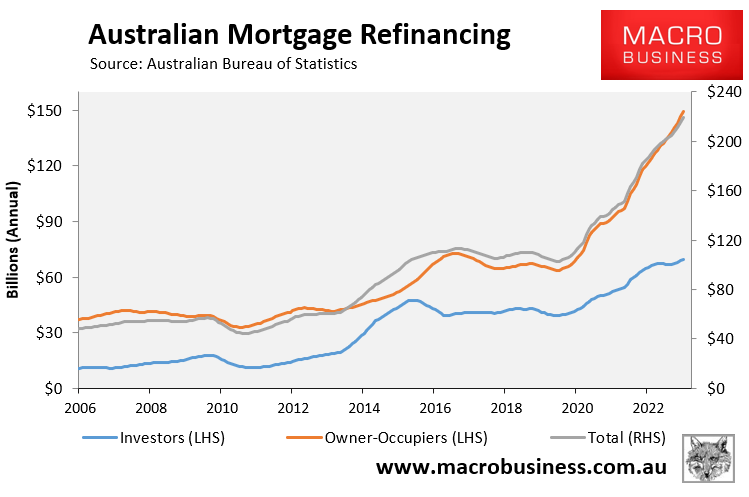

This week’s housing finance statistics from the Australian Bureau of Statistics (ABS) showed that refinancing activity has hit new highs, with $219 billion worth of mortgages refinanced in the year to February 2023:

That’s double the value of mortgages refinanced in the year to February 2020, just prior to start of the pandemic.

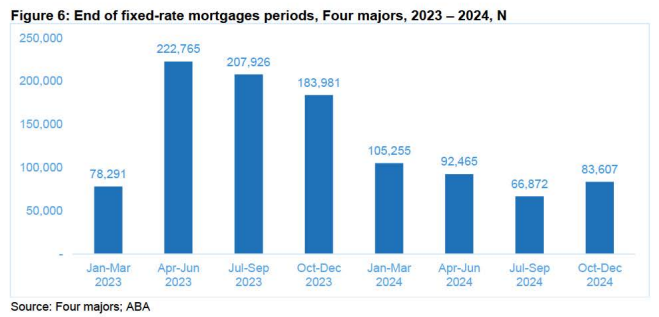

Refinancing activity is certain to increase through the remainder of this year given record volumes of fixed rate mortgages are scheduled expire over the June, September and December quarters.

As shown in the following chart from the Australian Bankers Association, around three times as many mortgages (222,800) will expire over the June quarter as did over the March quarter (78,300).

There will also be large volumes of fixed rate mortgage expirations in the quarters ending in September (208,000) and December (184,000):

These expirations will see borrowers convert from ultra cheap fixed rates of around 2% to variable rates of around 6%, thereby adding thousands of dollars a year in repayments on the typical mortgage.

Sydney homeowner Steven De Celis is a case in point. This week the 44 year old told The AFR that his $1.6 million fixed rate mortgage will expire in June, lifting his repayments from $69,000 a year to nearly $110,000.

“I’m going to get absolutely slammed”, De Celis said.

“I’m really nervous, to be honest. The pause this month is a relief. It will stop the haemorrhaging, for a bit, but who knows what happens next time”.

“We wait with bated breath for every RBA announcement. I just want my kids to have a good life”.

A recent survey from Canstar revealed that around one quarter of Australian mortgage holders are paying 6.5% or more on their variable rate loans, which is significantly higher than the lowest rate available on the market.

Westpac CEO Peter King also told The AFR Banking Summit that he was witnessing “the most competitive market I’ve seen in mortgages in my career”, meaning there are major savings to be had if borrowers shop around.

This is where the MacroBusiness Compare n Save home loan comparison service can help by enabling you to compare hundreds of loans to potentially save thousands of dollars in annual mortgage repayments.

Try the Compare n Save comparison service for yourself. It is quick and easy to use.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan

If you decide to proceed with an application, the Compare n Save staff will guide you through the process.

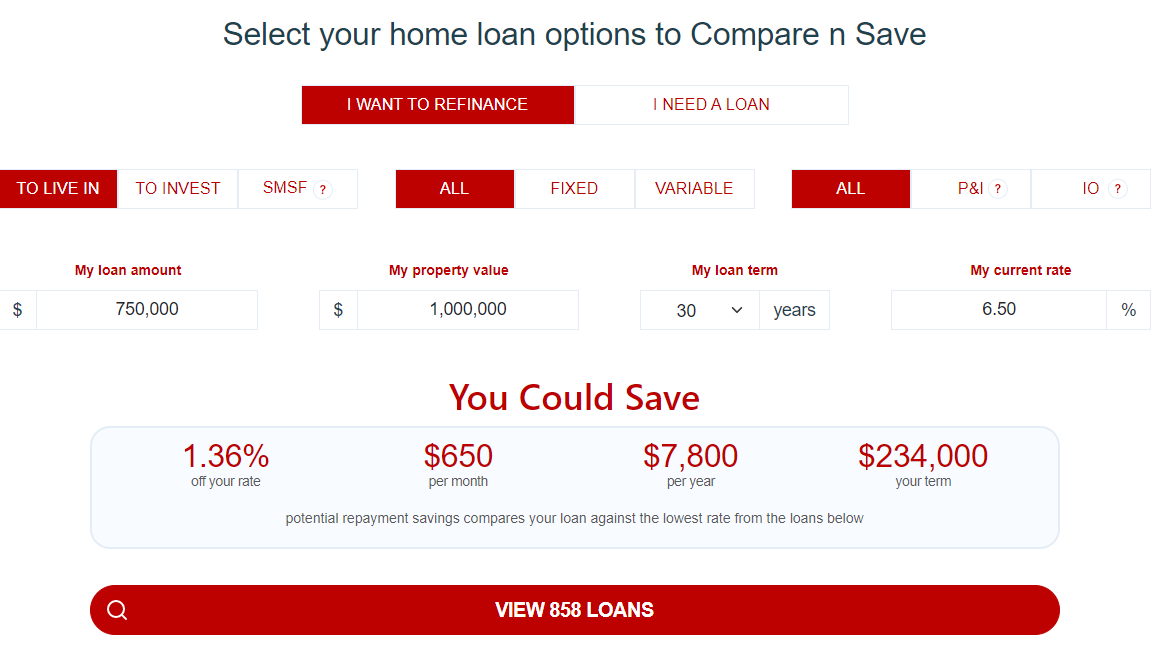

For instance, if you are seeking a cheaper rate on an existing mortgage, select “I Want To Refinance” and input the amount you wish to borrow and the interest rate you are currently paying.

Compare n Save will then show the amount you could save by refinancing.

Once you’ve browsed the various loan options, click the Enquire button, provide your contact information, and Compare n Save will get in touch with you to begin the application process.

Take as an example a person who wishes to refinance a $750,000 loan on a $1,000,000 house with a 6.5% interest rate.

If this borrower refinanced at the lowest rate available, they could save $650 per month ($7,800 annually):

The Compare n Save comparison tool lists hundreds of loans for comparison, ranging in cost from lowest to highest.

If you obtain a loan through Compare n Save, MacroBusiness will receive a share of the commission, which will help fund the site.

The approaching months will be challenging for hundreds of thousands of borrowers who are exiting low-cost fixed-rate mortgages.

At least you can reduce the damage by making sure to pay the lowest possible mortgage rate.

Make the banks fight for your dollar.