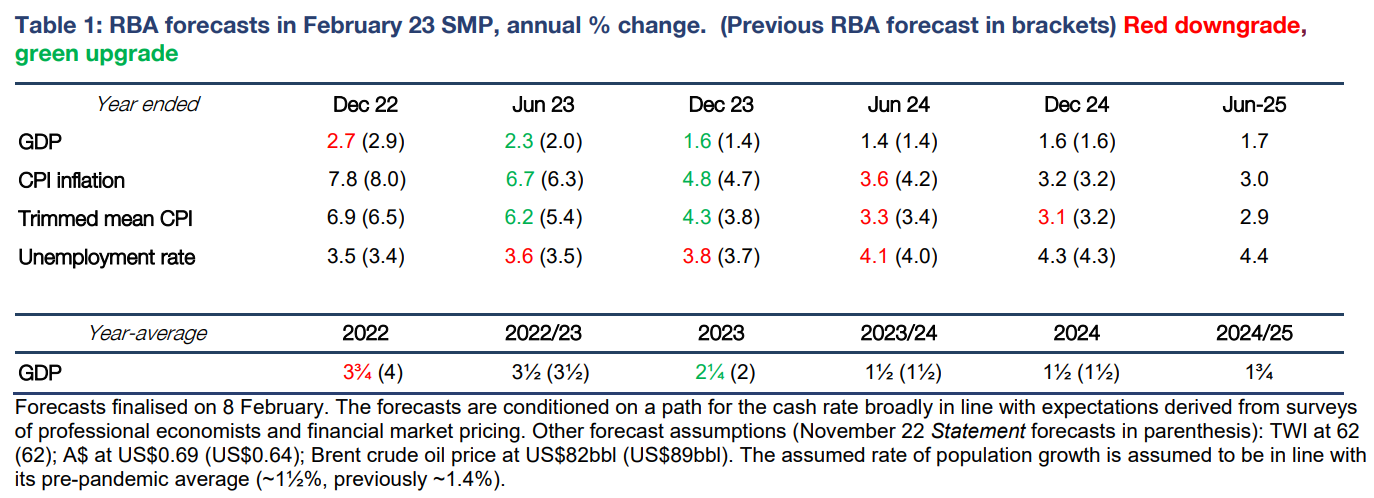

- The RBA has made no material changes to their headline inflation, GDP or unemployment rate forecasts.

- But expectations for underlying inflation and wages growth in 2023 have been revised up, which underpins the hawkish shift at the February Board meeting.

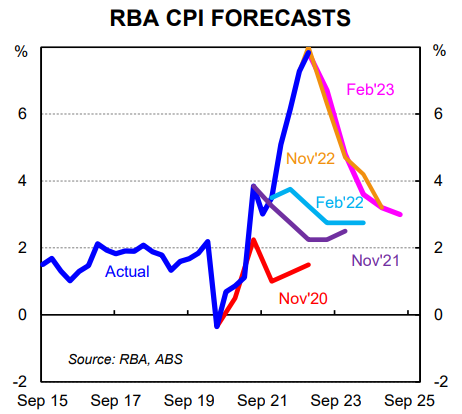

- The RBA expects annual inflation to have peaked in Q4 22 at 7.8% and to be 4.8% in Q4 23 and 3.2% in Q4 24.

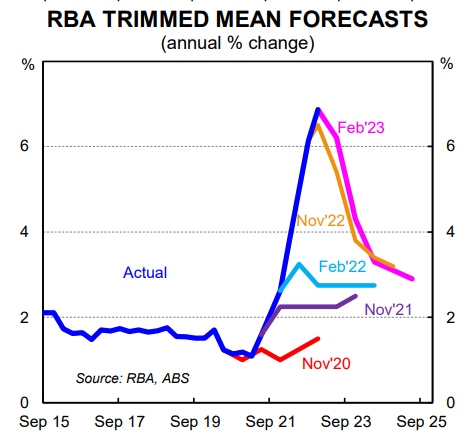

- Underlying inflation is forecast to be 4.3%/yr in Q4 23 and 3.1%/yr in Q4 24.

- The RBA have left their GDP profile broadly unchanged and expect growth of 1.6%/yr in both Q4 23 and Q4 24.

