The Reserve Bank of Australia (RBA) has kept the official cash rate (OCR) unchanged at 4.10% since June. Official interest rates have probably peaked, barring a significant upside surprise in Australia’s economic data.

However, because a large number of fixed-rate mortgages have yet to convert to variable rates, the RBA can rest assured that there is still a substantial level of monetary tightening ‘baked in’ to the system.

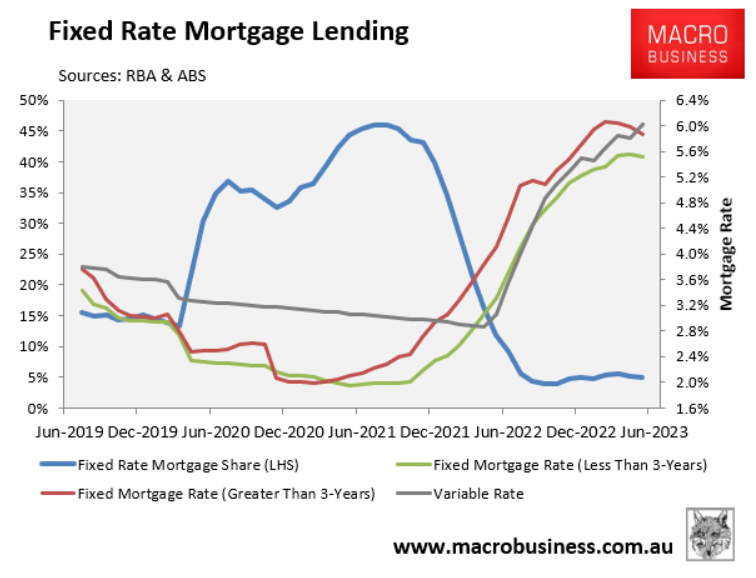

The next chart shows how a disproportionate number of mortgages had fixed interest rates at their inception during the pandemic:

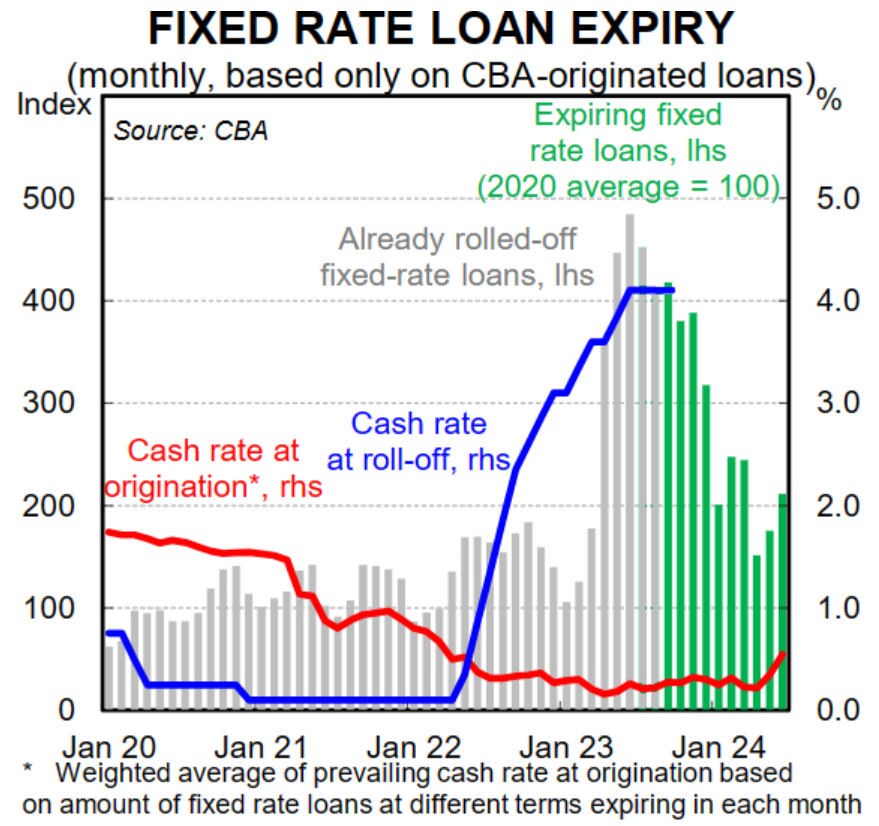

The bulk of these fixed-rate mortgages were scheduled to expire in 2023, shifting from ultra-low rates of roughly 2% to variable rates of around 6%.

