Westpac with the note.

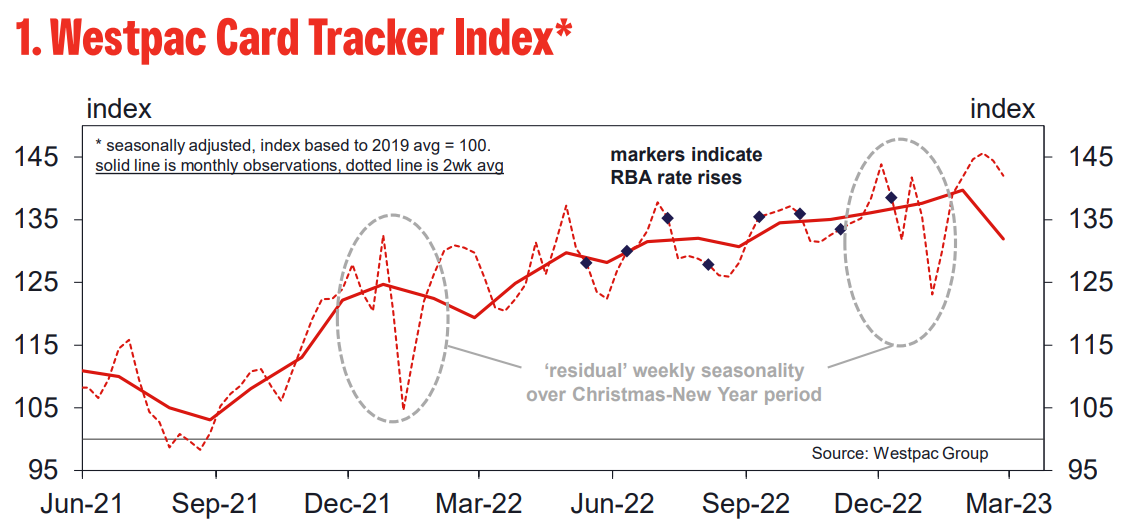

― The Westpac Card Tracker Index posted a notable pull-back over the second half of February, falling 4.8pts over the last two weeks, from 145.7 to 138.3. While this still leaves the index at a relatively high level, the growth pulse appears to be slowing significantly with quarterly momentum in nominal spending now getting close to stalling.

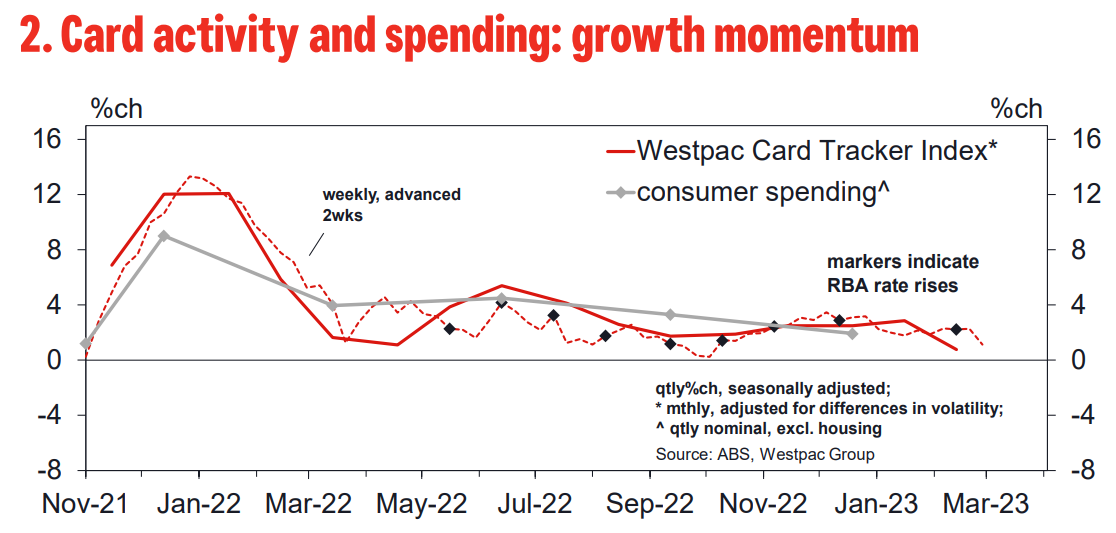

― Stalled nominal spending implies outright declines in real, inflation-adjusted terms. With the recently released Q4 national accounts showing a weaker-than-expected finish for real consumer spending in 2022 and more constrained picture of household finances, the latest card updates suggest there has been a further deterioration in momentum in early 2023. That said, technical differences may see some of the resilience in card activity in Q4 support official spend measures in Q1, particularly around services.

