Former RBA governor Ian Macfarlane this week warned that the fixed rate ‘mortgage cliff’ poses a serious concern for Australian households and the financial system, and may require intervention from regulator APRA and the federal government.

“It will be resolved by the bank’s customer – the borrower – taking a haircut, probably APRA bending a few rules, and conceivably, a last resort, the government having to step in”.

If things “really got nasty, there would have to be some form of additional lending from government”, Macfarlane said in a podcast with private wealth firm, Stanford Brown, of which he’s an investment committee member.

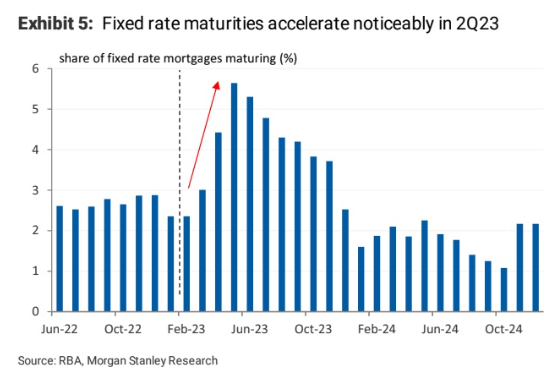

The next chart shows that record numbers of fixed rate mortgages expired in May, with additional large volumes scheduled to expire over the remainder of 2023:

Many borrowers will reset from ultra-cheap rates of around 2% to variable rates nearing 6% or above.

In turn, monthly loan repayments will rise by around 50% for these borrowers.

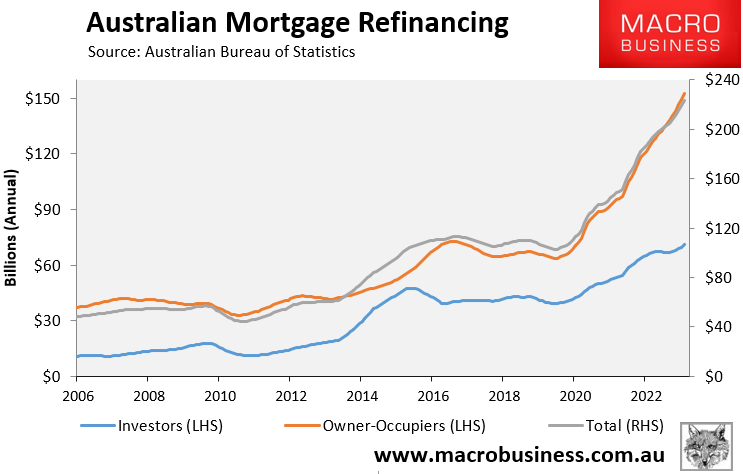

Soaring interest rates, alongside the fixed rate mortgage reset, has driven a boom in refinancing activity.

Data released on Friday by the Australian Bureau of Statistics showed that $226 billion worth of mortgages were refinanced in the year to April, which is around double the pre-pandemic level:

Owner-occupiers have driven this refinancing activity, with loan volumes more than double since the start of the pandemic.

Meanwhile, the RBA assistant governor (financial system), Brad Jones, told a Senate Estimates Committee this week that 15% of variable-rate borrowers will face negative cash flow by the end of this year as their loan repayments climb above their disposable income.

Thus, many borrowers will face increasing difficulty in the coming months as they depart ultra-low fixed rate mortgages and reset to rates at least double these levels.

However, by refinancing to one of the market’s lowest variable rates, consumers can save themselves thousands of dollars in mortgage payments each year.

MacroBusiness has partnered with Compare n Save to offer a home loan comparison service.

This site compares hundreds of loans, and should you refinance, could save you thousands of dollars in mortgage payments.

If you choose to move ahead with an application, the Compare n Save staff will handle the process for you.

Try the Compare n Save comparison service for yourself. It takes less than a minute.

For example, if you want to refinance your mortgage, simply click the “I Want To Refinance” button, input the amount you want to borrow, and the interest rate you are presently paying.

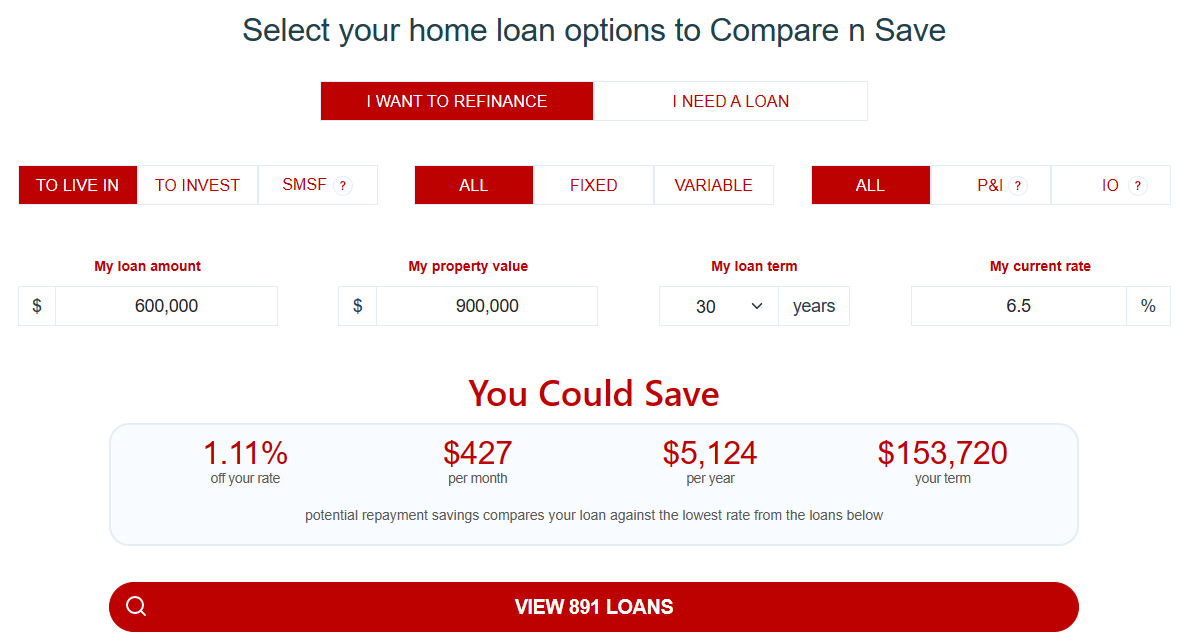

The Compare n Save tool will then show you how much you may save by refinancing, as well as loan choices.

Examine the available loans, and if you wish to apply, simply click the Enquire button, enter your contact information, and the Compare n Save team will call you back to get the process started. It’s as simple as that.

Consider a borrower who wants to refinance a $600,000 loan on a $900,000 home and is being ripped off paying a variable mortgage rate of 6.5%.

They might save $427 per month ($5,124 a year) if they refinance to the lowest available rate:

The Compare n Save tool also lists hundreds of loans for comparison, starting from cheapest to more expensive.

If you go through with a loan, MB gets a cut of the commission so you will be helping the site as well.

The RBA’s record interest rate hikes are unavoidable.

But at least you can reduce the pain by making sure you pay the lowest possible mortgage rate.