CBA: RBA “to pause very soon” on soft wage growth

By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The Wage Price Index (WPI) rose by0.8%/qtr in Q4 22 and the annual rate stepped up to 3.3%.

- Private sector wages grew by 0.8%, while public sector wages rose by 0.7% over the quarter.

- The WPI including bonuses stepped down through the year to 3.5% (from 3.8%).

- The WPI today was consistent with our internal data –Australia is not facing a wage-price spiral.

- The Q4 22 WPI printed below the RBA’s updated forecasts from the February Statement on Monetary Policy.

- Our call for the RBA is unchanged – based on the RBA’s recent rhetoric we expect two further 25bp rate hikes over the next two months that would take the cash rate to 3.85%.

- However, today’s undershoot on the benchmark wages index in Australia lends weight to the case to pause very soon in the tightening cycle.

Wages growth below the RBA’s latest forecasts

The RBA made a hawkish tilt at the February Board meeting when the Governor stated that, “the Board expects that further increases in interest rates will be needed over the months ahead”. The reference to “not being on a pre-set course” was removed.

The more hawkish rhetoric from the RBA was in response to the Q422 CPI. And it has been maintained over the past two weeks. But since then there have been two key economic releases that could complicate the near-term policy outlook.

The labour force data for January came in softer than anticipated; the unemployment rate lifted to 3.7% (from 3.5% in December). And today the Q4 22 WPI printed below market and RBA expectations.

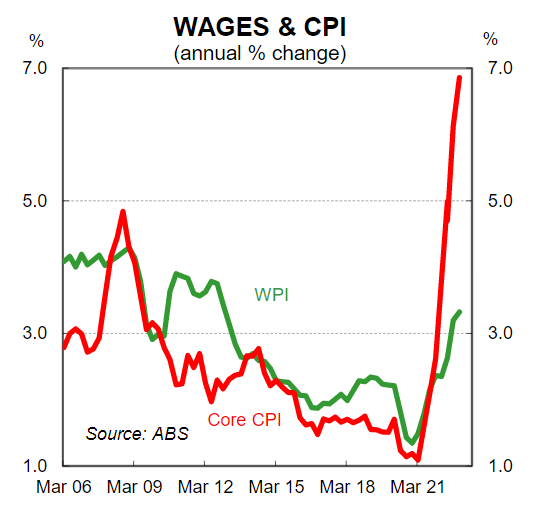

The news should be welcomed by the RBA. More specifically, the Q4 22 WPI was a ‘goldilocks” report that indicates wages pressures are neither too cold nor too hot. Wages in Australia, as measured by the WPI, are simply tracking exactly where the RBA would like them to settle over the medium term.

The 0.8%/qtr increase in the Q4 22 WPI was below our pick and the consensus call of 1.0%/qtr. The annual rate of 3.3% printed below the market median of 3.5% (CBA below consensus at 3.4%). Importantly from a monetary policy perspective the official measure of wages growth came in below the RBA’s expectations (the RBA forecast the WPI to be 3.5%/yr at Q4 22).

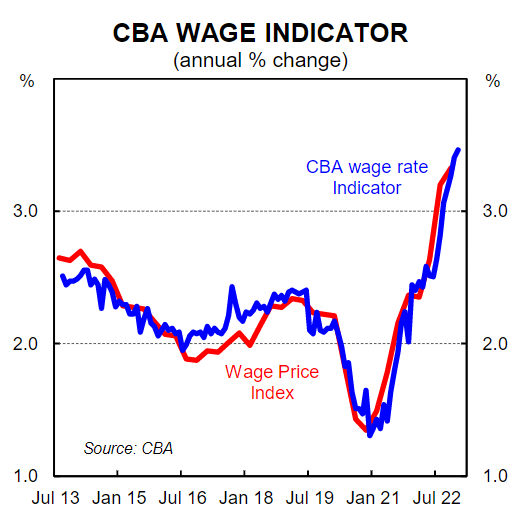

The print today was broadly in line with our internal data which very accurately maps the WPI (see below chart). It indicates wages pressures in the economy have taken time to emerge given the tightness in the labour market.

