By Bill Evans, chief economist at Westpac:

Key Points:

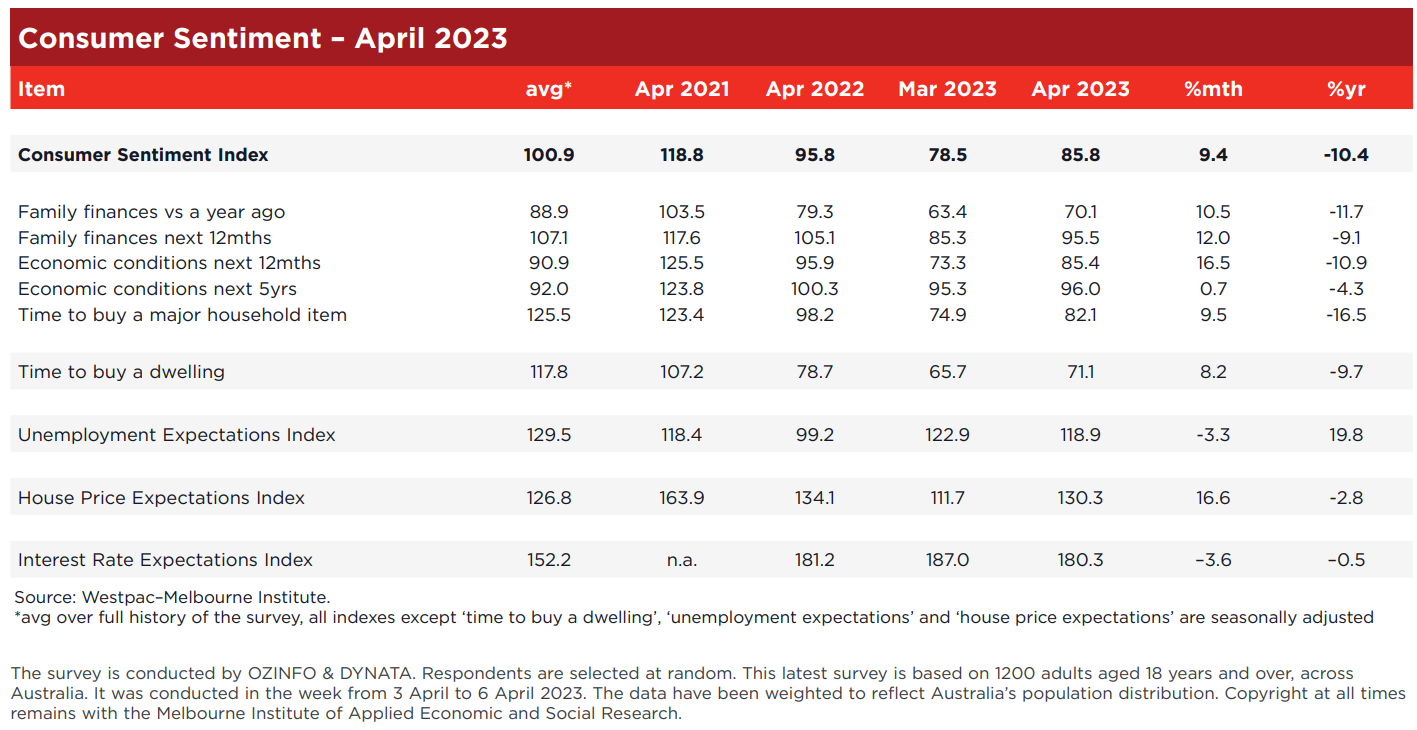

- Westpac-Melbourne Institute Consumer Sentiment surges by 9.4% in April.

- The decision by RBA Board to pause is the key to this resurgence.

- Confidence still weak – 10.4% below April last year before the tightening cycle.

- Confidence amongst mortgage borrowers lifted by 12.2%.

- Respondents remain cautious – 34.11% still expect rates to increase by more than 1% over the year although down from 44.55%.

- Confidence in the outlook for house prices has surged – Index up by 16.7%.

- The House Price Expectations Index is up 43% from its recent low in November.

