What a terrible time to be a young Australian.

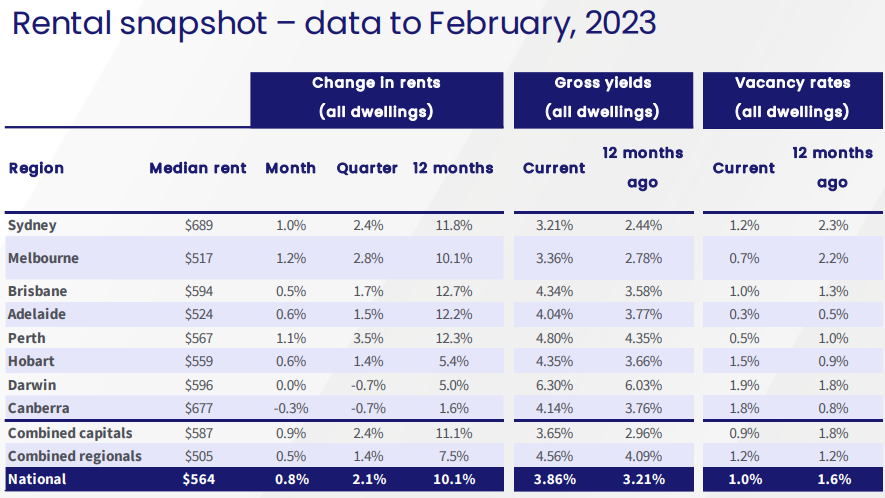

The majority of young Aussies that are renting are facing record tight conditions, with rents soaring at a double-digit pace across the combined capital cities:

Immigration is running at record levels, which means that the rental market will tighten further as well as pushing wage growth lower as the tidal wave of migrants compete with younger Aussies for jobs.

Those young Aussies that managed to ‘get in’ to the housing market are being slammed by rapid interest rate hikes, which will increase mortgage repayments by around 50% once fully passed on to borrowers.

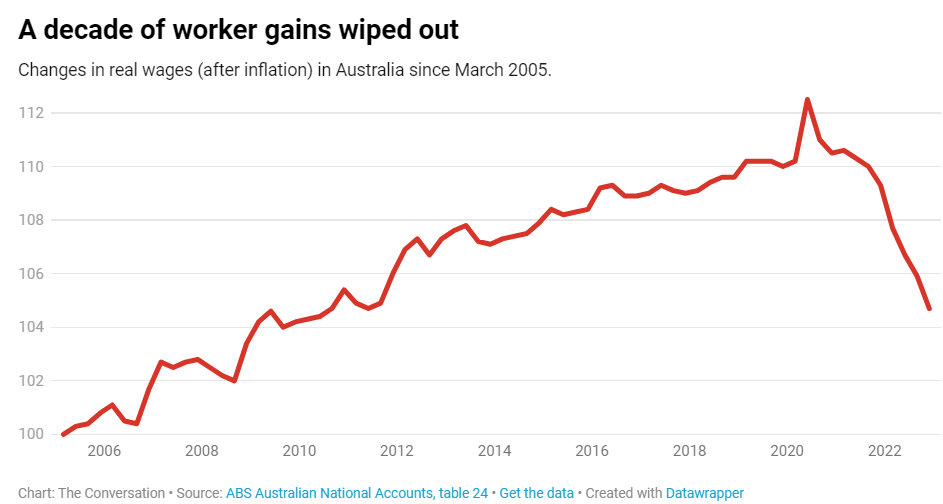

Finally, the broader cost-of-living squeeze has pushed real wages to decade lows:

Now more than three million younger Australians are facing a 7% increase in their HECS/HELP debts when the annual indexation kicks in mid-year.

According to Australian Taxation Office (ATO) data, outstanding HECS-HELP debt in 2021-22 totalled more than $74.3 billion, shared among more than three million people.

These graduates will be be hit with a $4.5 billion increase in their student debt as of 1 June.

This increase in student debt, resulting from indexation tied to the rate of inflation, will see around $1500 added to the average $25,000 student loan.

Modelling by online mortgage brokers UNO for The Daily Telegraph shows that middle and high income earners paying off $40,000 to $50,000 HECS-HELP debts lose 15% to 20% of borrowing capacity compared to those without such debts.

For example, a someone earning $99,000 a year with a student debt of $45,000 could borrow at least $457,724.

But without that student debt, their borrowing capacity increases $528,145, giving them $70,000 (15.4%) of extra borrowing capacity.

UNO Home Loans founder Vincent Turner claims the liability of HECS-HELP debt is a “triple whammy” for prospective first home buyers, impeding their ability to save a deposit and increasing their mortgage insurance and interest costs.

No matter which way you cut it, the cards are stacked against young Australians at the moment.