According to CBA estimates, the value of fixed-rate mortgages that expired in the six months to 30 June 2023 was $34 billion, with another $52 billion expected to expire in the six months to 31 December:

According to recent CBA estimates, Australian borrowers had only felt about two-thirds of the 4% OCR increases.

However, that figure is expected to grow to roughly 85% by the end of the year as more borrowers switch their fixed-rate mortgages to variable-rate mortgages.

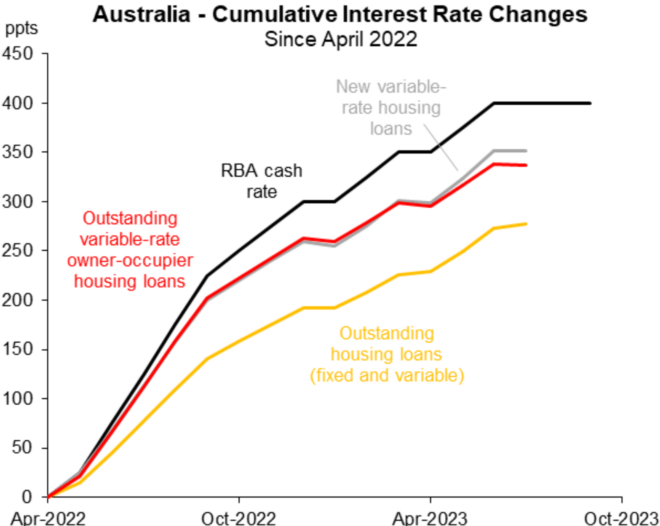

According to Justin Fabo, senior economist at Macquarie Group, the “RBA cash rate has risen 400bps, but (as at July) the weighted-average rate on outstanding variable-rate owner-occupier home loans in Australia had risen ‘just’ 337bps”.

“For all outstanding home loans, the rise was 278bps”, according to Fabo:

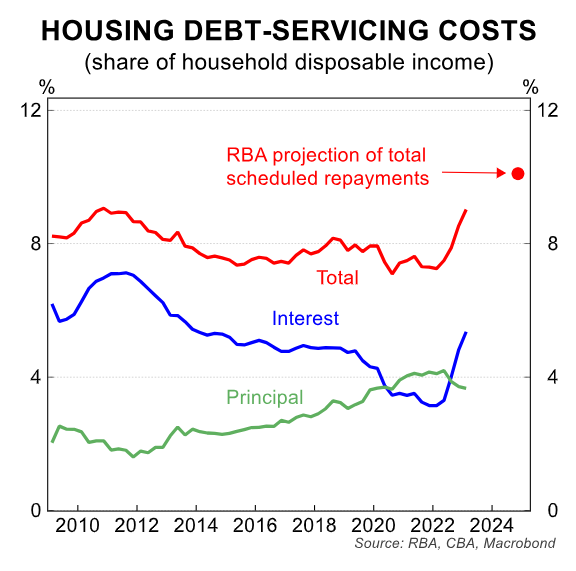

CBA projects that by mid-2024, once almost all of the pandemic fixed-rate mortgages have expired, Australian households in aggregate will spend about 10% of their disposable income on debt servicing costs, easily the highest share on record:

Accordingly, as fixed-rate mortgages expire, the average interest rate paid by Australian mortgage holders will continue to grow.

This lessens the need for the RBA to raise interest rates even further in order to slow the economy.

