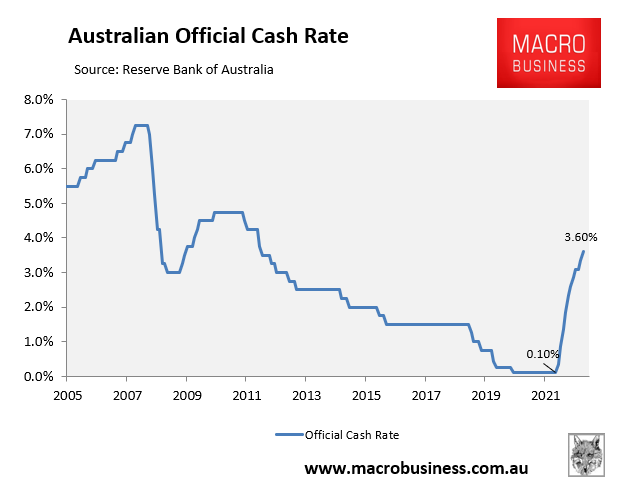

The Reserve Bank of Australia (RBA) on Tuesday lifted the official cash rate (OCR) another 0.25%, the 10th consecutive hike.

This brought the OCR to 3.60%, its highest level since 2012:

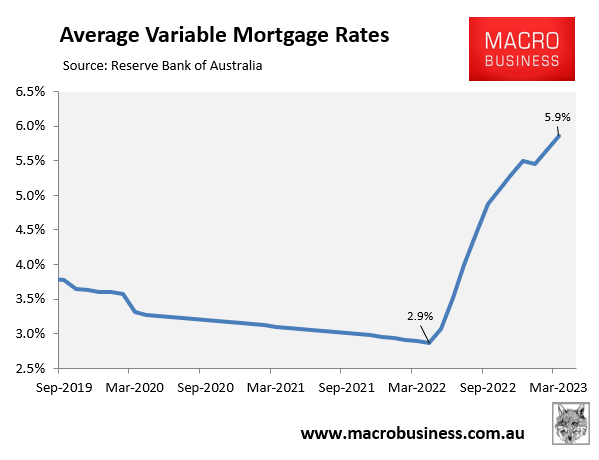

The increase in the OCR has more than doubled average owner-occupier variable mortgage rates from 2.9% in April 2022 to 5.9%:

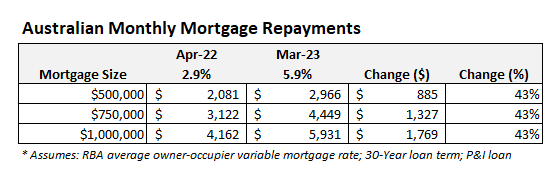

The impact on mortgage holders has been brutal, with average variable mortgage repayments soaring 43% from their pre-pandemic level, adding around $900 in monthly mortgage repayments on a typical $500,000 mortgage:

While the minutes accompanying Tuesday’s decision took a more dovish tone, the RBA indicated that interest rates will rise further in the months ahead.

This is a worrying prospect, given monetary conditions will tighten significantly even without further rate hikes from the RBA.

