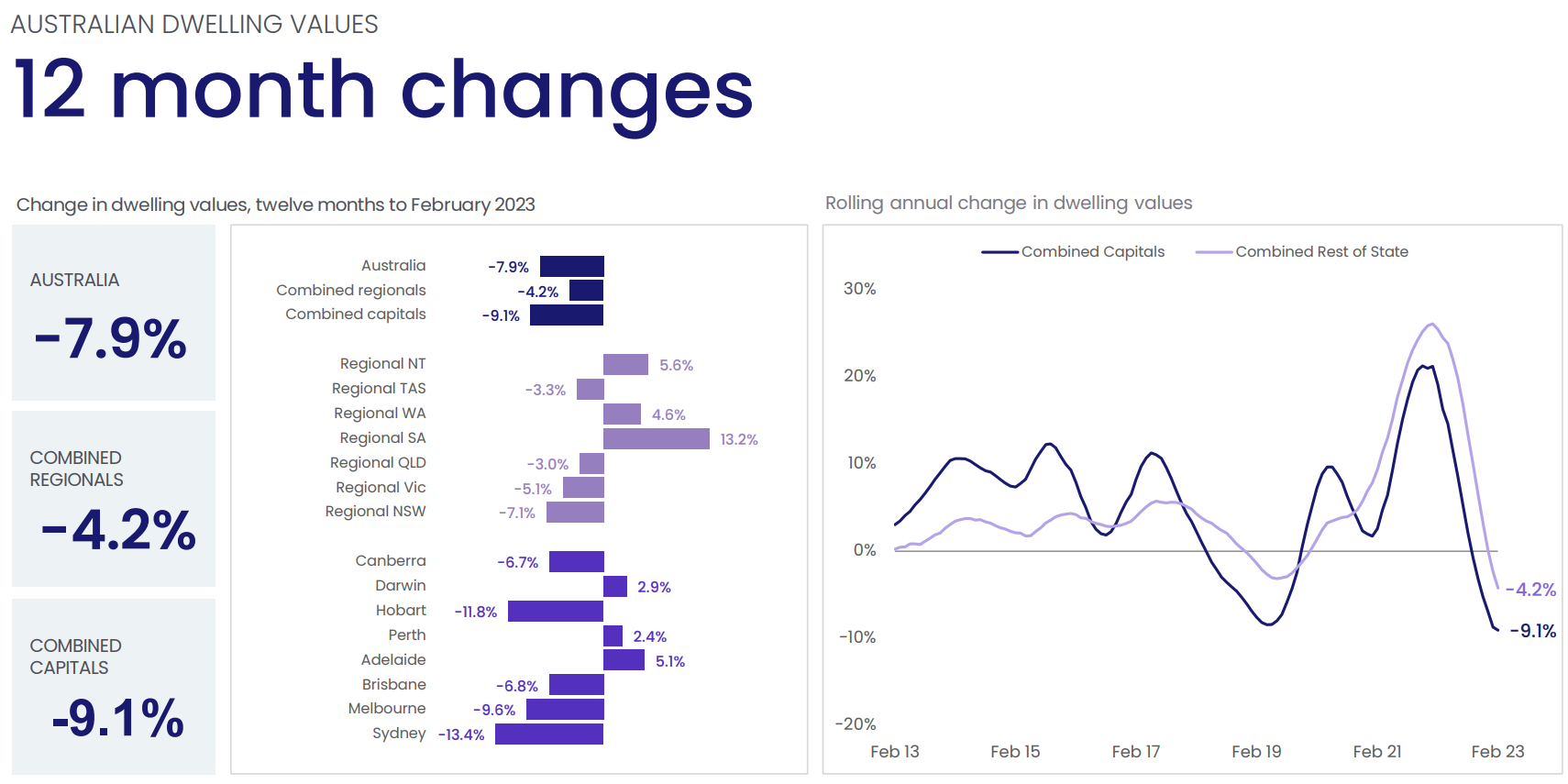

CoreLogic has released its Monthly Chart Pack, which notes that dwelling values nationally were down 7.9% over the 12 months to February, “the largest annual decline on record”:

The combined value of residential real estate in Australia was $9.3 trillion at the end of February, which is down $700 billion from its peak of $10 trillion in April 2022 immediately before the Reserve Bank of Australia’s (RBA) first interest rate hike.

