Advertisement

Slowly but surely sense is developing in Aussie bond curves.

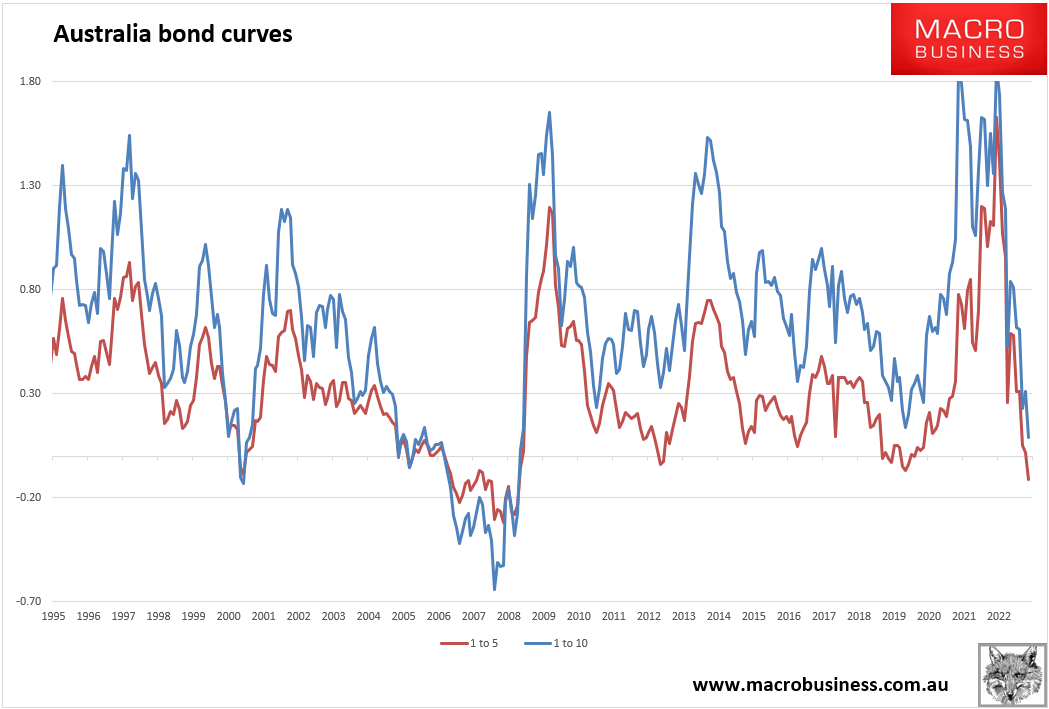

Australian yields are now inverted from the one year past seven years. The 1-5 is the most inverted since the GFC and 1-10 is as well. The 1-5 is an especially good predictor of per capita recession:

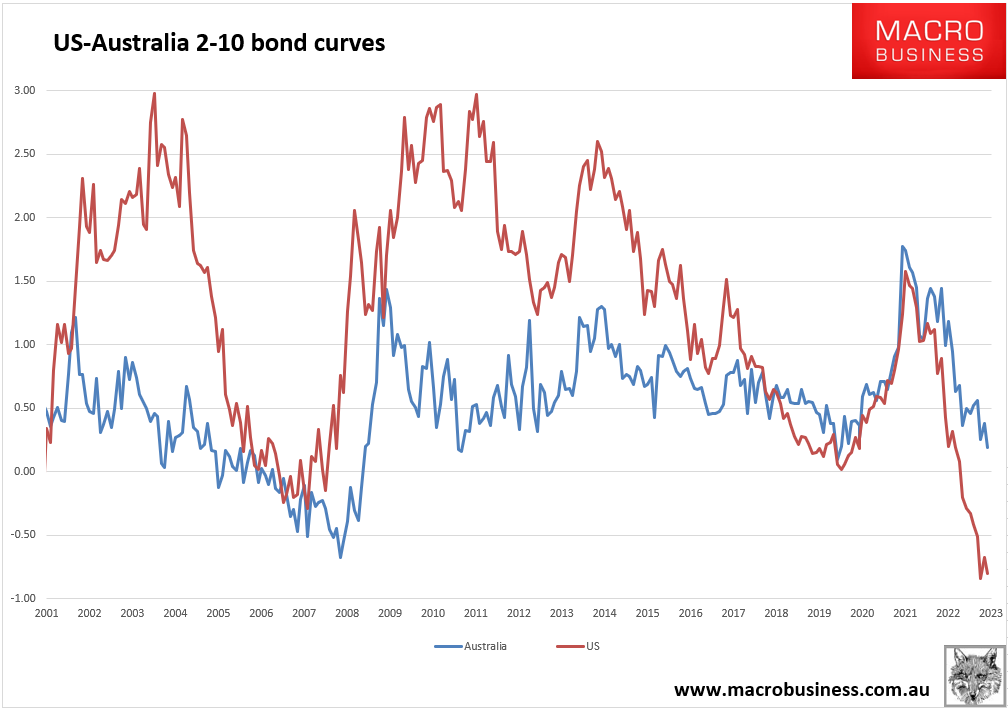

Moreover, the 2-10 curve is flattening sharply again, now just 19bps away from hard landing territory:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.