The current rally in iron ore shows that any market can be squeezed. Because the China iron ore supply chain is relatively restocked, it is vulnerable to speculative price moves, but do not mistake this for underlying demand.

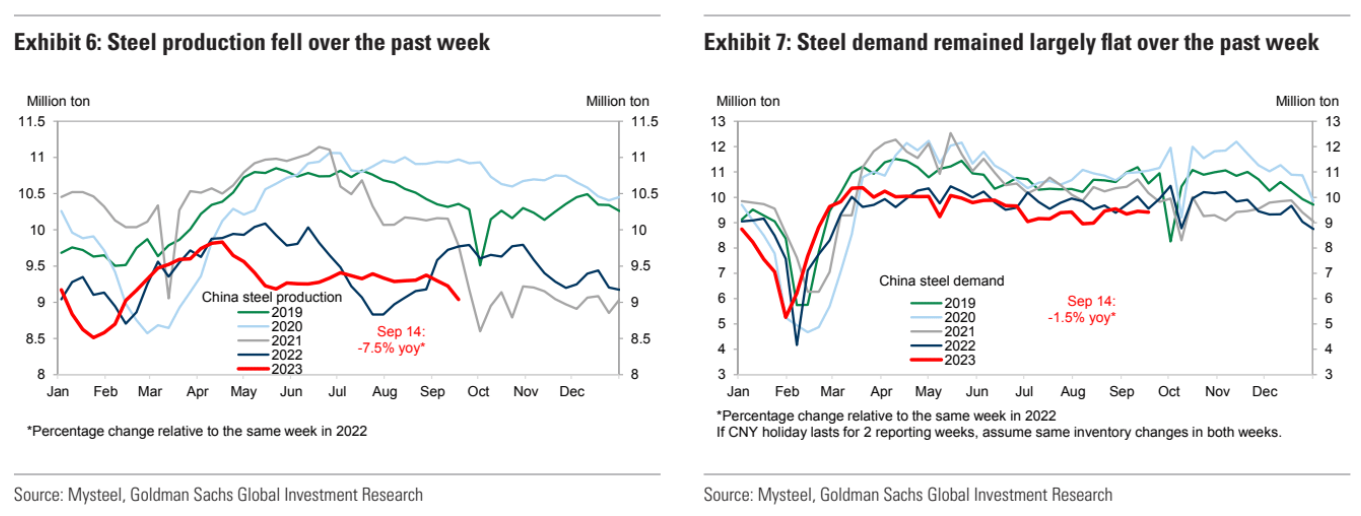

Steel production fell in August and is below 2019:

Output growth so far this year is 24mt. About 13mt of this rising exports. The rest of the growth is accelerated property completions and/or other sectors. Neither of these is sustainable.

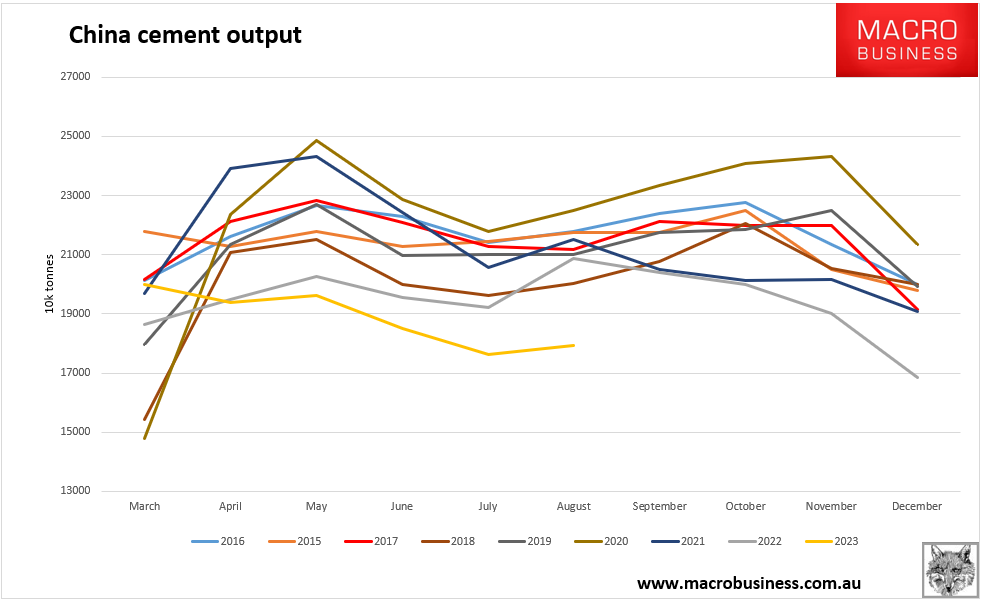

Cement cannot be exported and is the leading indicator for Chinese domestic construction steel demand:

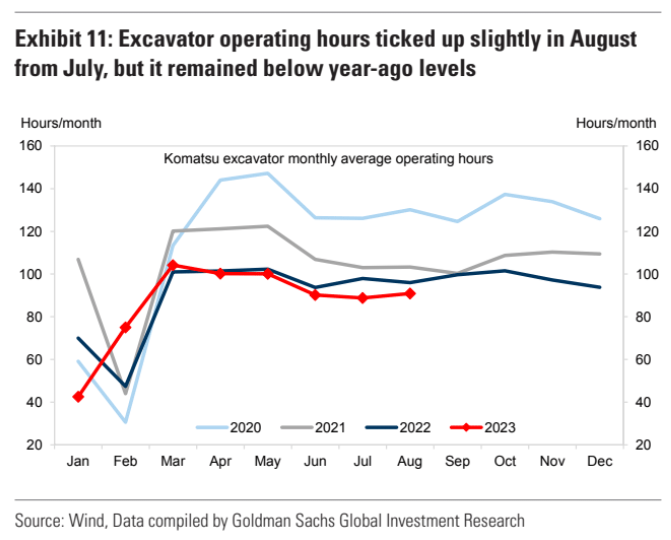

Excavators ouch:

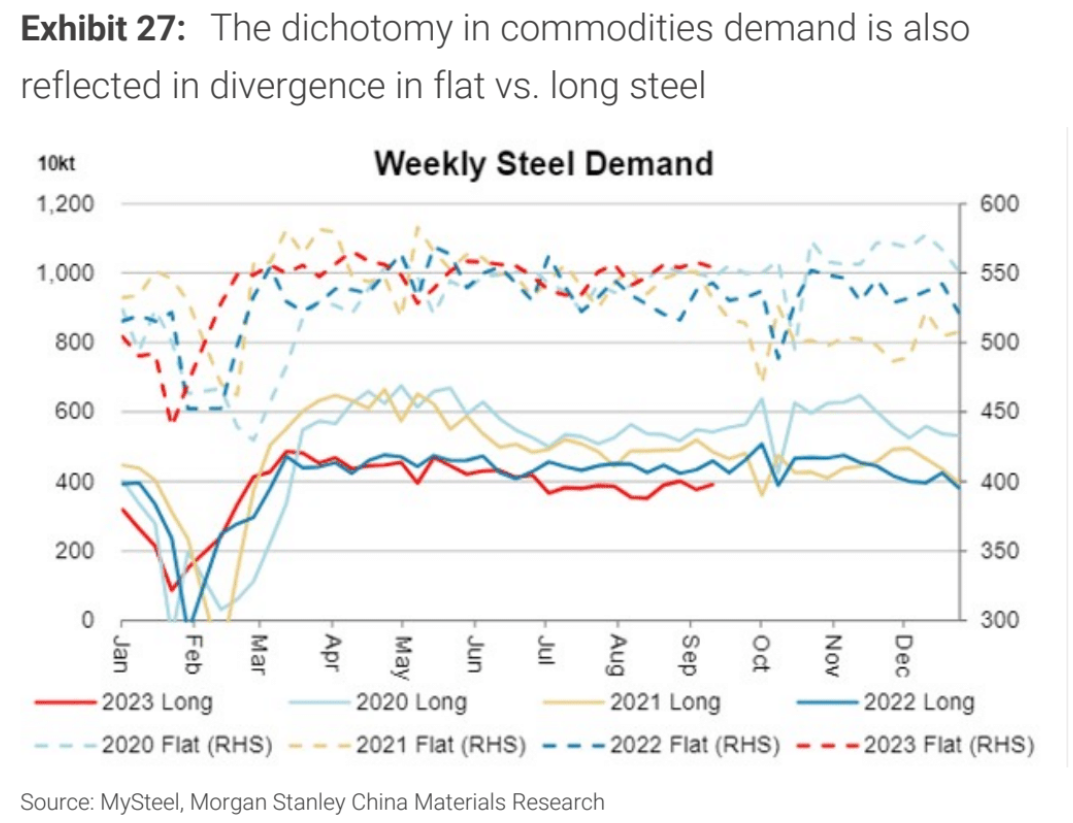

As infrastructure falls away:

Also, steel long products used in construction are only down 10% from peaks. Byt the time we are done, Chinese demand will halve:

MySteel indexes are still weak, and it sure looks like steel output caps are underway, officially or otherwise:

Scrap is again doing the heavy lifting in absorbing cuts:

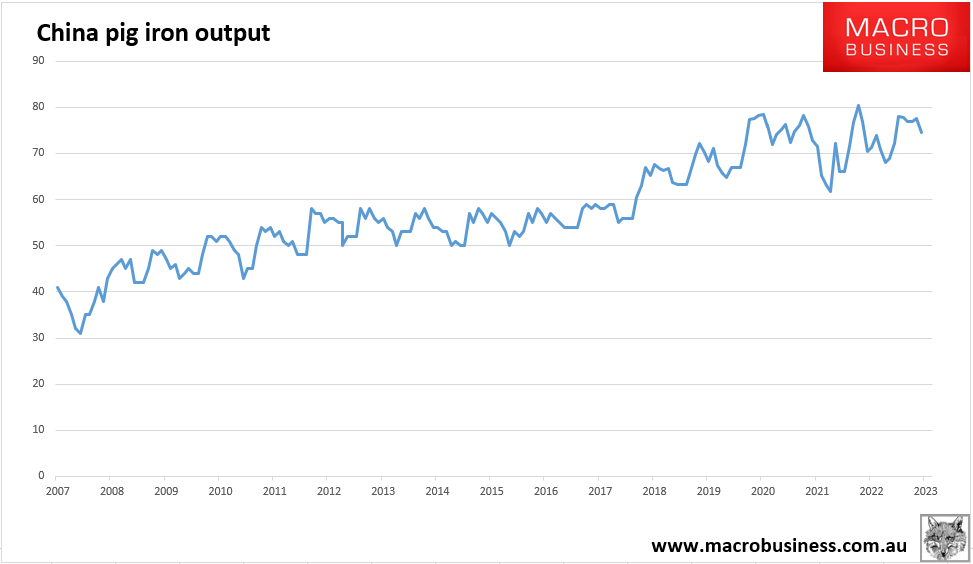

But pig iron output is falling with more ahead if output cuts persist:

The last three months of the year are shaping as materially weaker for steel output than the first nine. No stimulus has changed this.

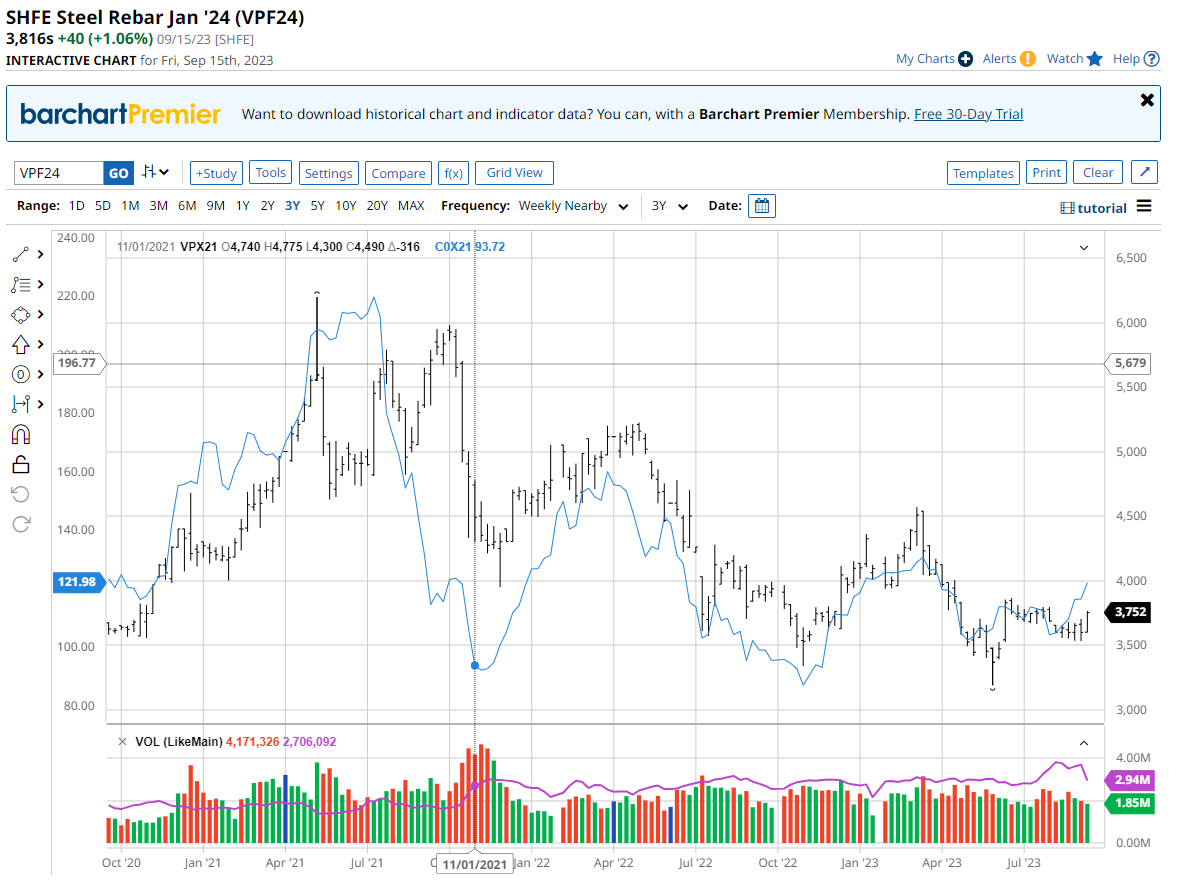

Iron ore is melting up into thin air: