Citi with the note. Still looks like a bit of a sudden freeze to go along with the banking crisis.

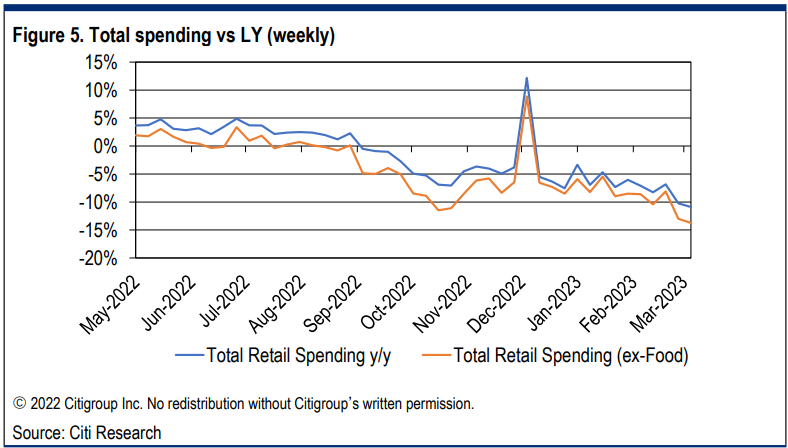

Citi’s CC data for the 16 sub-sectors we track show that total spending in March wk 4 (ended 3/25/23) decreased 10.9%, a slight deceleration vs March wk 3 (-10.3%). To be clear, the data we report on are for 16 subsectors of spending relevant to our retail coverage universe. We do not track (in our data) spending on services (where spending trends have been significantly stronger in F23 than our 16 sub-sectors). March to date is down 8.9% and is on pace to be the weakest month since April 2022. Ex-Food spending decreased 13.7% vs -13.0% in March wk 3 and March to date (exfood) is down 11.3% vs Feb down 7.6%. These past two weeks of deceleration reflect spending pressure potentially stemming from (in no particular order) disruption within the financial sector, unfavorable weather, SNAP benefit reduction and/or lower tax rebates. March week 4 also decelerated compared to 2019.

Citi’s Proprietary CC Data for 16 sub-sectors: Citi is the world’s largest credit card issuer, and our Retail Research Team in conjunction w/Citi’s Research Innovation Lab colleagues, look at high level credit card data at a sub-sector level, which we believe is helpful in assessing overall spending trends to help build an investment mosaic.