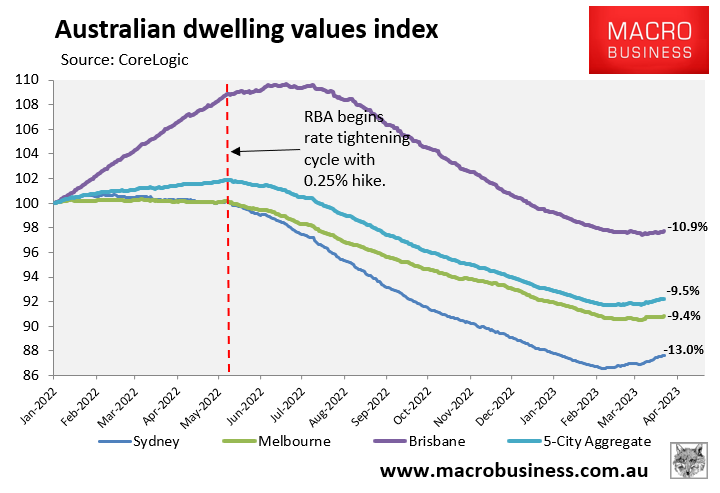

Australia’s house price rebound continues in the face of the Reserve Bank of Australia’s (RBA) ten consecutive interest rate hikes.

Since bottoming on 7 February, CoreLogic’s daily dwelling values index has rebounded 0.6% at the 5-city level, led by a 1.2% rise across Sydney:

This rebound is extraordinary because it has arrived despite a 0.25% rate hike in early February and another 0.25% rise in early May, which has further restricted borrowing capacity.