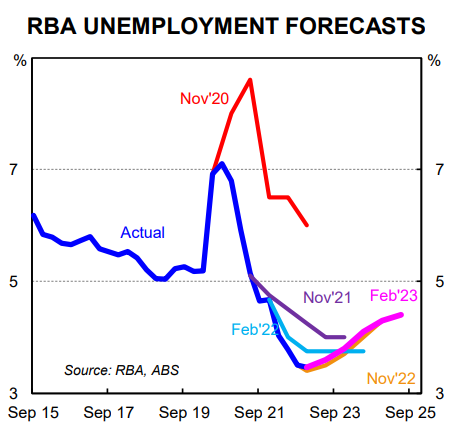

- The RBA’s forecasts for the unemployment rate look optimistic – the RBA expects the unemployment rate to be 3.8% in Q423 and 4.1% in Q2 24 (we forecast a higher unemployment rate of 4.3% in Q4 23 and 4.4% in Q2 24).

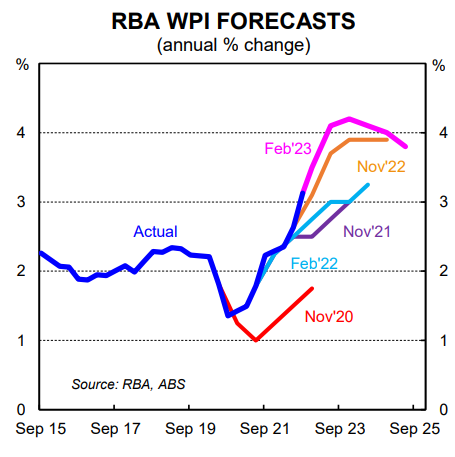

- The RBA have made an upward revision to their forecasts for annual wages growth and expect it to be 4.2% in Q4 23 before edging lower to 4.0% in Q4 24 (we forecast wages growth to peak at 3.8%/yr).

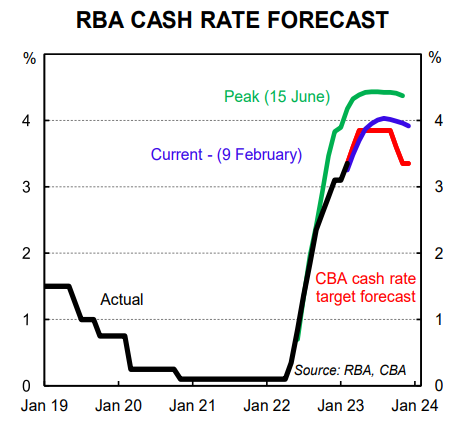

- We expect two further 25bp rate hikes in March and April that would take the cash rate to 3.85% (our expectation for the peak in the cash rate).

- We continue to think policy easing will be required in Q4 23 if Australia is to avoid a hard landing. We expect 50bp of rate cuts in Q4 23 and a further 50bp of easing in H1 24.

RBA has signalled more rate hikes ahead

The RBA’s February Statement on Monetary (SMP) comes in the wake of the 25bp rate hike at the February Board meeting, which took the cash rate to 3.35%.

The decision to raise the cash rate by 25bp in February was widely anticipated by us and most analysts. But the RBA delivered a surprisingly hawkish message. More specifically, there was a clear shift in tone and forward guidance in the Governor’s Statement accompanying the decision.

That hawkish tilt was apparent again in the February SMP, albeit a little less pronounced. In the Governor’s Statement accompanying the Board decision on Tuesday it was stated that, “the Board expects that further increases in interest rates will be needed over the months ahead”. Today that equivalent forward guidance stated, “the Board expects that further increases in interest rates will be needed”.

We are not drawing too much into this slight tweak today.

We believe the changes the Governor made to his Statement this week imply that the RBA Board has essentially made up their mind and intend to raise the cash rate further over coming months. Indeed it would be a big shock now if the RBA did not tighten policy further.

We modified our central scenario for the cash rate on Tuesday due to the change in language in the Governor’s Statement.

Despite that, we maintain that there is a strong case to pause. Monetary policy works with a lag and the RBA is flying blind given they have put through an incredible amount of tightening that is yet to fully impact home borrower cash flow and by extension spending decisions.

In addition around a fifth of mortgages are fixed at ultra-low rates and will expire this year. This means that there is a lot of tightening to come. And the initial impact of rate hikes has been blunted due to more borrowers on fixed rates than usual.

Indeed the RBA recognised this to some extent today. Box A contained an excellent analysis on Mortgage Interest Payments in Advanced Economies.

