‘Tis the strangest of economic cycles.

We’ve watched as the US lurched towards recession, then re-accelerated on the back of an AI stock boom.

Interest rate markets have been equally volatile, at once surging, dumping, and surging again as they chased around asset prices like a dog chasing cars.

An asset market-led economy can pivot between states quickly because it is a confidence-trick economy. Make people believe there is a recovery with wealth effects, and presto, there is one.

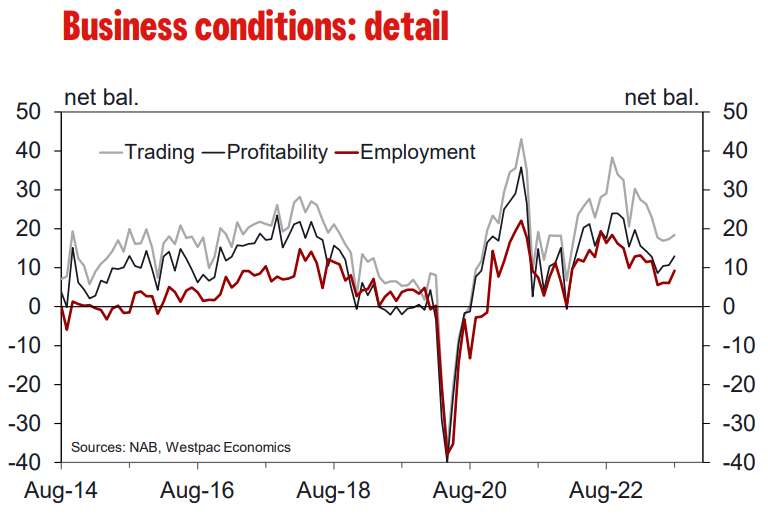

So, I looked at yesterday’s NAB survey with interest. Like the US, what seemed an uninterrupted plunge in economic conditions has suddenly stabilised and reversed:

All states are fine:

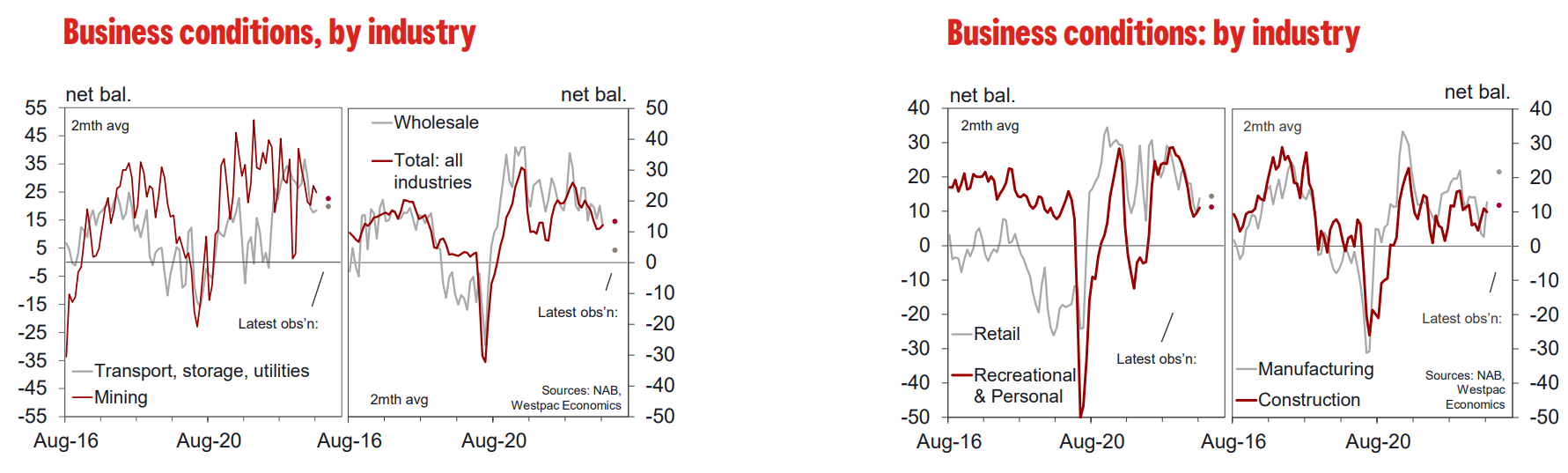

Most sectors too:

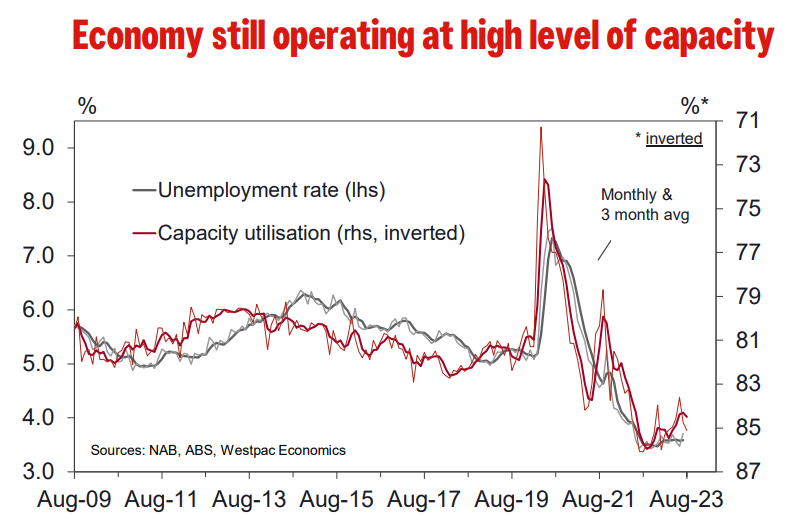

Everything is still tight:

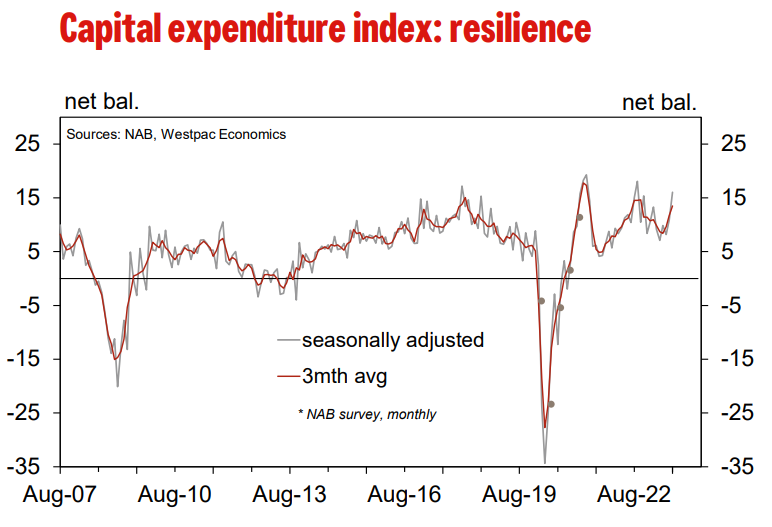

Capex is booming:

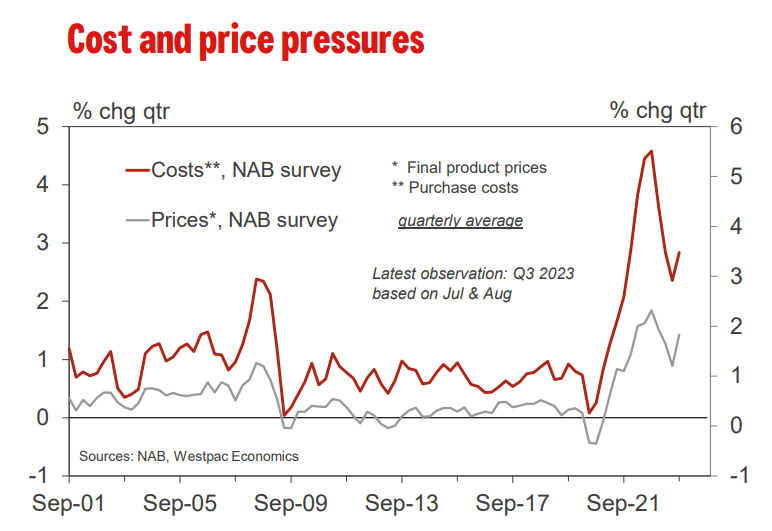

Price pressures rebounded:

I won’t make this my base case. Australia still has a lot of embedded tightening in the fixed-rate reset and mortgage rate pass-through.

As well, the NAB survey tends to exaggerate things.

That said, Australian house prices determine the economy and have been rising for a few quarters. In any normal cycle, we would expect a recovery to be taking hold about now as wealth effects spread.

The falling AUD has been boosting competitiveness, too, while the China accident has so far been more projection than reality.

And let me add an anecdote. A CEO told me last week that he had advertised last year for an IT role and gotten 150 applications from which he successfully employed.

The exact same role attracted 550 applicants this year, and nobody was suitable. Nearly all were migrants with…err…spurious qualifications.

It is not inconceivable that Albo the Wrecker has dropped an inflationary bomb on the supply side of the economy – most notably housing – without much offset in apposite labour supply.

Ergo, there is an emerging risk case that Australian interest rates have not peaked.