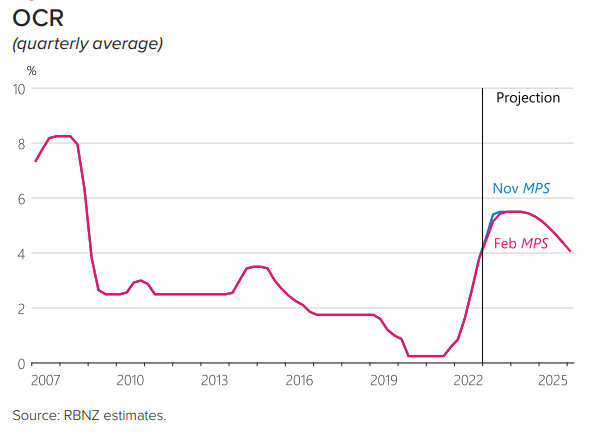

On Wednesday, the Reserve Bank of New Zealand (RBNZ) lifted the official cash rate (OCR) another 0.5% to 4.75%.

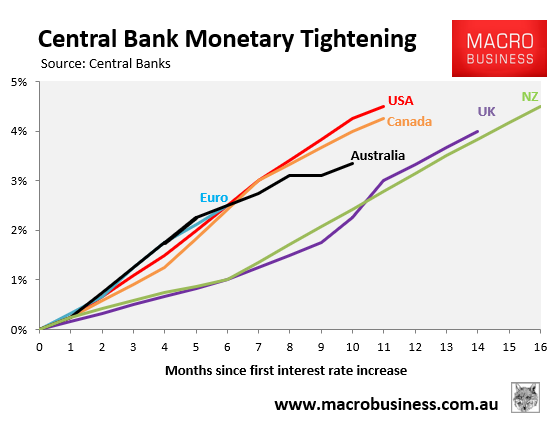

This took New Zealand’s official interest rate to the one of the highest levels in the developed world:

In its Statement of Monetary Policy (SoMP) accompanying Wednesday’s release, the RBNZ forecast that it would lift the OCR to a peak of 5.5%:

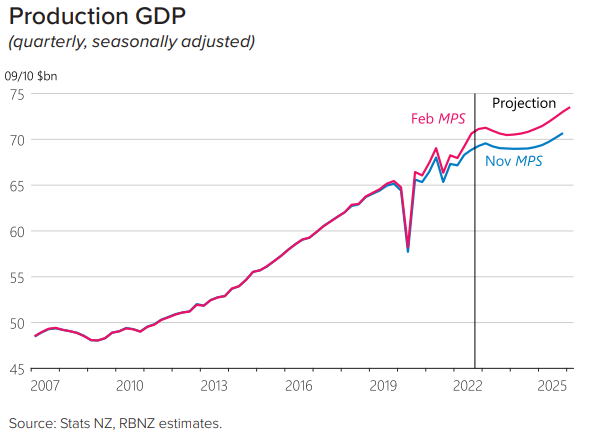

In doing so, the RBNZ said that it intends to drive the economy into recession in order to bring inflation back to its target level.

Specifically, the RBNZ forecasts a “peak-to-trough decline in the level of GDP over 2023… [of] about 1 percent”.

“While this recession is assumed to be spread over several quarters from the middle of this year, there is considerable uncertainty about the timing”, the SoMP notes.

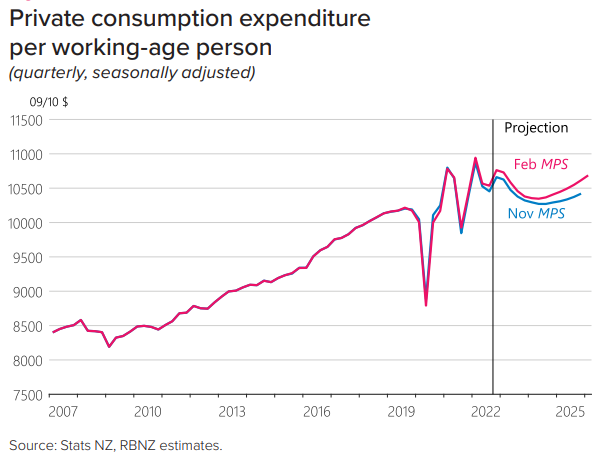

This decline in GDP will be driven by shrinking household consumption spending.

The RBNZ notes that “higher interest rates, lower house prices and a weaker labour market are expected to lower household consumption over coming years, with per-person consumption assumed to return to around its pre-pandemic level over the projection”:

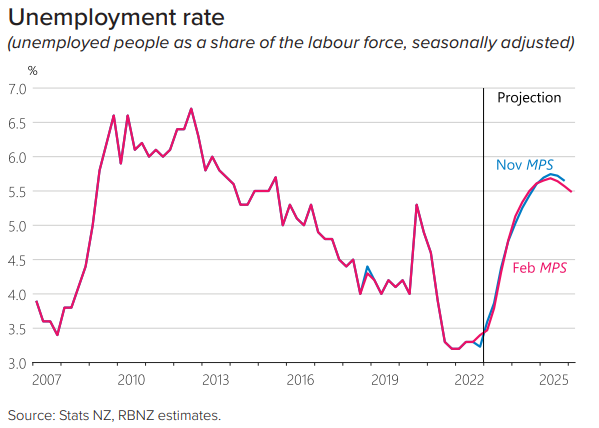

Indeed, New Zealand’s unemployment rate is projected to soar by around 2% over the forecast period:

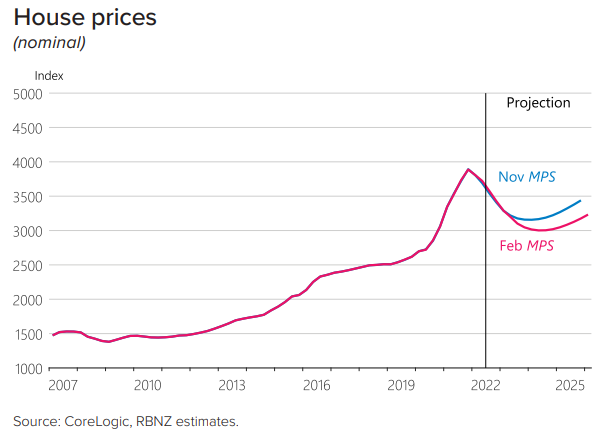

The RBNZ also notes that “house prices have declined by around 15 percent to date” and projects they will “fall by about 23 percent in total from their peak by 2024”:

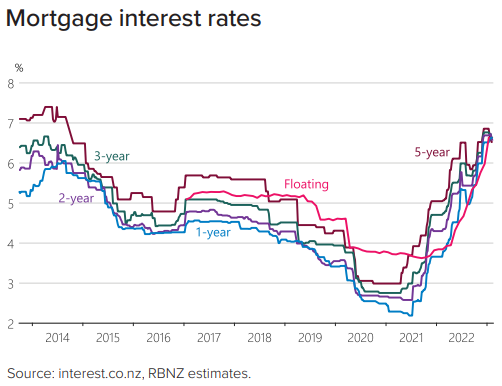

Curiously, the SoMP doesn’t explicitly mention the fixed rate mortgage reset that will hit in 2023.

According to Westpac, more than half of New Zealand’s mortgage book will this year reset from ultra-cheap pandemic fixed rate mortgages to rates that are at least double current levels:

Therefore, there is already significant tightening built-in to New Zealand’s financial system, and the RBNZ risks going too far if it continues to hikes rates.

A deep recession cannot be ruled-out.