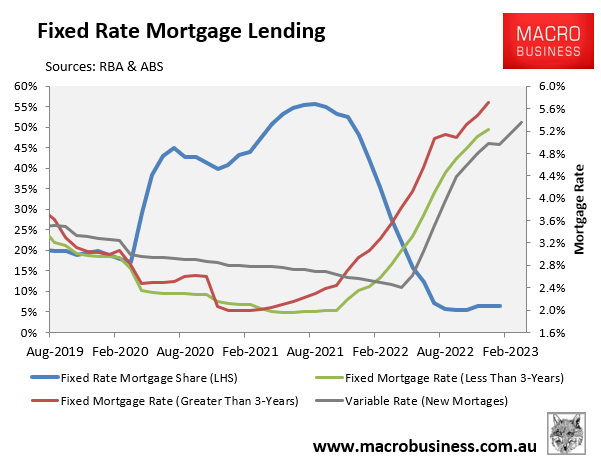

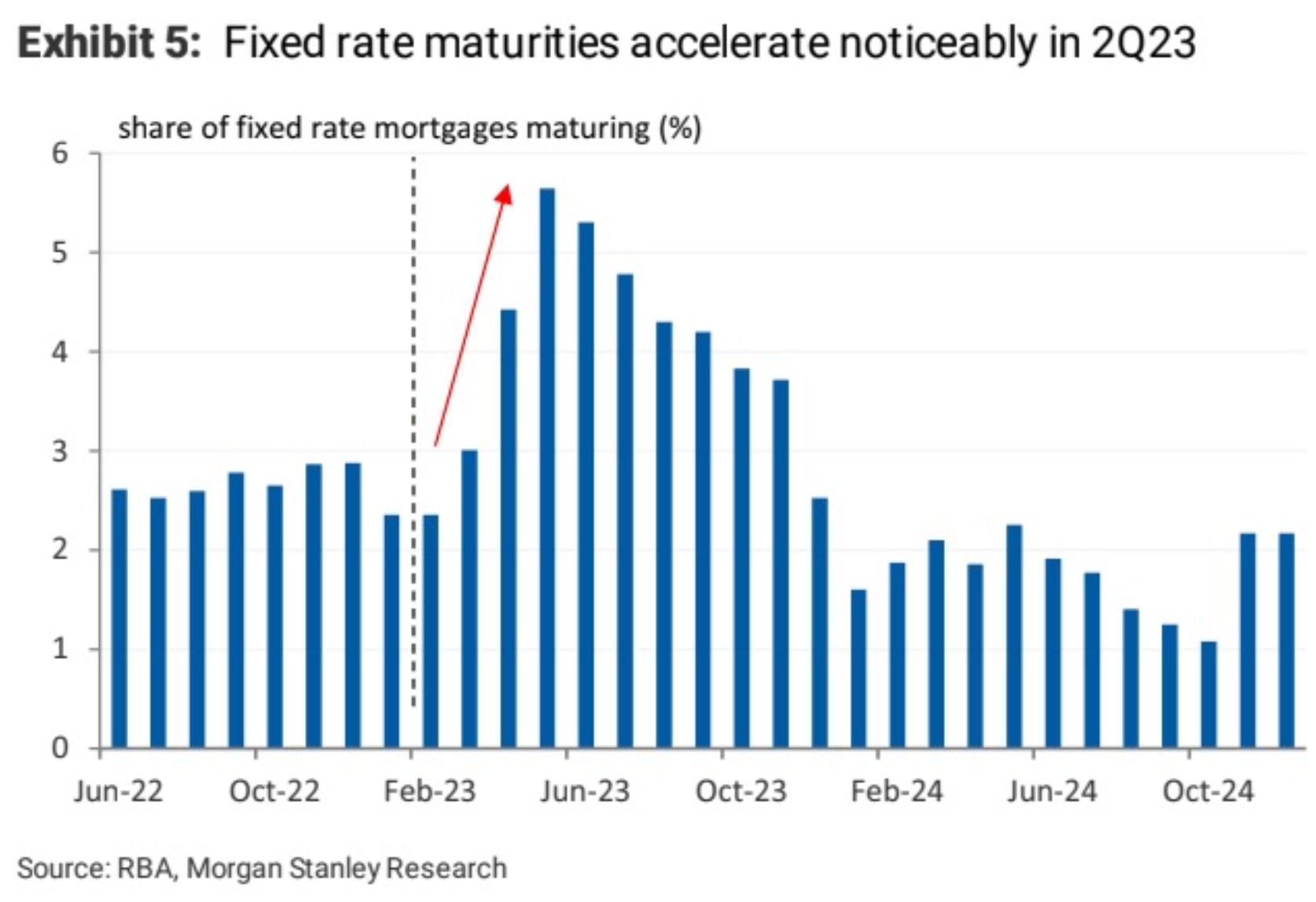

According to RBA’s own estimates, around one third of all home loan borrowers are on fixed mortgages, many of which were originated over the pandemic at rates of around 2%:

Nearly 900,000 borrowers, or 23% of Australia’s total mortgage book, will this year switch from these cheap pandemic fixed rates to variable mortgages with rates that are more than double current levels.

The next chart from Morgan Stanley highlights the extent of this fixed rate “mortgage cliff”, with the volume of fixed rate mortgages expiring rising precipitously from April, peaking in May, and then remaining at high levels for the remainder of the year:

Given the size of the monetary tightening to come, which comes at a time when the economy is slowing and unemployment is rising, the RBA is playing with fire on interest rates.

If it continues to tighten over the months ahead, it risks plunging the economy into a consumer-led recession.