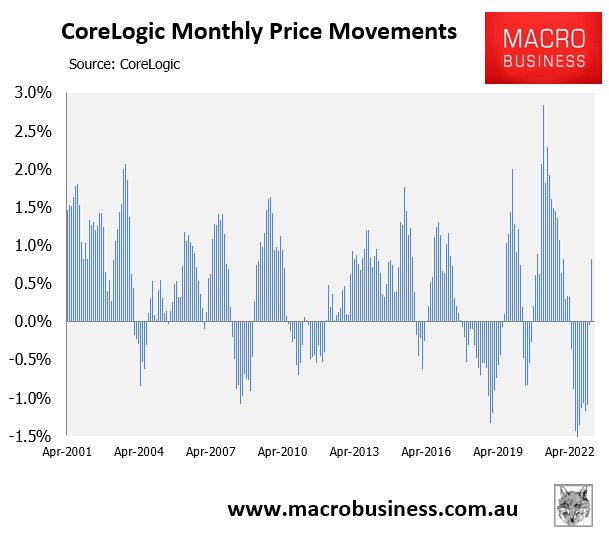

CoreLogic’s daily dwelling values index results for March are out with values rising 0.8% across the five major Australian capital cities:

It was the first monthly rise in values since April 2022, and the largest rise since January 2022.

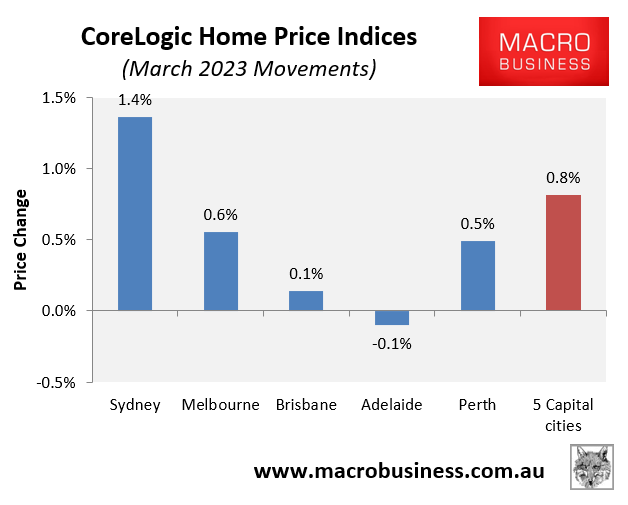

The increase in values was driven by Sydney, where prices boomed by 1.4%. Values also rose by 0.6% across Melbourne and by 0.5% across Perth:

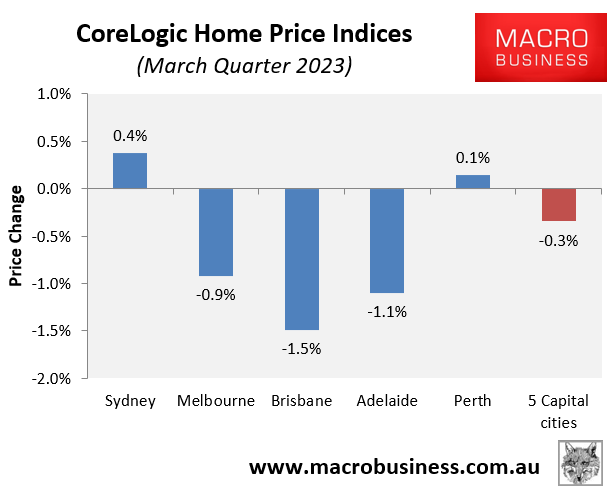

Quarterly value growth has now swung into positive across Sydney (+0.4%), while loss rates have shrunk across Melbourne (-0.9%), Brisbane (-1.5%) and the combined five capital cities (-0.3%):

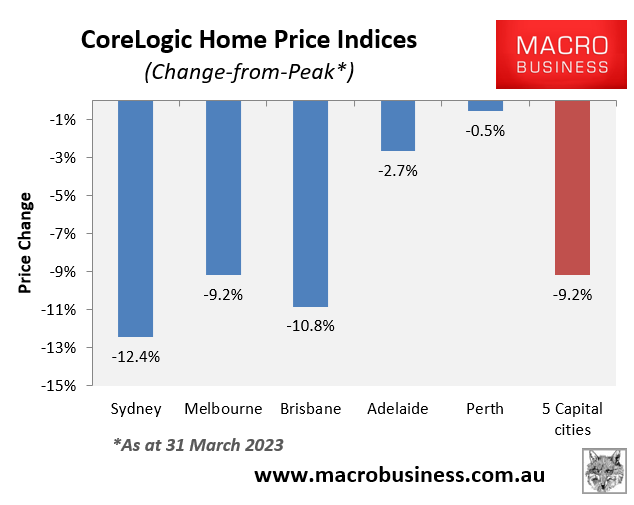

Values are now down 9.2% at the 5-city aggregate level, driven by the three major capital city markets:

It is a spectacular price rebound that has arrived despite two consecutive 0.25% interest rate rises from the RBA in early February and early March.

There are still headwinds on the horizon from the pending fixed rate mortgage cliff, so there could still be a double-dip correction.

Regardless, I believe 2024 is setting up for a price boom, given:

- The RBA is likely to cut interest rates, which would lift borrowing capacity.

- The Australian Prudential Regulatory Authority is likely to follow suit by reducing the 3% mortgage buffer, which would further boost borrowing capacity.

- Australia will continue to experience rapid immigration.

- The rental market will tighten further.

- Housing construction will be depressed, given high construction costs and widespread builder insolvencies.

Real demand exists in the market. Only high mortgage rates and their effect on borrowing capacity are preventing prices from rising.

When that restriction is lifted, the elements are in place for the subsequent house price boom.