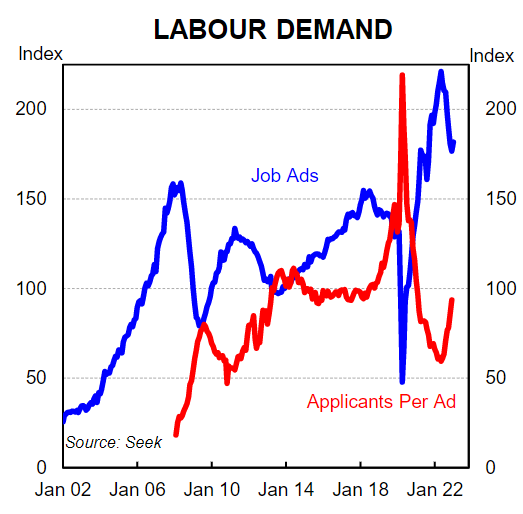

Here we note that peak tightness in the labour market is now behind us. The labour market was at its tightest point in the September quarter 2022. The WPI increased by 1.1%/qtr in Q3 22(revised up from the original 1.0%), helped by the big lift in the Annual Wage Review of between 4.6% and 5.2% by the Fair Work Commission). Since then the flow of migrants and foreign workers into the country has accelerated. At the same time, job advertisements have fallen and the number of applicants per job ad has risen. This dampens wages growth.

Wage increases in the private sector have continued to outpace the public sector over recent quarters, albeit the quarterly growth rates have converged. The 0.8%/qtr increase in private sector wages took the annual rate to 3.6%.

Public sector wages increased by 0.7%/qtr over Q4 22 and the annual rate stepped up a touch to 2.5%. Wage increases for public servants have been held down by long standing wages caps. But many of these are currently now being revised higher.

The WPI including bonuses stepped down to 3.5% (from 3.8% in Q322). The data is not seasonally adjusted so we don’t focus on the quarterly read and it is the annual rate that matters. Over the past year firms have made greater use of bonuses and discretionary payments rather than adjusting base pay upwards. Such an approach avoids ‘locking in’ higher pay.

This is very important when considering the outlook for inflation. Firms that have used bonuses and other one-off payments to reward, retain and attract workers rather than upwardly adjusting base pay have not had a permanent upward adjustment in input costs. As demand in the economy slows these payments can be wound back. A wage-price spiral occurs when base pay is resetting upwards in line with inflation, not when greater use of discretionary payments are made when the economy has boomed and the labour market was tight, as was the case in 2022.

The WPI has its limitations. And it is not the only measure of labour costs. But the WPI is still the benchmark for wages growth in Australia. It enables us to better understand what is occurring across the whole economy with respect to wages inflation in a way that most of the other survey measures of labour costs do not (they are influenced by changes in superannuation, headcount, hours worked, absenteeism, job shifting, promotions and discretionary payments).

We retain our base case that the annual rate of wages growth will peak at 3.8% in mid-2023. We do not share the RBA’s central scenario that the annual rate of wages growth will lift to 4.2%. As such, we expect inflation to subside more quickly than the RBA.

In summary, Wednesday’s report should be interpreted as good news. On one hand it may not seem as such given real wages are deeply negative. Workers in Australia have gone backwards. But the wages dynamics right now in Australia mean that the RBA can pursue their objective of keeping the economy on an ‘even keel’.

The RBA does not need to generate a meaningful lift in the unemployment rate to bring inflation down given wages growth is consistent with the inflation target. The lagged impact of the already delivered rate hikes will slow the economy in 2023 and inflation pressures will abate.

There is still a very large number of home borrowers that will roll off ultra-low fixed rate home loans onto significantly higher mortgage rates in 2023. This means there is more tightening to come for the Australian household sector irrespective of how much higher the RBA takes the cash rate. There is a key risk now that the RBA is tightening policy into a labour market and economy that is already showing sufficient signs of softening.