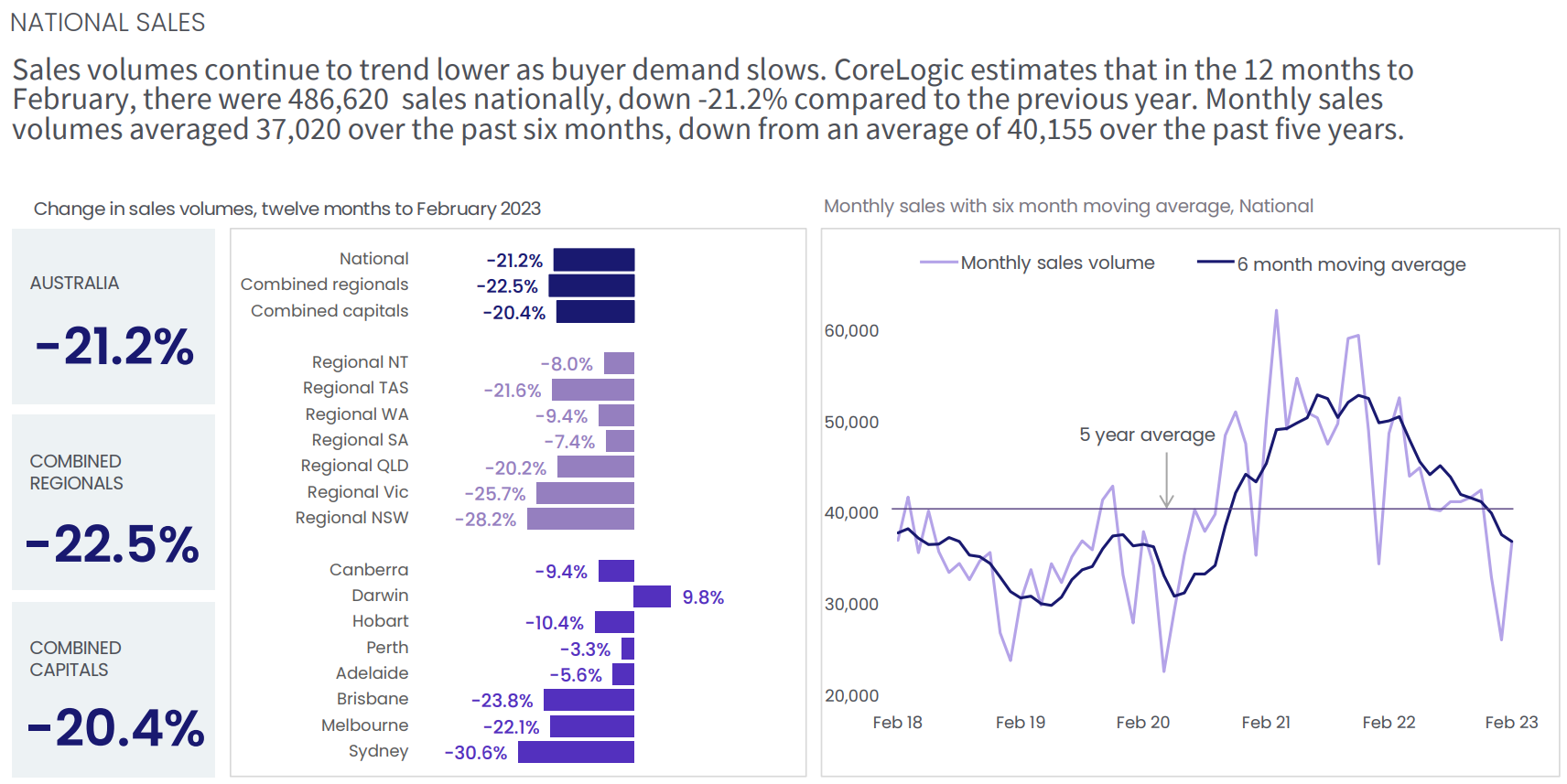

Sales volumes continue to trend lower as buyer demand slows.