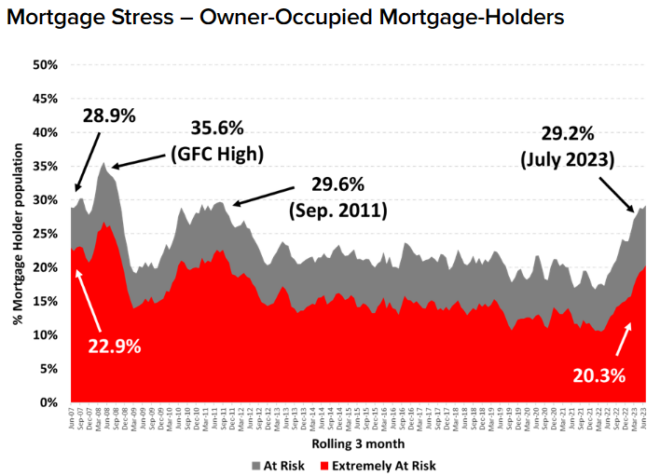

Mortgage stress will climb further:

The RBA acknowledged in its statement accompanying this month’s interest rate decision that the impact of rate increases on Australian households is uneven, with “with many households experiencing a painful squeeze on their finances, while some are benefiting from rising housing prices, substantial savings buffers and higher interest income”.

Variable mortgage rates have more than doubled since the RBA began raising interest rates in May 2022, resulting in a circa 50% increase in principal and interest mortgage repayments.

According to Roy Morgan’s most recent mortgage stress survey, 29.2% of owner-occupied households with mortgages are “stressed”, the highest level since May 2008 when the OCR was 7.25%:

Roy Morgan says it employs “a conservative model, essentially assuming that all other factors remain constant”.

As a result, as more borrowers migrate from fixed to variable rates, mortgage stress will rise.

Furthermore, if Australia’s unemployment rate climbs in line with the RBA’s prediction, from 3.7% to about 4.5% late next year, mortgage stress would worsen.

The risks of a recession are increasing:

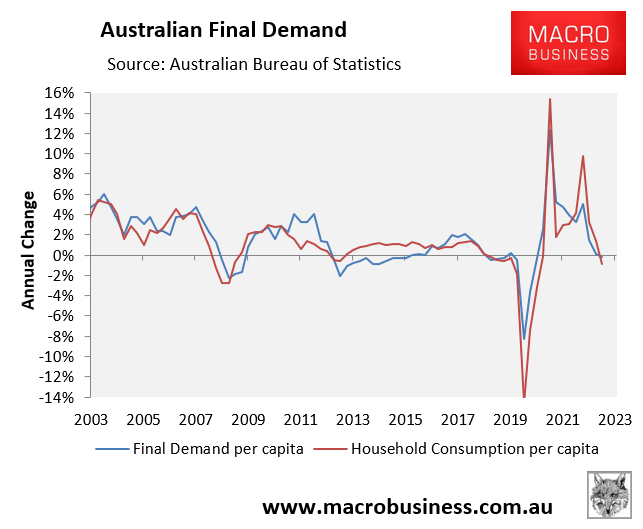

The Australian Bureau of Statistics (ABS) released its June quarter national accounts earlier this month, revealing that the Australian economy has entered a per capita recession after two consecutive 0.3% decreases in per capita GDP.

This drop in per capita GDP was caused by a contraction in household consumption, with real per capita household disposable income falling by 0.2% year on year to June:

Australian consumption spending and the economy will deteriorate further as average mortgage repayments rise when the large number of fixed-rate mortgages expire and revert to variable rates, as explained above.

Households will also experience prolonged real income declines as salaries fail to keep pace with inflation.

Given these circumstances, the RBA was justified in keeping interest rates on hold at its latest meetings.

The fixed-rate mortgage reset has already resulted in significant monetary tightening. This will cause further mortgage stress for households while also dampening consumer expenditure and the economy.