Property investors bleeding cash as mortgage costs soar

What a difference a year makes.

A year ago, property investors were enjoying rock bottom interest rates, prices had just gone through their biggest boom in generations, and many landlords were enjoying neutral or positive cash flow.

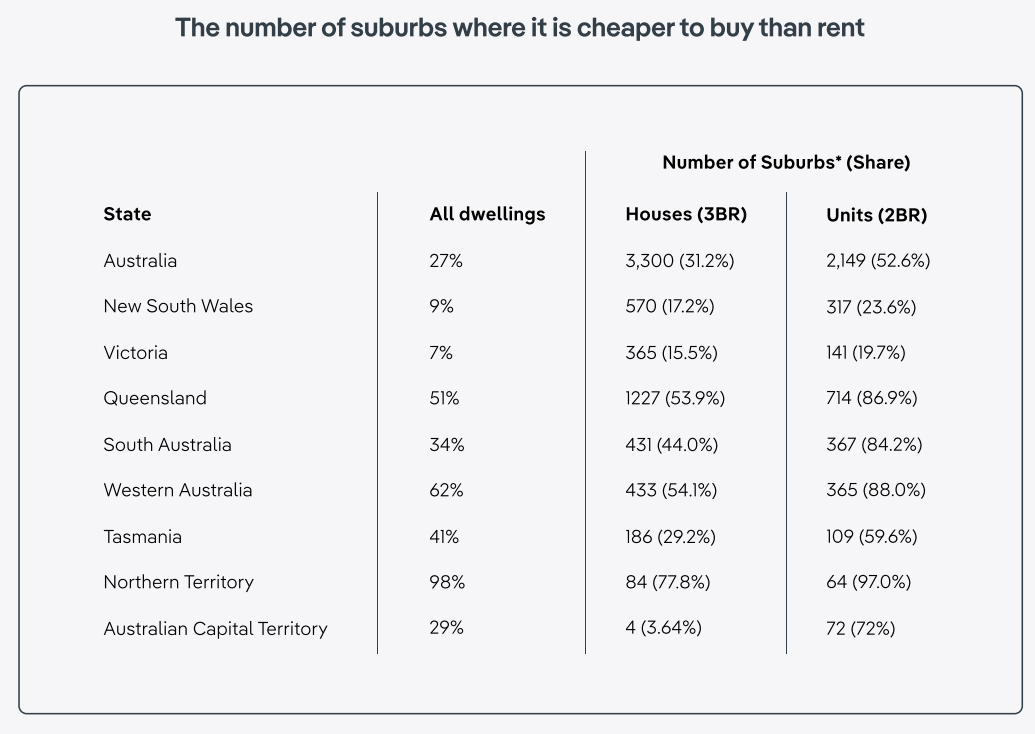

Stories dominated the media about how it was cheaper to buy than rent across many Australian suburbs:

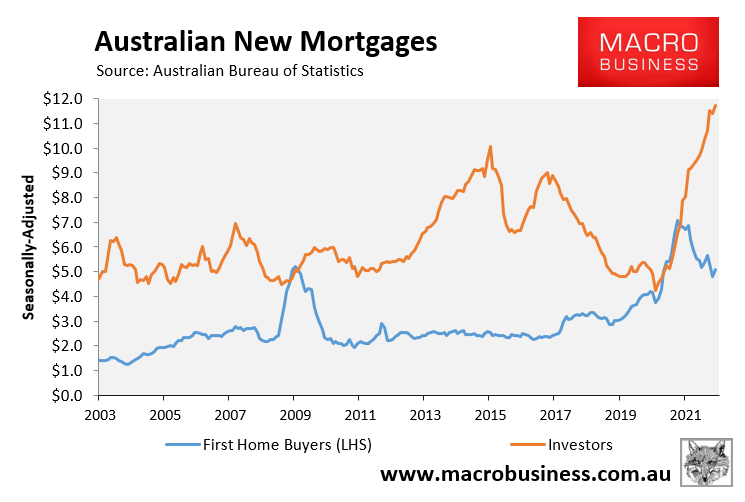

Accordingly, investors were piling into the market at a record pace (chart from March 2022):

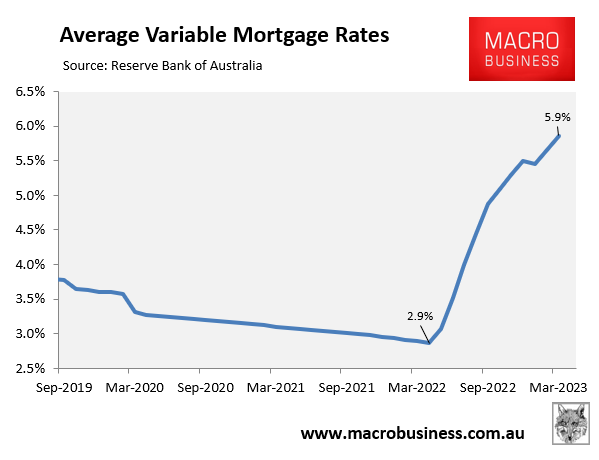

Fast forward to now and the situation has reversed. Mortgage rates have doubled on the back of 10 consecutive rate hikes from the Reserve Bank of Australia:

And property investors are now struggling with mortgage repayments far exceeding the increase in rents, which is forcing many to sell.