CoreLogic estimates that in the 12 months to February, there were 486,620 sales nationally, down 21.2% compared to the previous year:

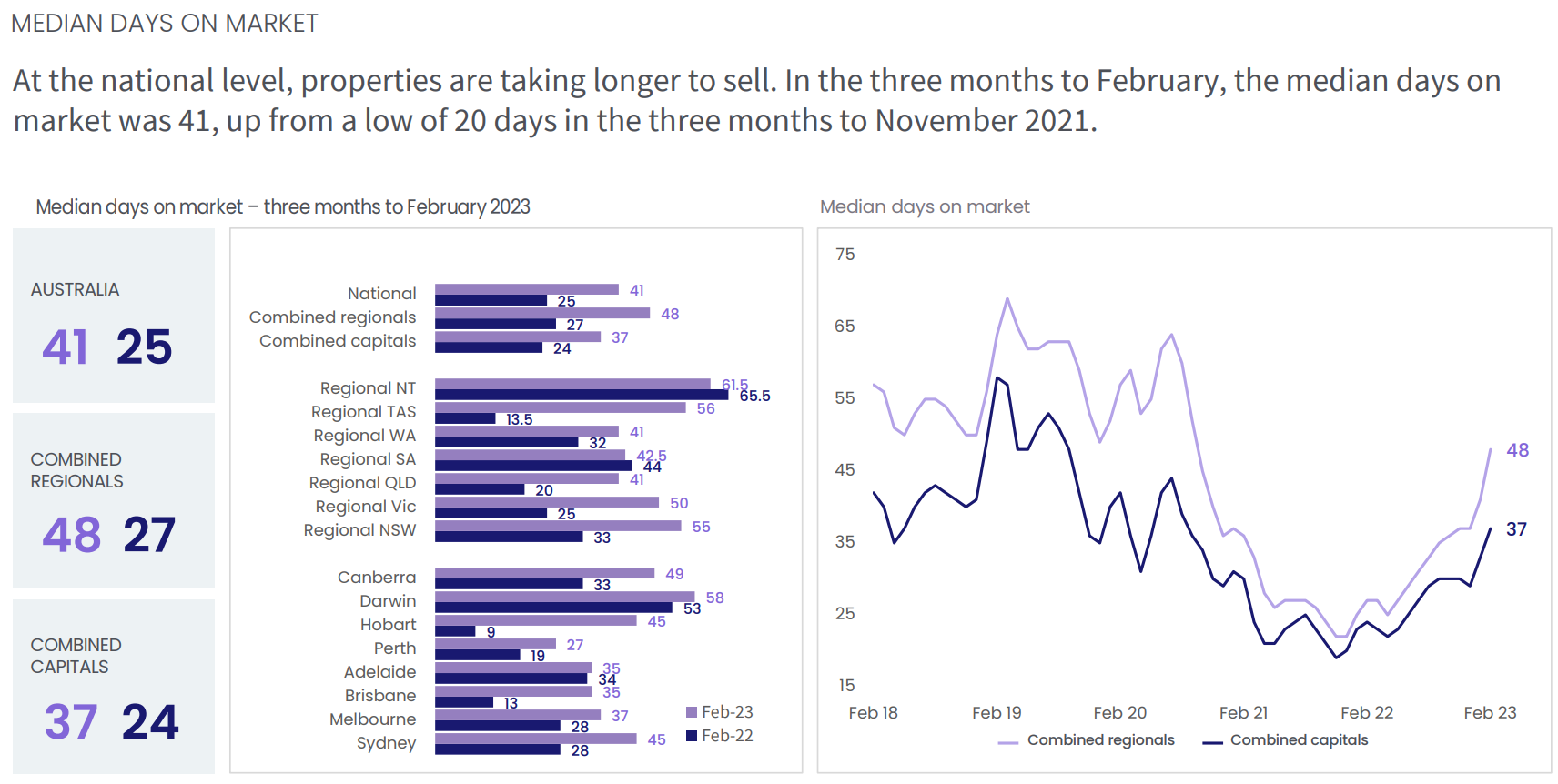

Properties are also taking longer to sell. In the three months to February, the median days on market was 41 nationally, up from a low of 20 days in the three months to November 2021:

