Total nonfarm payroll employment rose by 187,000 in July,, and the unemployment rate changed little at 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, social assistance, financial activities, and wholesale trade.

…The change in total nonfarm payroll employment for May was revised down by 25,000, from +306,000 to +281,000, and the change for June was revised down by 24,000, from +209,000 to +185,000. With these revisions, employment in May and June combined is 49,000 lower than previously reported.

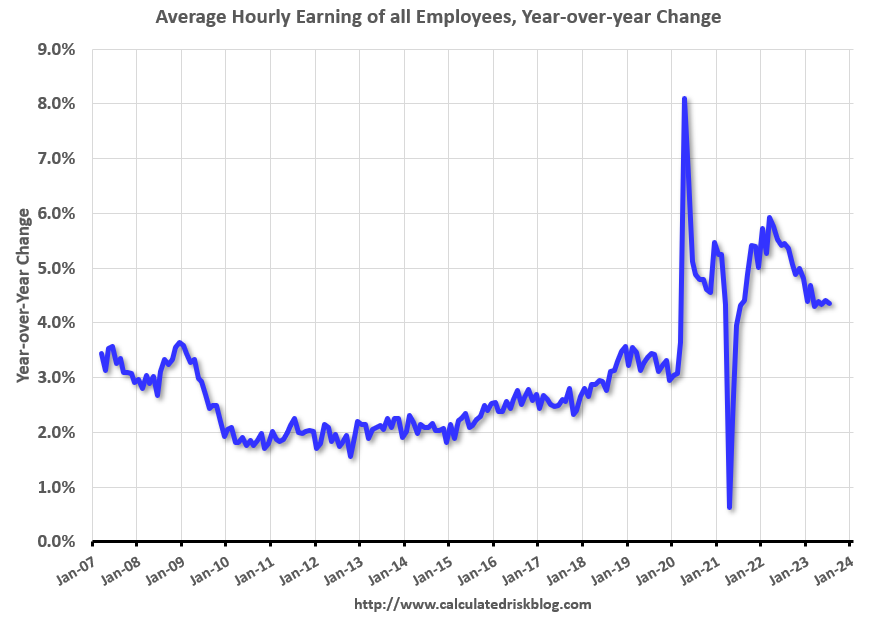

But wage growth has stabilised at around a very solid 4.5%:

Advertisement

Bidenomics favours workers. Albonomics does not. This means the US is settling into a higher interest rate price deck than China, Europe or Australia.

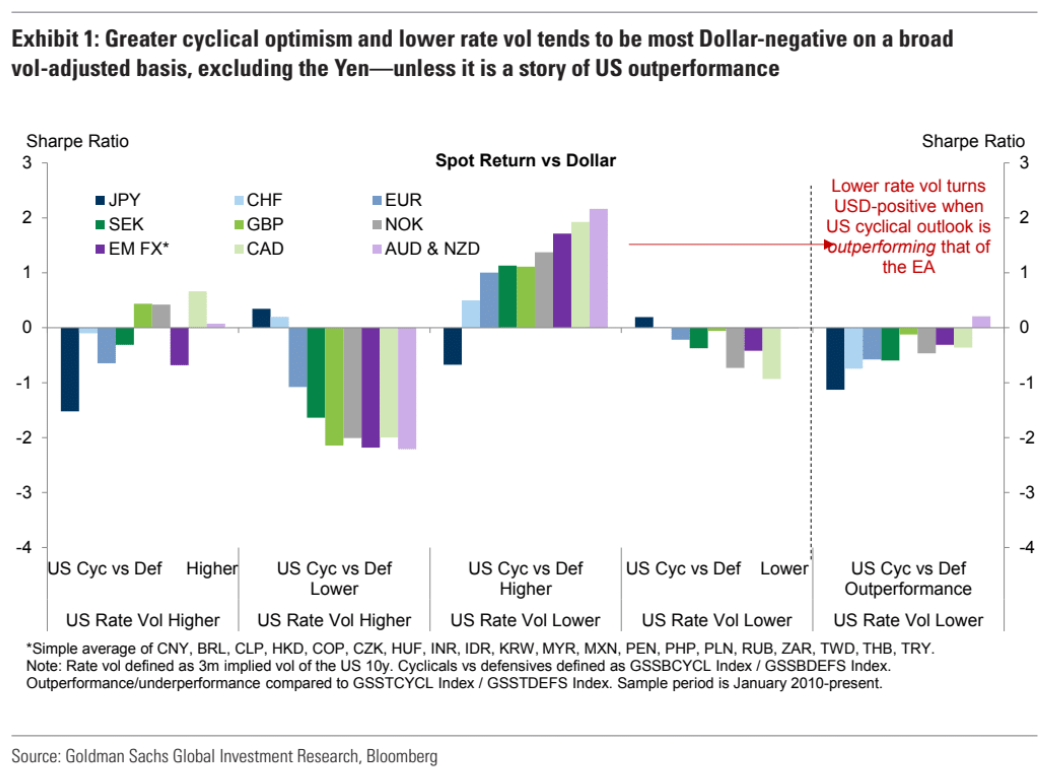

Goldman foretells the implications:

The three pillars to our ‘Shallow Dollar Depreciation’view—US growth resilience, limited foreign monetary policy support, and weak capital return prospects in the ‘challengers’—were on full display this week. In our view, the Dollar moves this week mostly reflect a ‘temperature check’ on theuncomfortable‘goldilocks’ balance between solid activity data, and still a lot official spending, but softer inflation expectations. We have argued that the risk to ‘goldilocks’ tilted towards eventually finding things running ‘too hot’ rather than ‘too cold’, which is one reason why we think yields and the Dollar will be ‘stickier’ than commonly believed, despite clear progress towards a better balance. We think this week’s price action was more consistent with the US outperformance—and the policy restrictions that may require—that has helped sustain the Dollar’s high valuation, rather than fiscal fears. That matters in part because the usual Dollar relationship with growth sentiment does not hold when the US is leading the cyclical upswing (Exhibit 1). Importantly, there were also elements of the limited foreign policy support in three key constituents. First, the BoJ’s tentative step may have added to the skittishness in fixed income markets,but so far yield differentials have moved in a JPY-negative direction, which is probably in no small part because the BoJ has acted twice already to limit JGBparticipation in the global sell-off (more in the JPY bullet below). Second, a more aggressive start to the cutting cycle in the EM ‘carry champions’ like BRLisalready eroding a bit of the carry advantage. Finally, our economistsexpectChinato ease monetary policy further, and other demand-side announcements have still shown a measure of restraint. All of that said, it is important to reiterate that we expect this uncomfortable balance to persist, and weaker inflation readings to ultimately allow the Dollar to weaken. But, this is what a shallow and bumpy path feels like, and we expect more of it to come.

Yep. Add that China is an ex-growth geopolitical pariah, the EM asset class is dead, a decade-long bear market for commodities has begun, Europe is following all down, and US AI leadership, and what you get is the ingredients for a record-low AUD in the next cycle.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.