Advertisement

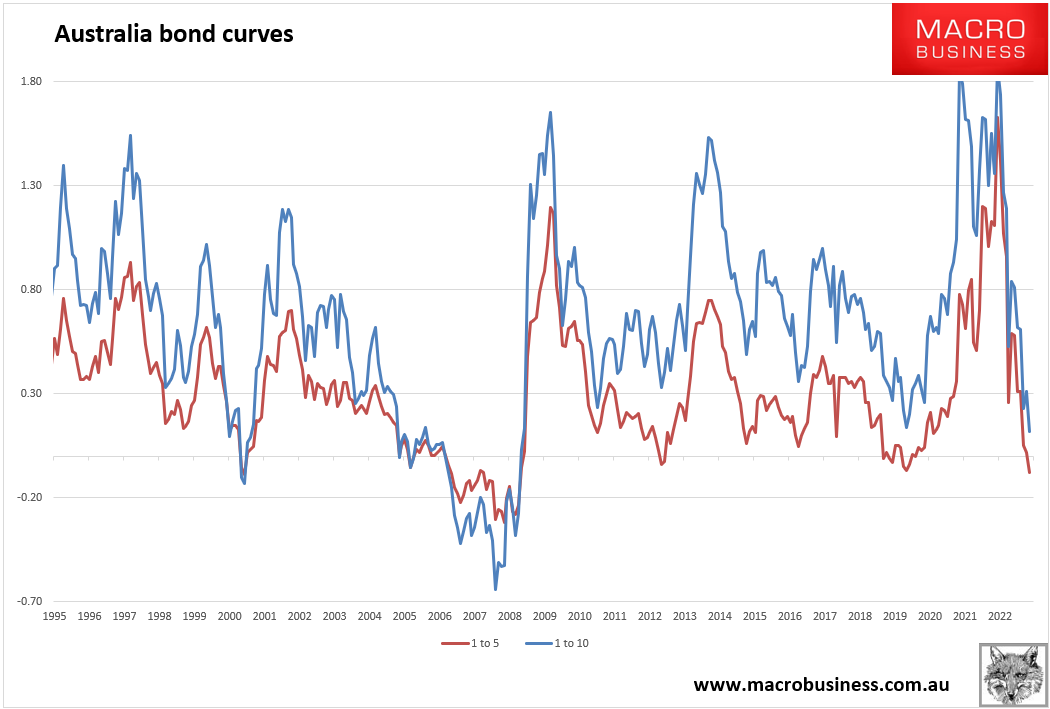

The Australian bond market is grinding its way to reality. The 1-5 year curve is now the most inverted it has been since the pre-GFC period. Recall that this chart is great predictor of per capita recession:

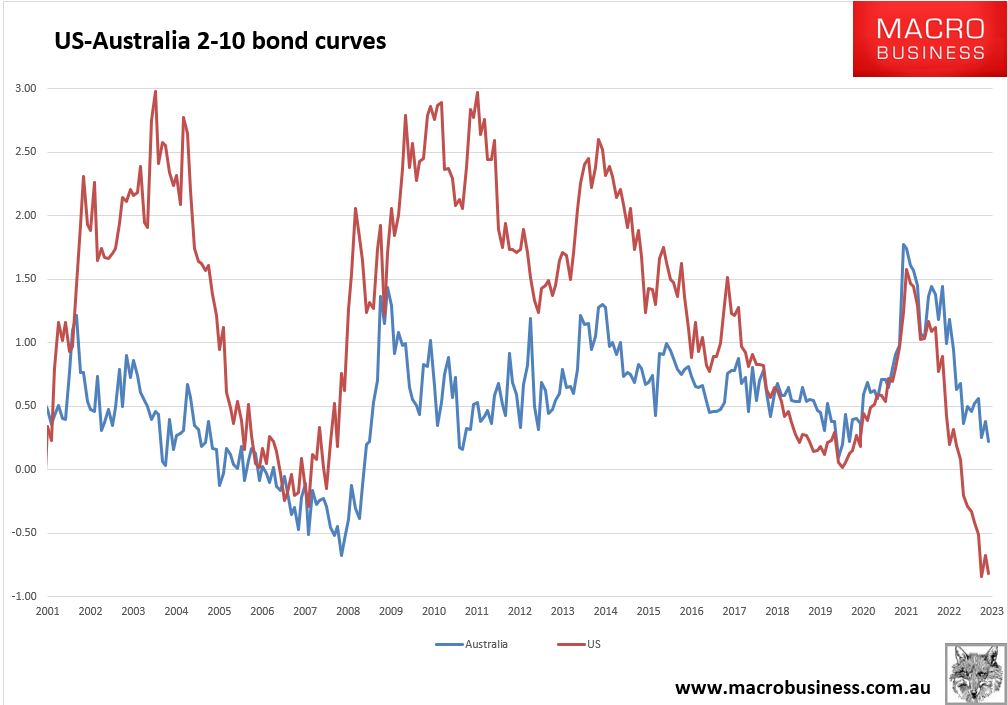

The 2-10 year curve is also at new flats of 22bps, though still has a lot of catching to do with the thoroughly recessionary US:

Advertisement

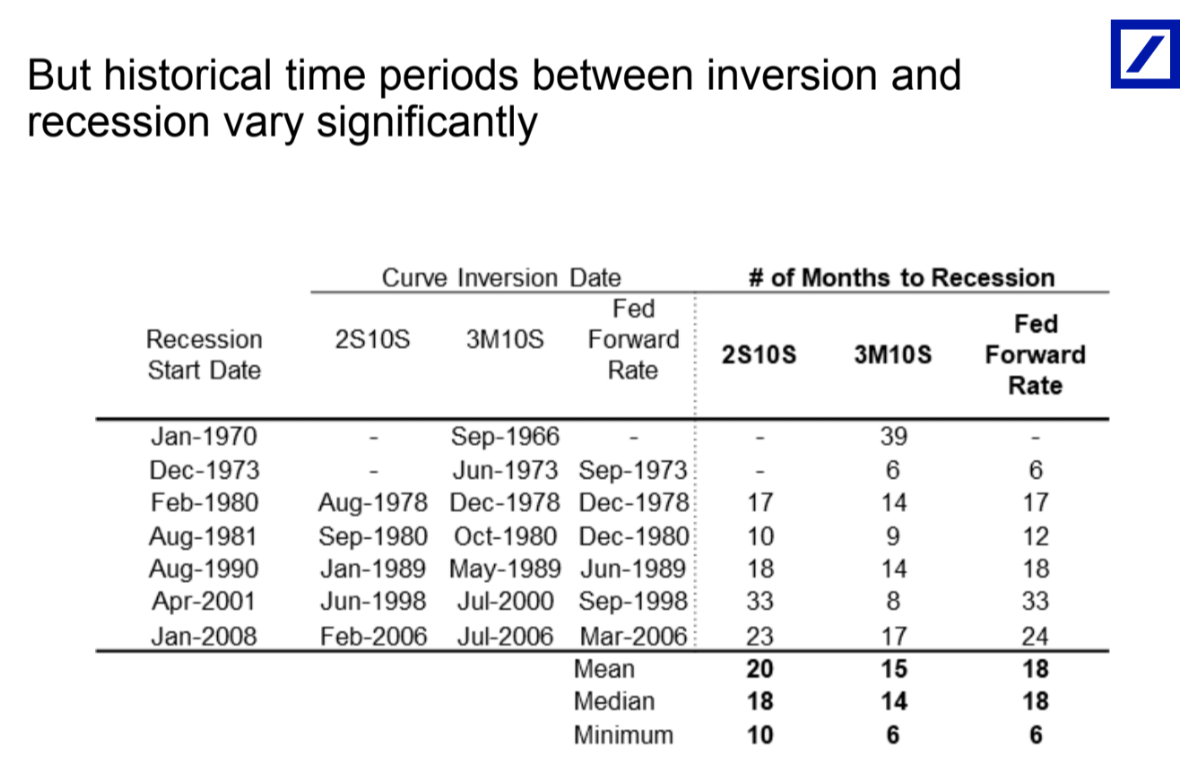

But, be warned, recessions take time:

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.