A sharp disparity has emerged between mortgage growth and Australian home values.

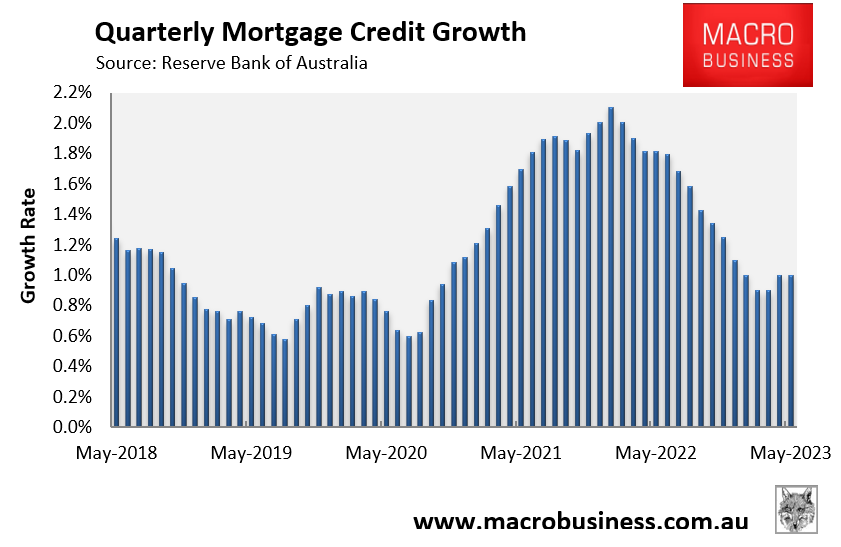

The Reserve Bank of Australia (RBA) released its mortgage credit growth figures for May on Friday, revealing that the value of outstanding mortgages increased by only 1.0% over the quarter, barely above the 0.9% lows recorded in February and March:

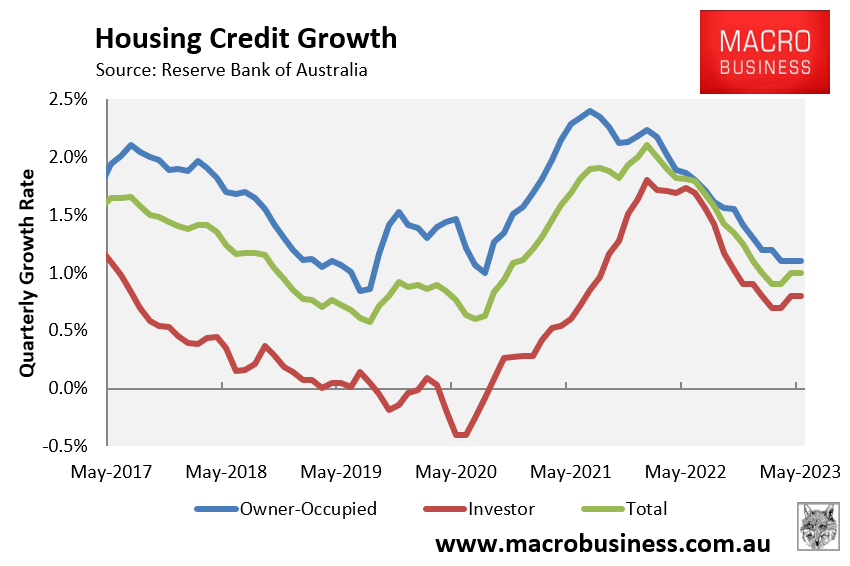

Quarterly owner-occupier mortgage credit growth is tracking at its lowest level since August 2020, whereas investor credit growth has rebounded modestly from its March low:

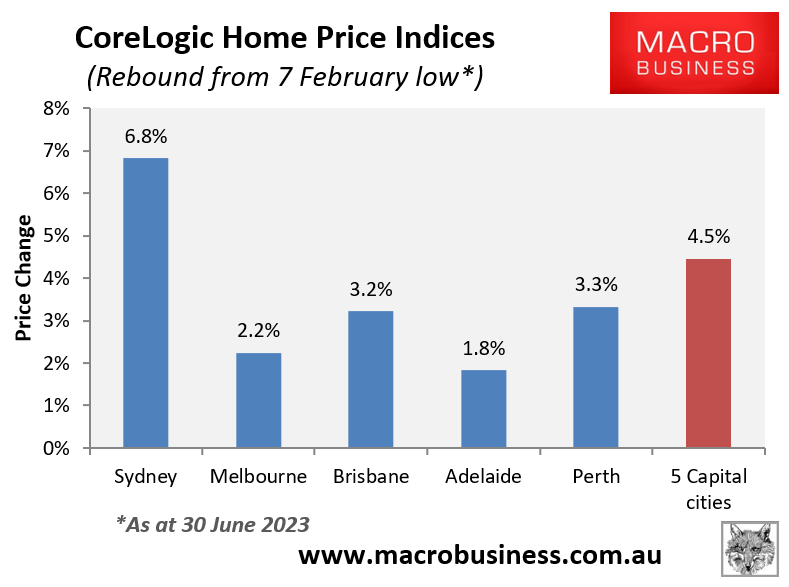

By contrast, CoreLogic’s daily dwelling values index has recorded a strong rebound since values bottomed on 7 February:

At the 5-city aggregate level, home values have recovered 4.5% from their low, led by a robust 6.8% price recovery in Sydney.

This data demonstrates that Australia’s house price recovery has occurred from a relatively narrow base.

Actual sales volumes are soft, but the homes that do sell are commanding higher prices.

The sluggish mortgage credit growth could also be attributed to Australians making extra mortgage repayments over their scheduled amount, which offsets newly issued mortgages.

It will be fascinating to see what happens to the market if the RBA hikes rates again on Tuesday.

For now, record immigration, a lack of listings, soaring rents, and rising construction costs is overpowering the rising cost of credit and falling borrowing capacity.