That all said, the RBA is clearly more concerned about inflation becoming entrenched. And we now expect the RBA Board to raise the cash rate by a further 25bp at both the March and April Board meetings. This would take the cash rate to 3.85%.

Our assessment of the economy and also the RBA’s updated forecasts are based on the expectation that the cash rate is taken to 3.85% over coming months (for completeness the RBA’s forecasts assume the cash rate peaks at 3¾% in mid-23 and declines to ~3% by mid-25). We continue to look for policy easing in late 2023 and have 50bp of cuts in our profile.

Forecasts look too optimistic on unemployment, too pessimistic on inflation

Forecasts for GDP, unemployment, inflation and wages should not be looked at in isolation. Rather it is the outlook for GDP that should drive the profile for the unemployment rate which then feeds into inflation and wages forecasts.

On balance we believe the RBA’s forecasts underestimate the impact that their policy tightening will have on the economy.

No economist has a crystal ball. But the RBA’s forecast profile for the unemployment rate looks too positive to us given their GDP forecasts. We also expect inflation to recede more quickly than the RBA (more on that below).

The RBA forecasts GDP to be 1.6%/yr in both Q4 23 and Q4 24. In our view these forecasts sit on the optimistic side of the fence (we forecast GDP to be 1.1%/yr at Q4 23).

The RBA’s base case points to household consumption growth of 1.7%/yr in Q4 23. We expect a weaker outcome as the lagged impact of rate hikes coupled with the fixed rate rollover slows the consumer more significantly over the year. We forecast household consumption growth will be 1.3%/yr in Q4 23.

Despite our expectation for economic growth to come in a little weaker than the RBA forecast, it must be noted that the RBA expects GDP growth to be significantly below trend (trend growth is assumed to be ~2.5%/yr in Australia). A forecast for below trend growth should be coupled with a commensurate forecast lift in the unemployment rate. But the RBA expects only a very gradual increase in

the unemployment rate.

The RBA has forecast the unemployment rate to lift by just 0.3ppts over 2023 to end the year at 3.8%. In our view this forecast is too optimistic. And it looks to be an ambitious outcome given their profile for GDP.

Okun’s law1 would indicate a higher unemployment rate forecast for the RBA’s GDP profile (~4% end 2023 based on GDP growth 1.0ppt below trend). Further out, the RBA has forecast the unemployment rate to be 4.1% by mid-2024. This is more positive than our forecast and the Commonwealth Government’s forecasts (both CBA and the Government expect the unemployment rate to be ~4.5% by

mid-2024).

Forecasts look too optimistic on unemployment, too pessimistic on inflation

Forecasts for GDP, unemployment, inflation and wages should not be looked at in isolation. Rather it is the outlook for GDP that should drive the profile for the unemployment rate which then feeds into inflation and wages forecasts.

On balance we believe the RBA’s forecasts underestimate the impact that their policy tightening will have on the economy.

No economist has a crystal ball. But the RBA’s forecast profile for the unemployment rate looks too positive to us given their GDP forecasts. We also expect inflation to recede more quickly than the RBA (more on that below).

The RBA forecasts GDP to be 1.6%/yr in both Q4 23 and Q4 24. In our view these forecasts sit on the optimistic side of the fence (we forecast GDP to be 1.1%/yr at Q4 23).

The RBA’s base case points to household consumption growth of 1.7%/yr in Q4 23. We expect a weaker outcome as the lagged impact of rate hikes coupled with the fixed rate rollover slows the consumer more significantly over the year. We forecast household consumption growth will be 1.3%/yr in Q4 23.

Despite our expectation for economic growth to come in a little weaker than the RBA forecast, it must be noted that the RBA expects GDP growth to be significantly below trend (trend growth is assumed to be ~2.5%/yr in Australia). A forecast for below trend growth should be coupled with a commensurate forecast lift in the unemployment rate. But the RBA expects only a very gradual increase in

the unemployment rate.

The RBA has forecast the unemployment rate to lift by just 0.3ppts over 2023 to end the year at 3.8%. In our view this forecast is too optimistic. And it looks to be an ambitious outcome given their profile for GDP.

Okun’s law1 would indicate a higher unemployment rate forecast for the RBA’s GDP profile (~4% end 2023 based on GDP growth 1.0ppt below trend). Further out, the RBA has forecast the unemployment rate to be 4.1% by mid-2024. This is more positive than our forecast and the Commonwealth Government’s forecasts (both CBA and the Government expect the unemployment rate to be ~4.5% by

mid-2024).