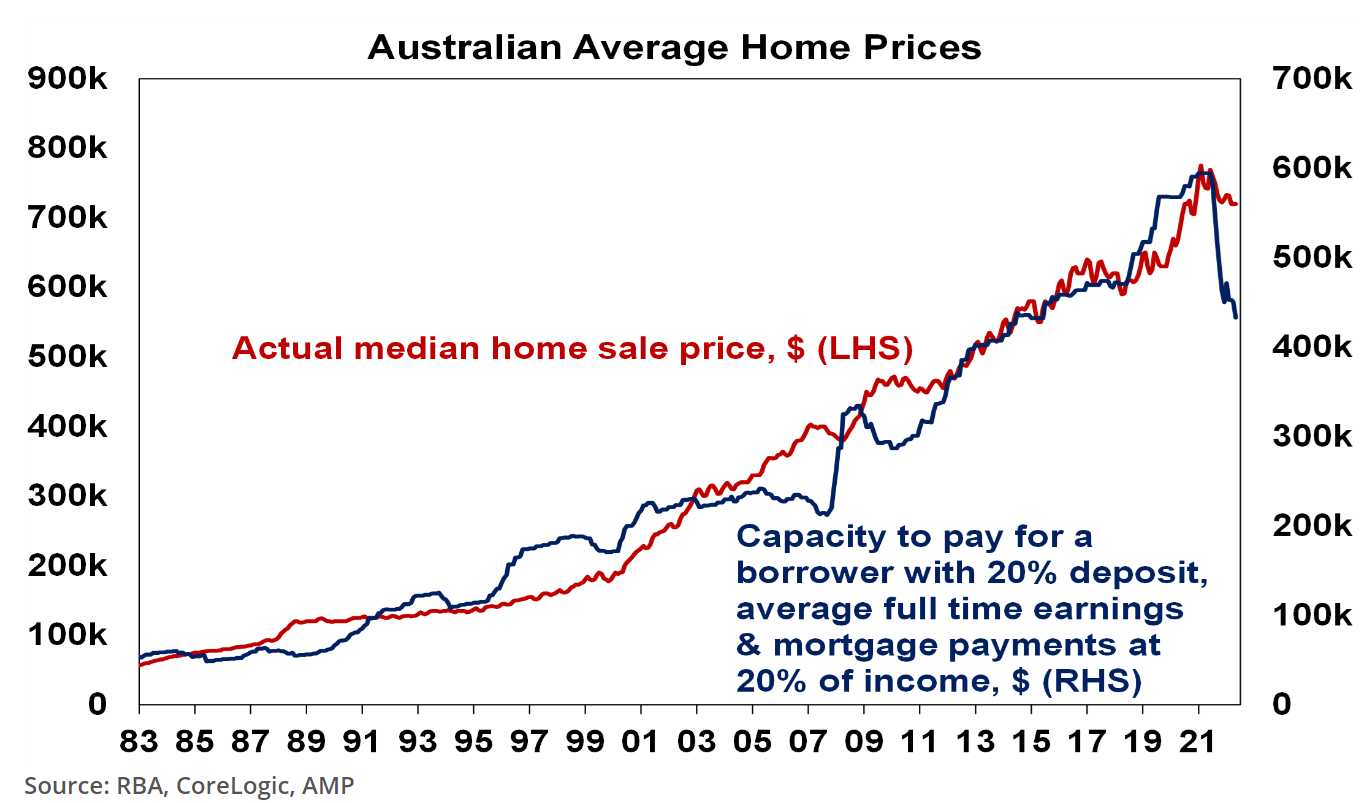

Indeed, a new housing market analysis from AMP Capital’s chief economist, Dr Shane Oliver, explains that borrowing capacity has fallen by around 27% in response to the RBA’s ten rate hikes.

This represents the sharpest decline in borrowing capacity on record and would usually be associated with a significant fall in home values:

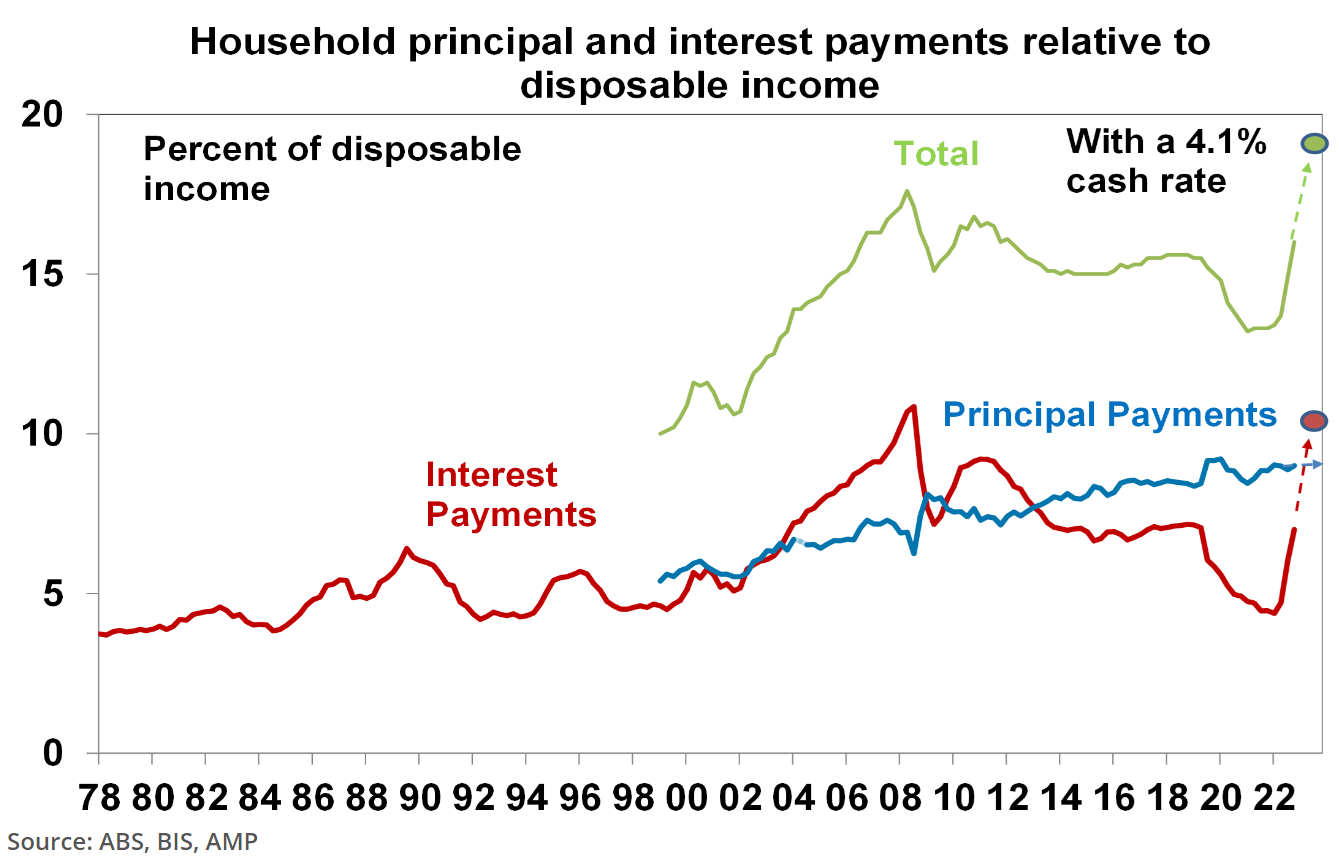

Dr Oliver also shows that “household debt servicing payments as a share of income have already risen to their highest in more than a decade” and “will rise further given the lagged flow through of variable rates and the fixed rate reset”, or if the RBA hikes again:

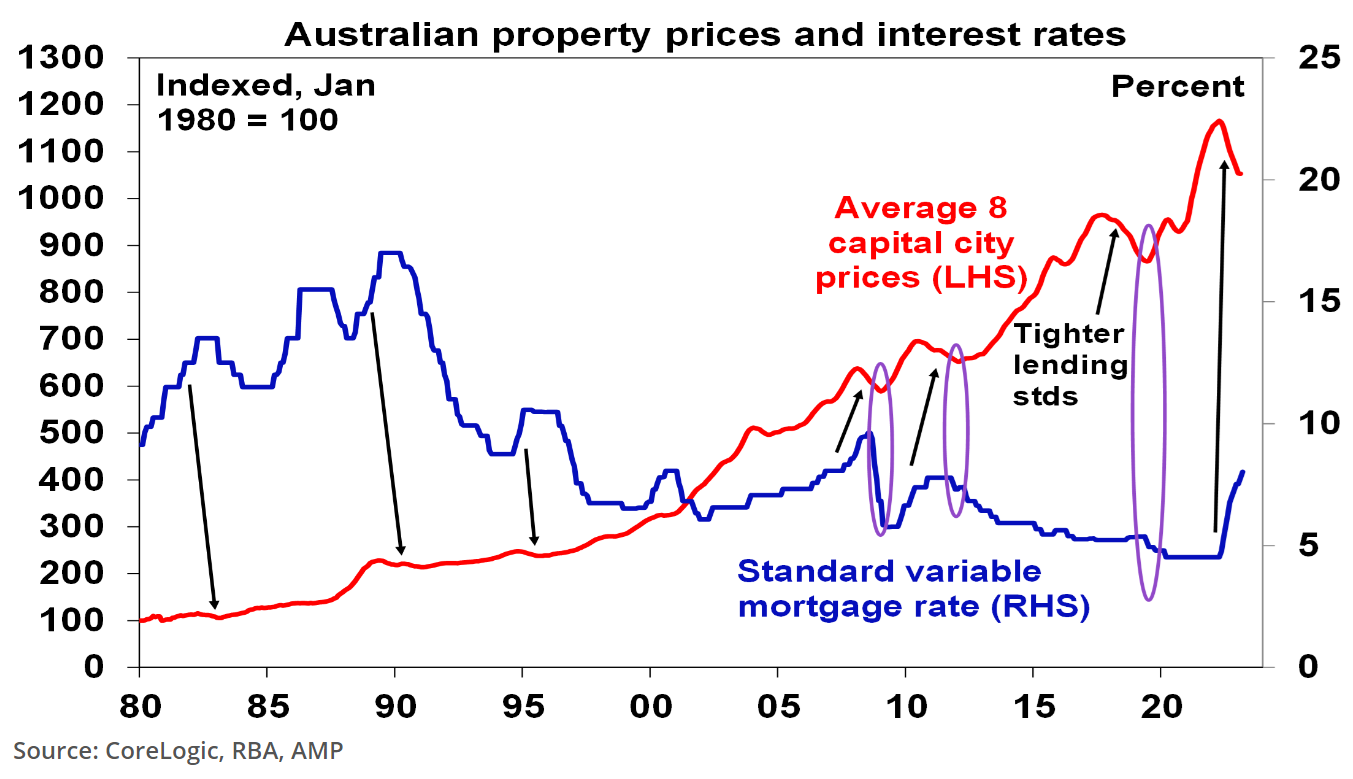

Moreover, “property down cycles into 2009, 2012 and 2019 only saw prices sustainably bottom once interest rates started falling” (see the purple ovals in the next chart), and Dr Oliver believes “rate cuts are still a way off yet”:

Accordingly, Dr Oliver believes the above financial factors “will likely constrain demand and cause a potential increase in supply as some financially stressed homeowners sell”.

The upshot is that Shane Oliver still sees the current house price rebound as “short-lived”, and his base case is for “average home prices having a top to bottom fall of 15-20% to later this year of which we are half way through”.

Dr Oliver also does not “see a sustained recovery until next year”.

That said, Dr Oliver acknowledges that “the current environment is very hard to read” since prices are also being supported by “improving demographic demand, constrained supply and tight rental markets”.

Therefore, “there is a chance that prices have bottomed, particularly if rates have peaked and if the Australian economy has a soft landing”.