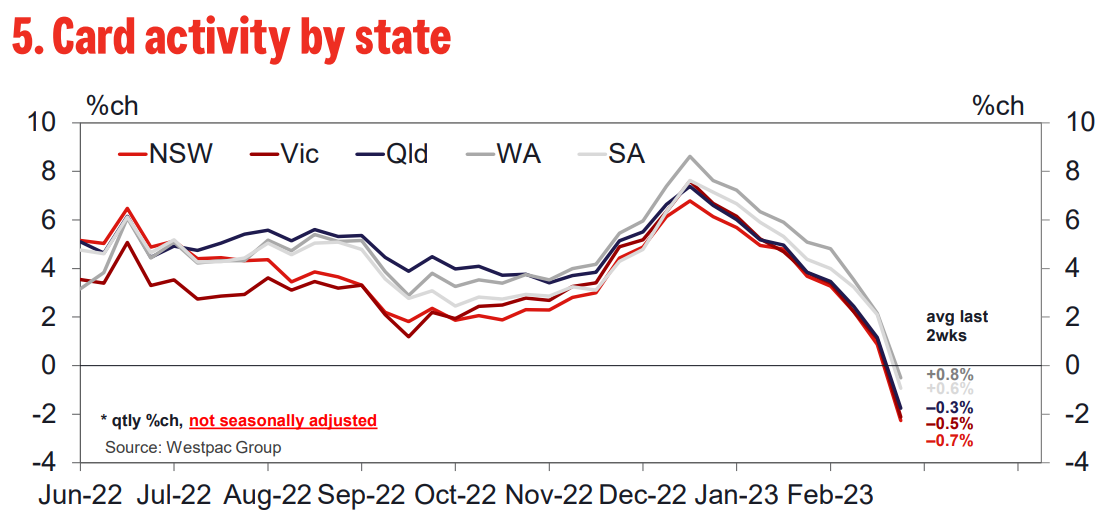

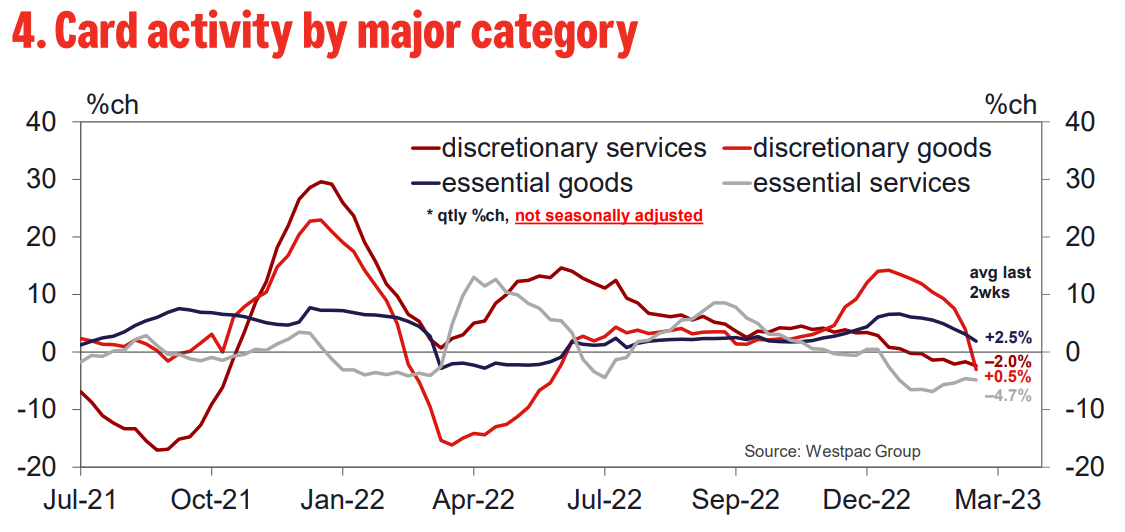

― The detail suggests a slowing in services and non food retail spending is more than offsetting a lift in food retail and hospitality. The slowing is more pronounced for discretionary categories although separating seasonal shifts from trends, and price-driven from volume-driven shifts remains difficult. Interestingly, the state breakdown shows weaker activity in NSW, Vic and Qld despite what looks to have been a more material lift in migration-driven population growth in NSW and Vic over the course of 2022.

― While still tentative, the softer tone starting to come out of the card data suggests the anaemic growth in real spending seen late last year may be shifting to outright weakness in early 2023. If so, the March updates on card activity could prove decisive for wider economic prospects this year.