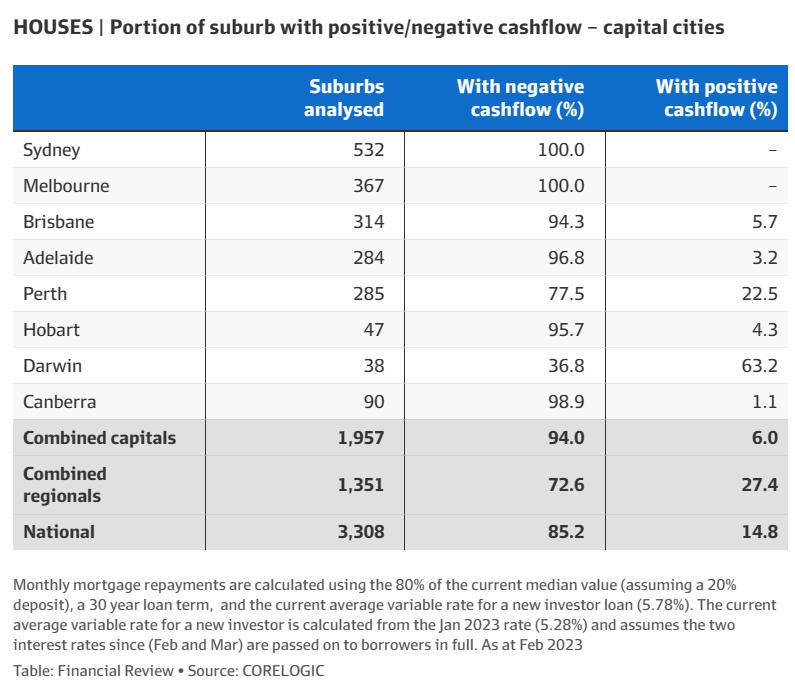

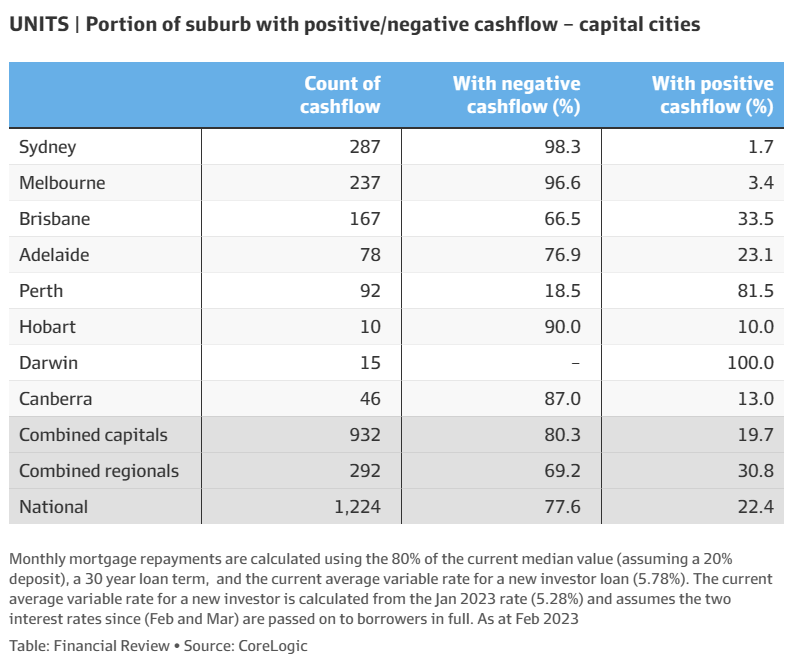

100% of suburbs with house rental markets and more than 97% of suburbs with unit markets in Melbourne and Sydney are cashflow negative, according to CoreLogic:

Accordingly, more than 30% of homes for sale across Australia are now property investors, up from 20% to 30% previously.

“Landlords have been pushing rents higher to offset the rising cost of debt, but there is a limit to what the market can absorb, and we are close to that now”, says CoreLogic’s research director, Tim Lawless.

For example, a Sydney investor with a $1.2 million house for rent and a $960,000 mortgage is spending around $30,000 more a year in costs than they receive in rents, which is forcing increasing numbers to sell their properties, according to The AFR.

In Melbourne, the annual shortfall for a median investment property worth about $900,000 is $22,000.

The pressure on highly leveraged investors will increase in the short-term as the tidal wave of borrowers that took out cheap fixed rate loans over the pandemic reset to variable rates that are double or triple their current levels.

There is also the prospect that the Reserve Bank of Australia will increase rates further in coming months.

Looking further ahead, the conditions facing property investors will improve markedly.

The Reserve Bank is likely to start cutting rates late this year, which will reduce mortgage costs and send prices higher.

Rental growth should also remain strong on the back of record immigration and sluggish housing supply.

While 2023 is rough for property investors, 2024 is set to return to boom times.