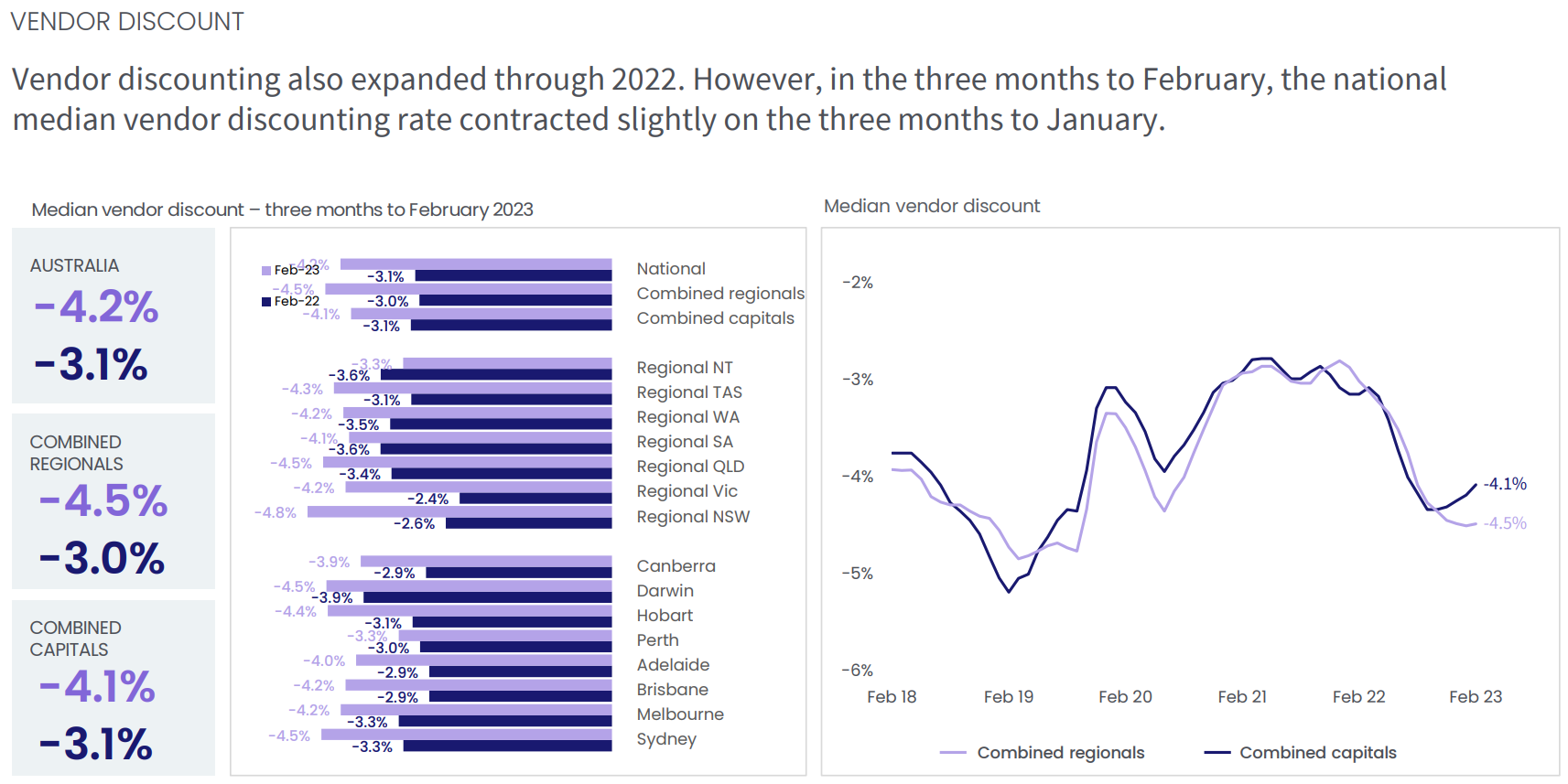

Vendor discounting also expanded through 2022. However, in the three months to February, the national median vendor discounting rate contracted slightly on the three months to January:

Logically, the market should soften further given the RBA’s latest rate hikes in February and March, which have further reduced borrowing capacity.

