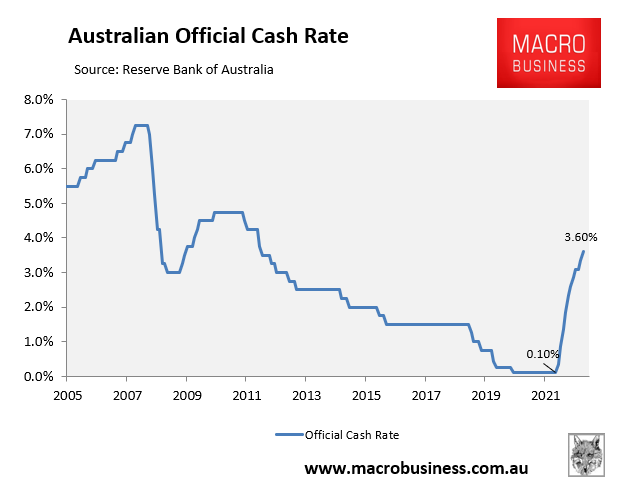

As expected, the Reserve Bank of Australia (RBA) today lifted the official cash rate (OCR) another 0.25% to 3.6%.

This has taken the OCR to its highest level since 2012:

In coming to its decision, the RBA abandoned the prior month’s hawkish commentary in favour of a more dovish tone.

Specifically, the RBA noted that “the monthly CPI indicator suggests that inflation has peaked in Australia” and “the central forecast is for inflation to decline this year and next, to be around 3% in mid-2025. Medium-term inflation expectations [also] remain well anchored”.

It noted that “growth in the Australian economy has slowed” and “household consumption growth has slowed due to the tighter financial conditions and the outlook for housing construction has softened”.

Moreover, “at the aggregate level, wages growth is still consistent with the inflation target and recent data suggest a lower risk of a cycle in which prices and wages chase one another”.

The RBA also “recognises that monetary policy operates with a lag and that the full effect of the cumulative increase in interest rates is yet to be felt in mortgage payments”.

“Household balance sheets are also being affected by the decline in housing prices”.

Nevertheless, the RBA indicated “that further tightening of monetary policy will be needed to ensure that inflation returns to target and that this period of high inflation is only temporary”.

“In assessing when and how much further interest rates need to increase, the Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market”.

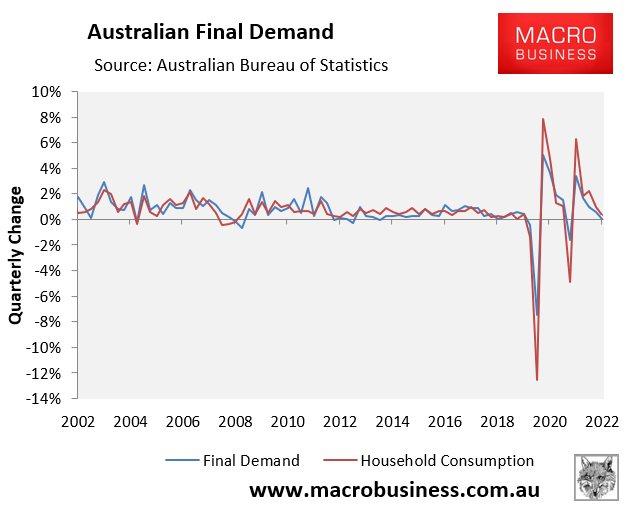

The RBA is clearly playing with fire given household consumption growth – the economy’s main driver – has already plummeted and unemployment is rising.

Monetary conditions are also set to tighten further as nearly one quarter of Australia’s total mortgage book switches from cheap pandemic fixed rates originated over the pandemic at around 2% to variable mortgages with rates more than double current levels.

The RBA risks going too far and plunging the economy into a consumer-led recession.