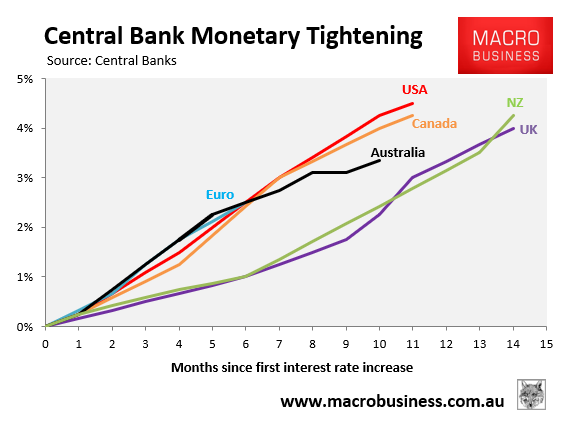

The Reserve Bank of New Zealand (RBNZ) has been among the world’s most aggressive central banks with respect to hiking interest rates.

The RBNZ has already hiked its official cash rate by 4.0% since it commenced its tightening cycle in October 2021:

And most pundits expect the RBNZ to raise rates again by 0.5% at its upcoming monetary policy meeting on Wednesday.

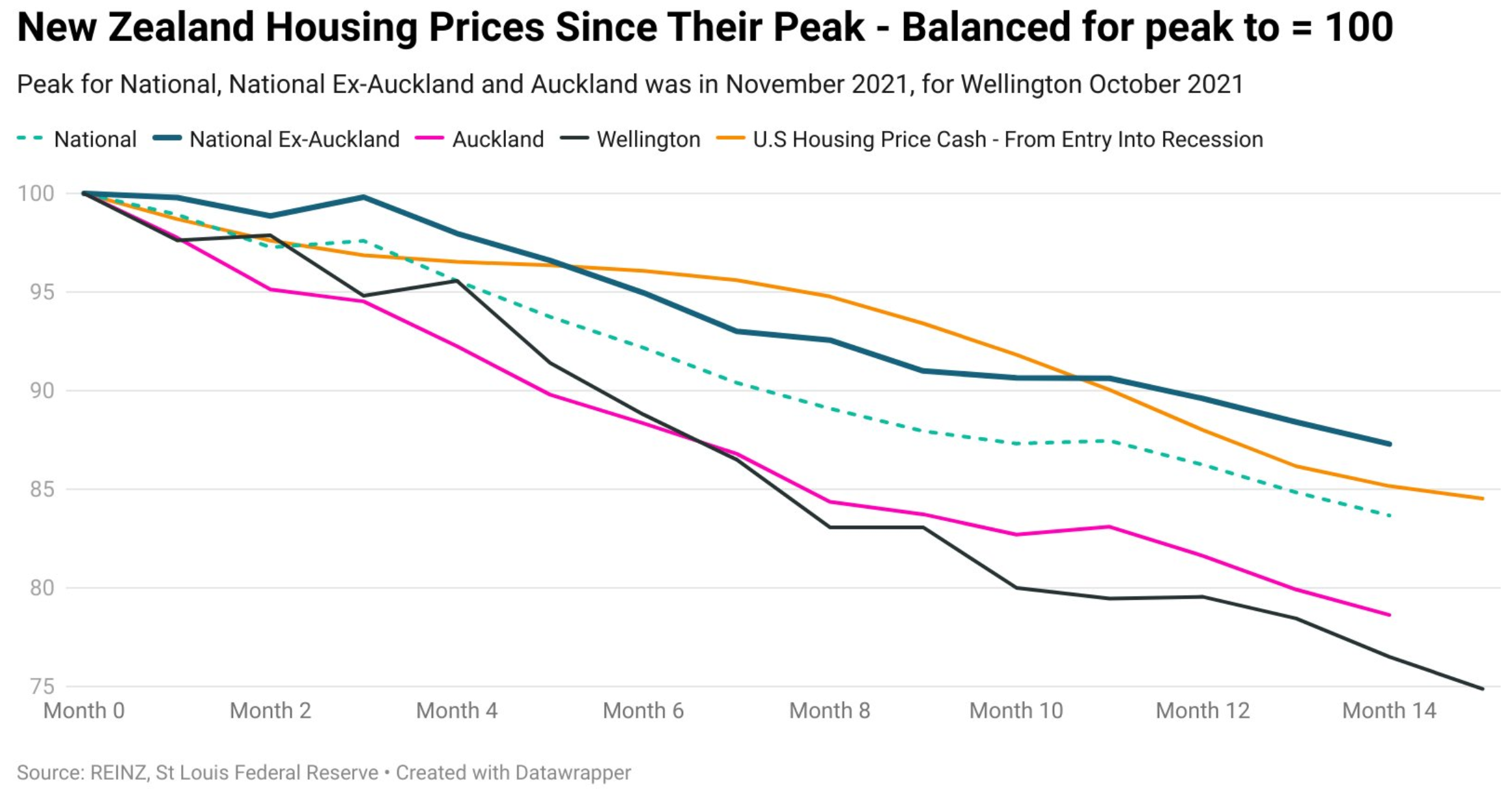

The RBNZ’s aggressive monetary tightening has already seen national house prices fall by 16.3% from their November 2021 peak:

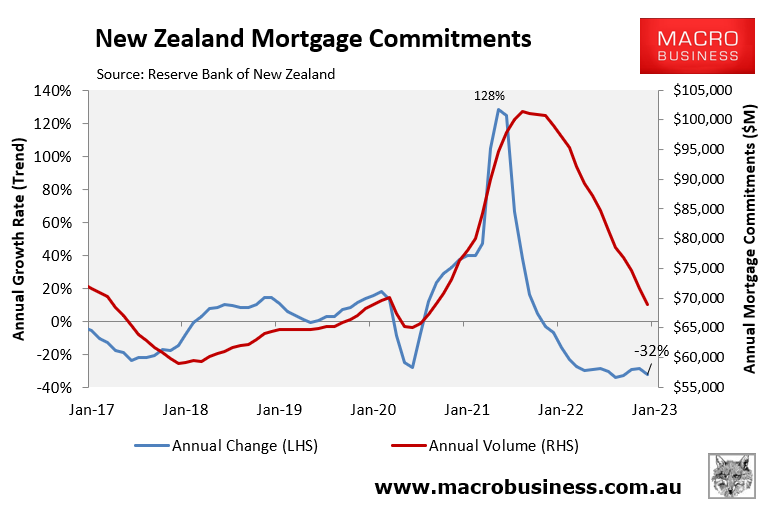

These rate hikes have also shrunk mortgage demand, with the value of commitments collapsing 32% year-on-year in December:

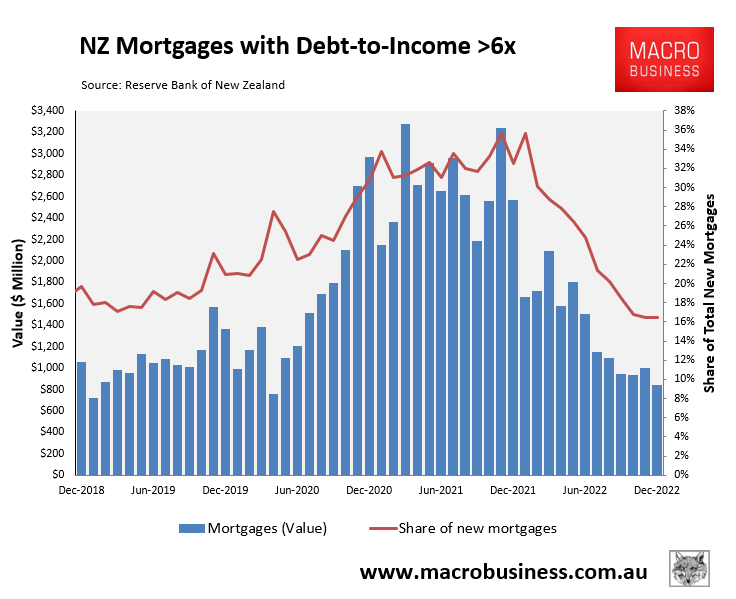

Now, the RBNZ has released data showing the amount of mortgage debt new borrowers are taking on relative to their incomes has plunged to their lowest level on record.

As illustrated in the next chart, the share of new mortgage borrowers with a debt-to-income ratio above six has more than halved from peaks of 36% in November 2021 and January 2022 to just 16% in December 2022:

Needless to say, the RBNZ would be happy with this turn of events.

Its aggressive rate hikes have clearly scared the life out of mortgage borrowers causing them to become far more risk averse. In the process, the stability of New Zealand’s financial system is improving, while the heat is also being taken out of demand-side inflation.

Given around 50% of New Zealand’s mortgage book will this year reset from ultra-cheap pandemic fixed rate mortgages to rates that are at least double current levels, there is further tightening already built-in.

Thus, the RBNZ should be nearing the end of its rate hiking cycle.