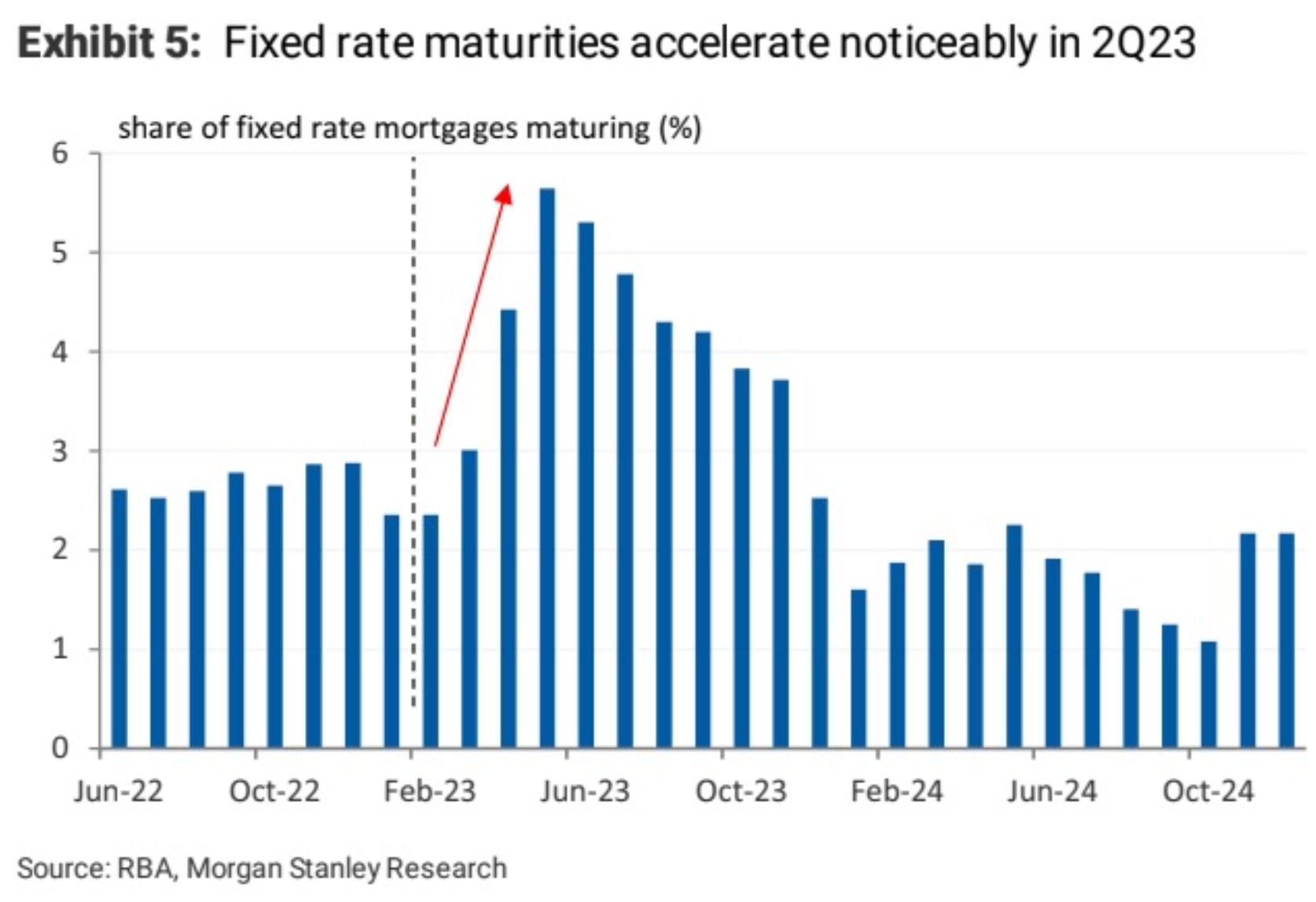

The fixed rate mortgage reset, which will gather steam over the next three months (see above chart), should also see an increase in forced sales, which will weigh on prices.