A lot has been written about the fixed rate “mortgage cliff” confronting Australia in 2023 as an estimated 880,000 borrowers shift from ultra-cheap fixed mortgages originated over the pandemic to variable mortgages with rates more than double current levels.

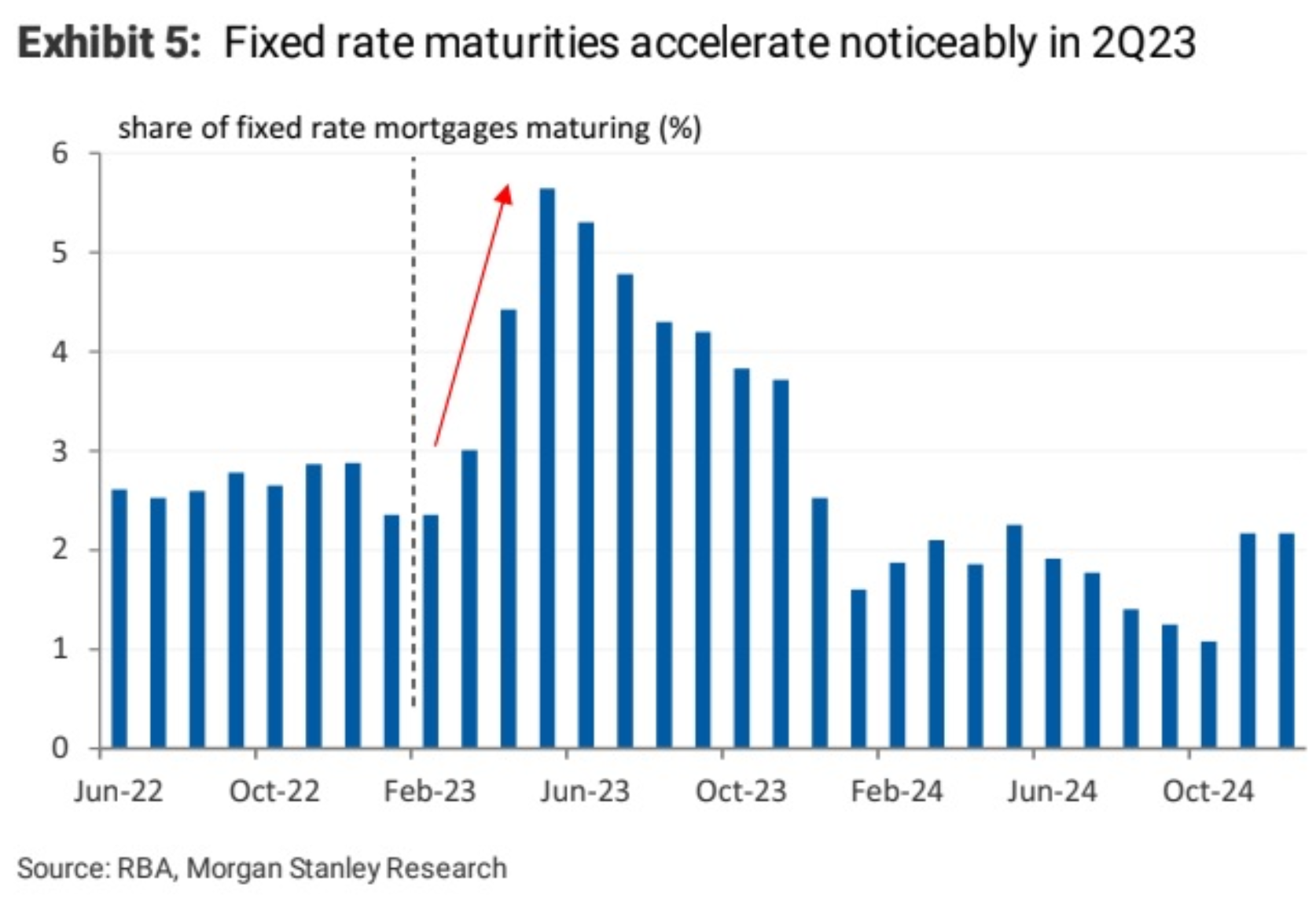

The next chart from Morgan Stanley illustrates this fixed rate “mortgage cliff”.

As you can see, the volume of fixed rate mortgages expiring will rise precipitously from April, peak in May, and then remain at elevated levels throughout the remainder of this year:

Following 10 consecutive rate hikes from the Reserve Bank of Australia (RBA), mortgage rates have already risen beyond 3 percentage points for many borrowers, which is the minimum serviceability buffer required by APRA in assessing whether someone can repay their loan.

As a result, many thousands of borrowers risk being pulled underwater as their fixed rate terms expire over the remainder of the year.