Additional boxes in the February 2023 Statement

The Statement also included a couple of interesting boxes with a focus on very topical issues. Below we highlight two.

Box A: Mortgage interest payments in advanced economies

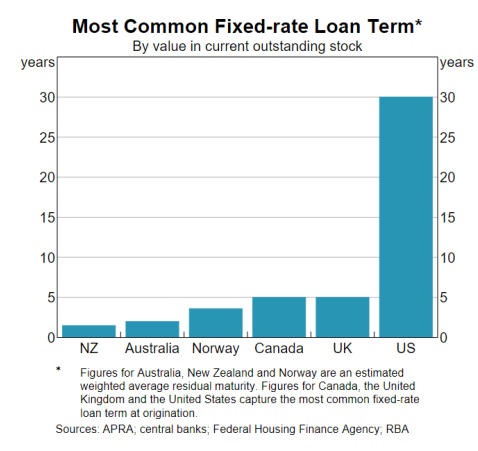

This box is of particular interest given the high level of household indebtedness in Australia – it’s well worth a read. The box notes that the transmission of monetary policy in Australia is generally much quicker than elsewhere. Our predominantly variable-rate mortgage market means that a lift in the cash rate flows through almost immediately to higher mortgage rates for a majority of borrowers. This is

even after accounting for the three month lagged cash flow impact, something we’ve talked about since September last year.

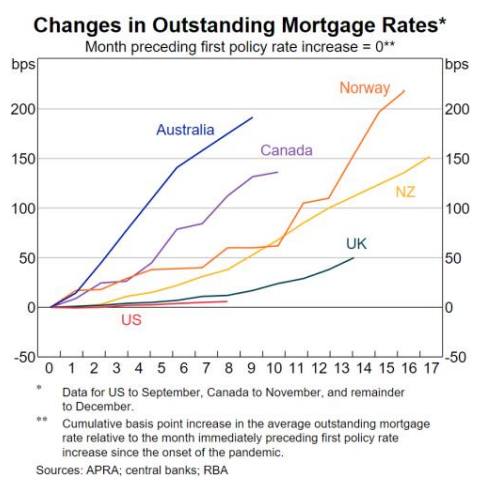

The quicker and fuller pass-through of rate rises to the average mortgage rate, coupled with high levels of household debt in Australia, is what makes each RBA rate hike potent. Indeed, that has been the crux of our view that the RBA can deliver a shallower hiking cycle than in many other economies. As the facing chart shows, it can be argued that the RBA has actually tightened more aggressively than

almost any other peer central bank. For instance, the average outstanding mortgage rate in Australia has increased by almost 50bp more than in New Zealand, despite the cash rate almost 100bps lower (3.35% vs 4.25%). That reflects the fact that around 70% of Australian’s mortgages are variable-rate while only around 10% of the mortgage stock in NZ is on variable rates.

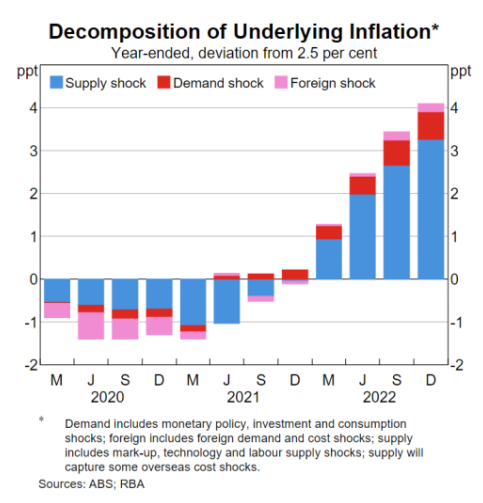

Box C: Supply and demand drivers of inflation in Australia

The RBA applied various models to decompose the recent increase in inflation into demand- and supply-side drivers. One model (using the San Francisco Fed’s method) shows supply factors were responsible for around half of the increase in headline inflation over the year to September 2022.

Another model suggests that supply shocks drove around three-quarters of the lift in underlying inflation to date, mostly in the tradables and the housing sector. Looking ahead, our view is that the evidence from other economies suggest tradable goods inflation has slowed as supply chain disruptions continue to dissipate and demand continues to ease. That dynamic is likely to play out in Australia.

Recent inflation data here also show that housing construction costs are moderating too.

Next week will be an important one for RBA watchers. Governor Lowe will appear before parliamentary committees on two occasions (15/2 and 17/2).