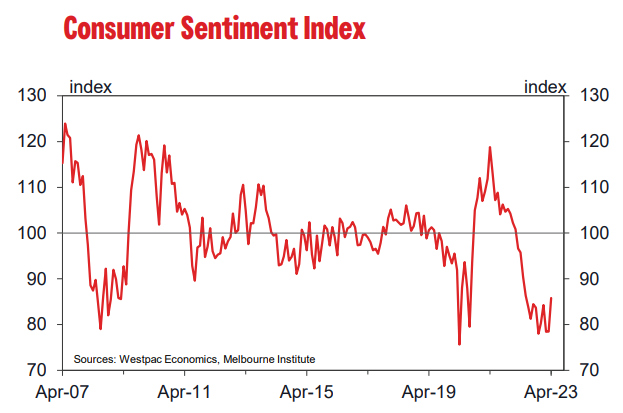

The Westpac Melbourne Institute Consumer Sentiment Index increased by 9.4% in April from 78.4 in March to 85.8 in April:

This strong recovery in the Index can be largely attributed to the decision by the Board of the Reserve Bank to break the sequence of ten consecutive meetings when the cash rate was increased by deciding to pause at the April meeting.

The survey was conducted over the four days of April 3–6 which covered the Board meeting on April 4.

While this tightening cycle has been unique in terms of ten consecutive meetings of rate increases the most comparable period was October 2009 to May 2010 when the Board increased rates at every meeting apart from the February meeting. Initially the pause in June was treated sceptically by consumers with Confidence falling a further 5.6%.

Following a second pause in July consumers became convinced that the pause could be sustained and Confidence increased by a solid 11% – not dissimilar from the result for April 2023.

Confidence is now at its highest level since June 2022 although still 10.4% below April 2022, the month before the RBA Board began raising the cash rate.

Despite this lift in April, we still characterise Consumer Sentiment as weak and consistent with Westpac’s view that consumer spending through 2023 and at least the first half of 2024 will be lack-lustre.

Following the Board’s decision, 34.11% are still expecting the Standard Variable Rate to be raised by more than 1% over the next year. That proportion is certainly down from 44.55% in March and 59.64% in November but still points to considerable apprehension around interest rates on the part of consumers.

Confidence amongst respondents with a mortgage lifted sharply by 12.2% although it is still 14.5% below its level before the tightening cycle began.

There were some very strong messages from the sub – Indexes, particularly around family finances and spending intentions.

The Sub Index – “Family finances compared to a year ago” lifted by 10.5% while the Sub Index – “Family Finances over the Next 12 months “surged by 12.0%.

The Sub Index – “Economic Outlook over the Next 12 months” lifted by 16.5% while “Five Year Outlook” was flat.

Time to Buy a Major Household Item” was up by 9.5%. This subIndex is still troubling. Last month we reported that the Index was at its lowest level in the history of the survey back to 1974 (apart from one month during the Global Financial Crisis). It is still very weak being 16.4% below April last year and 1.2% below the weakest print during the deep recession of the early 1990’s.

One key reason why spending has held up better than would normally be expected given such weak confidence has been the resilience of the labour market. In April, the Westpac Melbourne Institute Index of Unemployment Expectations fell by 3.3% from 122.9 to 118.9.

Because the Index measures respondents’ assessments of the outlook for the unemployment rate a lower print indicates an improvement in the outlook. Over the last six months the Index has increased by 6.8% indicating a gradual deterioration in consumers’ assessments of the labour market despite the modest improvement in April.

The improved outlook for interest rates has provided a significant boost to confidence in the housing market.

The Index “Time to Buy a Dwelling” increased by 8.2% from 65.7 to 71.1. This measure of confidence in housing, which, we believe, is heavily influenced by affordability remains very weak. The April result only restores the Index to the 70–80 range where it has held since the tightening cycle began. And recall that this Index is still 46% below its peak back in November 2020.

Confidence in the outlook for House Prices has boomed. The national Index of House Price Expectations lifted by 16.7% to 130.31, only 2.8% below its level in April last year, just before the tightening cycle began.

The Index has increased by a remarkable 43% since its recent low in November last year.

Confidence in the outlook for prices in April has lifted much more sharply in NSW (up 16%) than Victoria (up 9.5%) although some of the other states – QLD (up 30%) and WA (up 36%) are even more upbeat.

The Reserve Bank Board meets next month on May 2. The Board will have the advantage at the May meeting of a clean read on underlying inflation from the March quarter Inflation Report, which prints on April 26, and the staff’s refreshed economic forecasts.

With underlying inflation still likely to be in the 6.5%–7.0% range and the unemployment rate holding around fifty-year lows the case for extending the pause in May is likely to be challenged.

Risks at this stage to the inflation outlook from a potential wealth effect through the housing recovery, which is being signalled in this survey; the boost to demand from the unexpected sharp lift in immigration and Australia’s current dismal productivity record put more uncertainty around the Board’s current two-year plan to return inflation to the 2–3% target band.

The Board’s decision will be to weigh the “here and now “evidence against its two- year forecast.

Westpac expects that a final 0.25% increase in the cash rate at the May Board meeting remains the best policy approach rather than awaiting even more information and risking even higher rates later in the cycle.