Official data shows that the backlog of unfinished work – an industry proxy for delays – is growing significantly faster than the value of new work started.

These delays have pushed the construction industry’s total pipeline of work out to a record high $224 billion.

Meanwhile, construction insolvencies increased to 2213 in the year to June, representing the highest level in at least a decade.

This indicates that the industry is in deep trouble as a result of not being able to share unforeseen costs with clients.

“This is the industry now that government and society are relying on to fix the housing crisis, build our way to net-zero [emissions] and to house and deliver the infrastructure that’s going to house and cope with migrants coming to supplement the rest of the economy”, Australian Constructors Association head Jon Davies said to The AFR.

“We’ve got to fix the fundamental issue with sustainability of the industry or we’re going to have problems”.

Even after slowing from last year’s blistering pace, costs are now permanently higher.

According to Rick Graf, development director of residential developer Billbergia, the basic building cost per unit has increased by over 40% since the pandemic.

“We worked in order of cost per box – the cost per box is just construction [excluding land, development and finance costs] – of about $360,000-$380,000 per box”, Graf said to The AFR.

“We are now presently at $500,000 per box. We’re not pencilling in a fall below that any time soon”.

Building insurance costs have also rocketed, rising by around 40% year-on-year.

Therefore, the construction sector continues to face acute cost pressures.

As a result, construction activity is expected to continue declining.

Treasury Secretary Steven Kennedy told the Senate Estimates Economics Committee in late May that the housing downturn will last until 2025, with investment in new homes likely to fall by 2.5% in 2022-23, 3.5% in 2023-24, and 1.5% in 2024-25.

Similarly, Oxford Economics Australia predicted that overall dwelling construction activity would shrink by 21% over the three years to 2024-25.

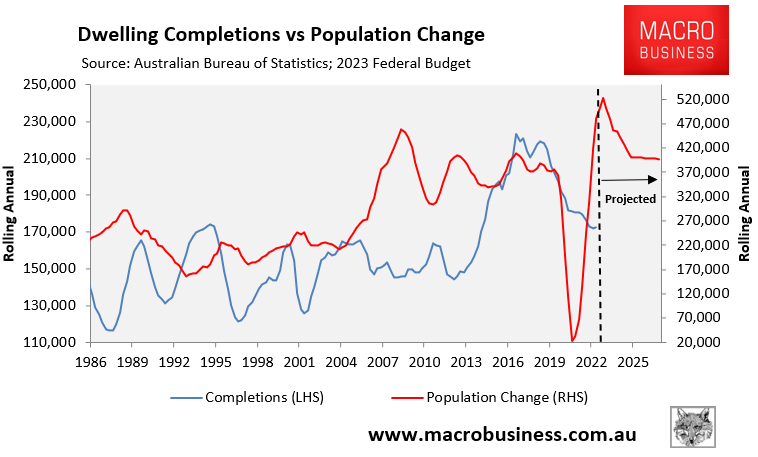

This means that the rate of new home supply will continue to shrink while Australia’s population grows at an unprecedented rate:

Just to accommodate the 1.5 million net overseas migrants projected to arrive in Australia by 2026-27, Australia needs to add 329 homes to its dwelling stock each day (net of demolitions).

Meeting this supply challenge will be clearly unachievable.

Therefore, Australia’s housing shortages will intensify, driving up rents and forcing thousands more Australians into homelessness.