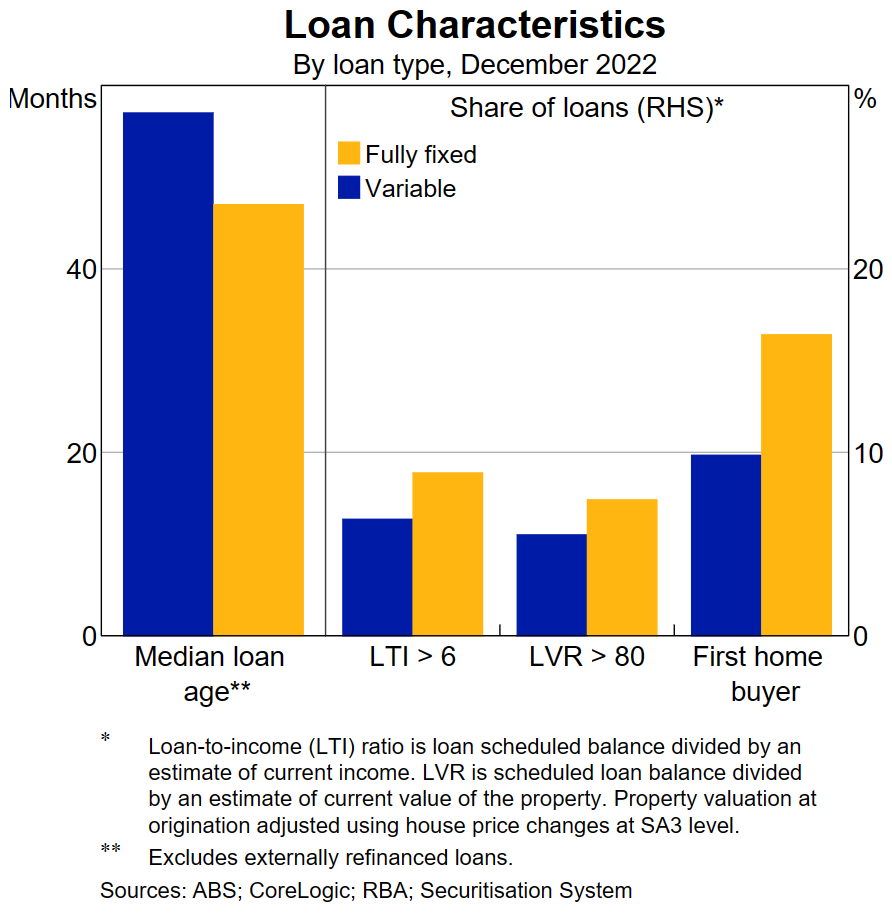

The RBA’s latest Bulletin on fixed rate borrowing shows that Australia could actually be facing a sub-prime “mortgage cliff”, since fixed rate loans tend to be far riskier than their variable couterparts:

As shown above, fixed rate loans are more likely to be held by younger borrowers with minimal equity (e.g. first home buyers), as well being more highly leveraged.

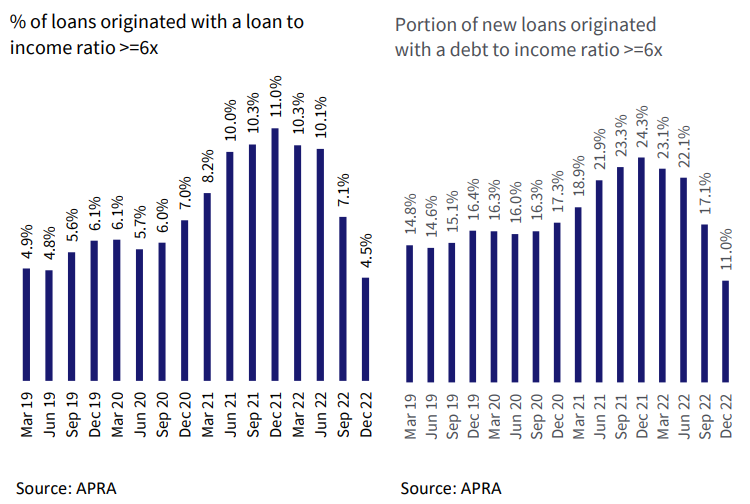

It is no coincidence that the share of mortgages originated with high loan-to-value ratios hit a record high over the pandemic:

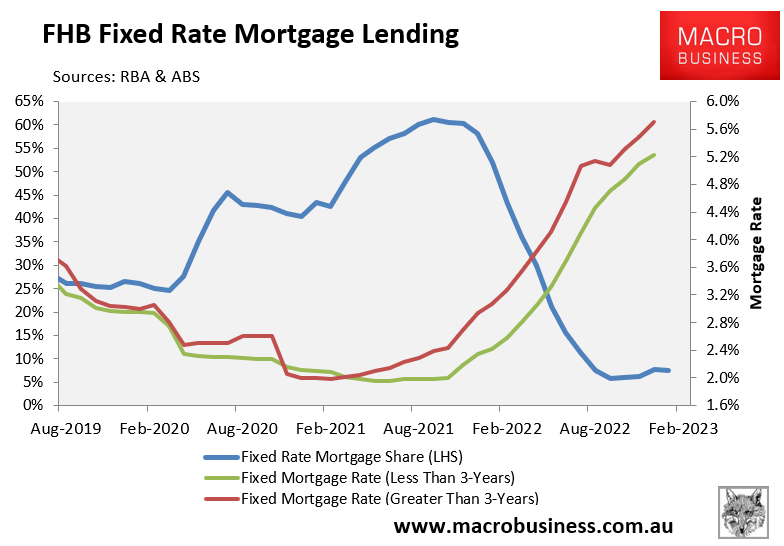

Much of this would have been first home buyers on fixed rate mortgages, which hit a record high 60% share in 2021:

Soon the piper will have to be paid, with huge numbers of highly leveraged first home buyers facing a doubling to tripling of their mortgage rates.

Some will be in negative equity because prices have fallen below their purchase cost.

And many will not be able to refinance to cheaper rates because they no longer meet lenders’ serviceability criteria.