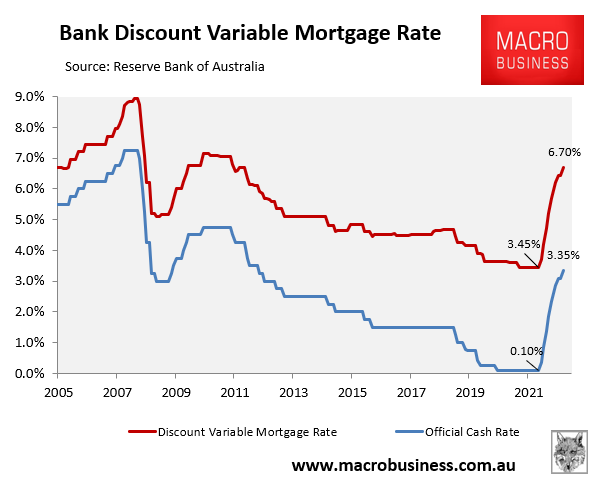

As expected, the Reserve Bank of Australia (RBA) has lifted the official cash rate (OCR) another 25 basis points to 3.35% – the highest level since September 2012.

This has taken the indicator discount variable mortgage rate 6.70%, up from 3.45% in April 2022:

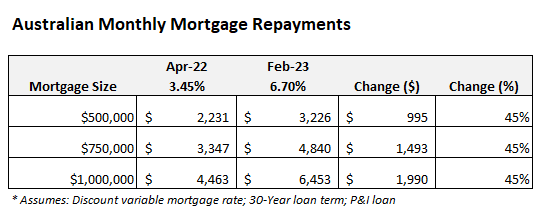

Once the increase is fully passed onto mortgage holders, variable mortgage repayments will have risen around 45% from their pre-tightening level:

For a borrower paying the indicator discount variable mortgage rate on a $500,000 mortgage, monthly repayments will have risen by around $1,000 from their pre-tightening level.

In coming to its decision, RBA governor Phil Lowe noted that Australian inflation is too high:

In Australia, CPI inflation over the year to the December quarter was 7.8 per cent, the highest since 1990. In underlying terms, inflation was 6.9 per cent, which was higher than expected. Global factors explain much of this high inflation, but strong domestic demand is adding to the inflationary pressures in a number of areas of the economy.

Inflation is expected to decline this year due to both global factors and slower growth in domestic demand. The central forecast is for CPI inflation to decline to 4¾ per cent this year and to around 3 per cent by mid-2025. Medium-term inflation expectations remain well anchored, and it is important that this remains the case.

Lowe also noted that Australia’s labour market remains very tight, with wage growth accelerating:

The labour market remains very tight. The unemployment rate has been steady at around 3½ per cent over recent months, the lowest rate since 1974. Job vacancies and job ads are both at very high levels, but have declined a little recently. Many firms continue to experience difficulty hiring workers, although some report a recent easing in labour shortages. As economic growth slows, unemployment is expected to increase. The central forecast is for the unemployment rate to increase to 3¾ per cent by the end of this year and 4½ per cent by mid-2025.

Wages growth is continuing to pick up from the low rates of recent years and a further pick-up is expected due to the tight labour market and higher inflation. Given the importance of avoiding a prices-wages spiral, the Board will continue to pay close attention to both the evolution of labour costs and the price-setting behaviour of firms in the period ahead.

However, Lowe acknowledged that “monetary policy operates with a lag and that the full effect of the cumulative increase in interest rates is yet to be felt in mortgage payments”. Moreover, some households “are experiencing a painful squeeze on their budgets due to higher interest rates and the increase in the cost of living”.

Lowe stated that “the Board expects that further increases in interest rates will be needed over the months ahead to ensure that inflation returns to target and that this period of high inflation is only temporary”.

Before concluding that “the Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that”.

Thus, there are likely to be further rate hikes over coming months.