Rabobank has released a report, entitled “Shock After Shock After Shock”, which notes that Australia’s retail sector has been in recession for a full year once inflation and population growth has been taken into account.

Worse, the retail recession will continue into 2024 as the Reserve Bank of Australia (RBA) hikes interest rates further and more borrowers roll-off cheap pandemic fixed rate mortgages:

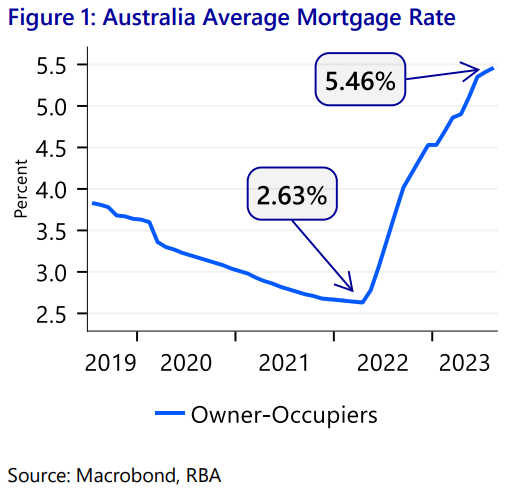

“Since May 2022, the RBA his lifted the cash rate by 400 basis points. Figure 1 shows that as of August this year, only 283 bps worth of that tightening has been transmitted to average mortgage rates for owner occupier mortgagors”.

“Further transmission of past tightening will occur as fixed-rate loans expire and competition for refinancing between lenders dies down”…

“Australian Q3 trimmed-mean inflation of 1.2% QoQ was much higher than the market expectation of just 1%. Q2 inflation was also revised higher. This gives Rabobank increased conviction on our forecast of a 25bps rate hike from the RBA in November to take the cash rate to 4.35%”.

“Risks of further increases to the cash rate are now tilted to the upside, and a hike at the December meeting is a possibility”…

“The impact of monetary tightening is now being widely felt in the real economy. The average variable-rate owner occupier mortgagor has seen their repayments increase by between 30-50% since May of 2022″…

“Softening in the labour market suggest that simply increasing hours worked is becoming less viable as a response to higher prices and interest costs”…

“Alongside softening in the labour market, a substantial slowdown in consumer spending is underway”.

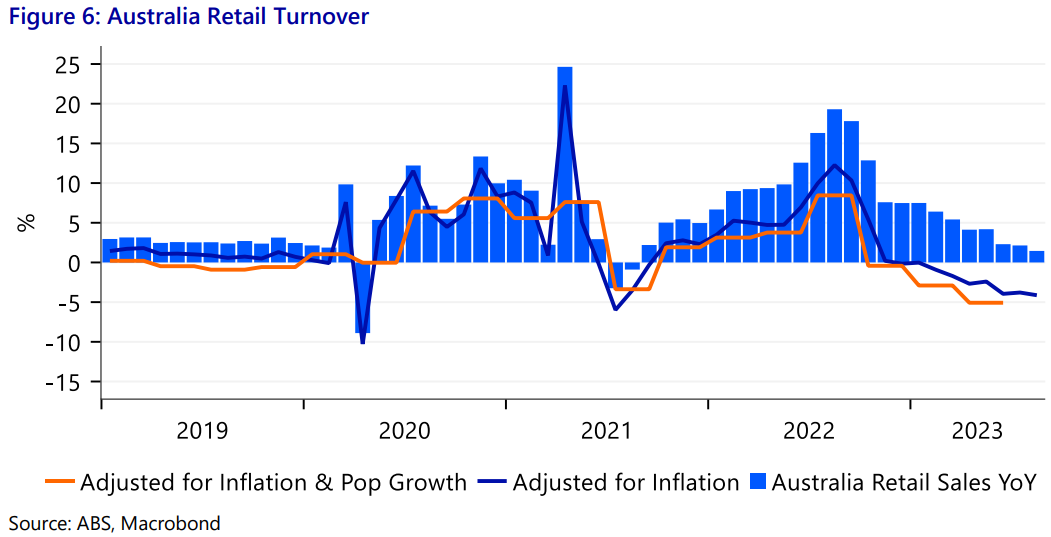

“Annual growth in retail turnover has fallen steadily since the highs of mid-2022, when stimulus induced “revenge spending” from the Covid lockdowns was in full-swing”.

“Annual growth in retail turnover is now below pre-Covid levels (Figure 6). If we adjust for growth in prices we can see that the *real* volume of turnover in goods and services has been falling since the start of this year”.

“Adjusting further for the strong growth in population reveals that real turnover of goods and services per capita has been falling since October of 2022”.

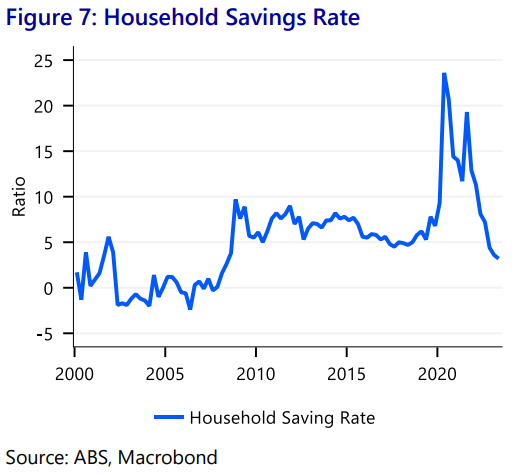

“In a further sign of pressure, the household savings rate has declined to 3.2%. That is the lowest level since 2008”.

“The rate is expected to fall further when the Q3 national accounts are released in early December”.

“The October Financial Stability Review also showed that [if] expenses like insurance and private school fees are included in household expenditure, the proportion of variable-rate mortgagors experiencing negative cashflow is ~13%”.

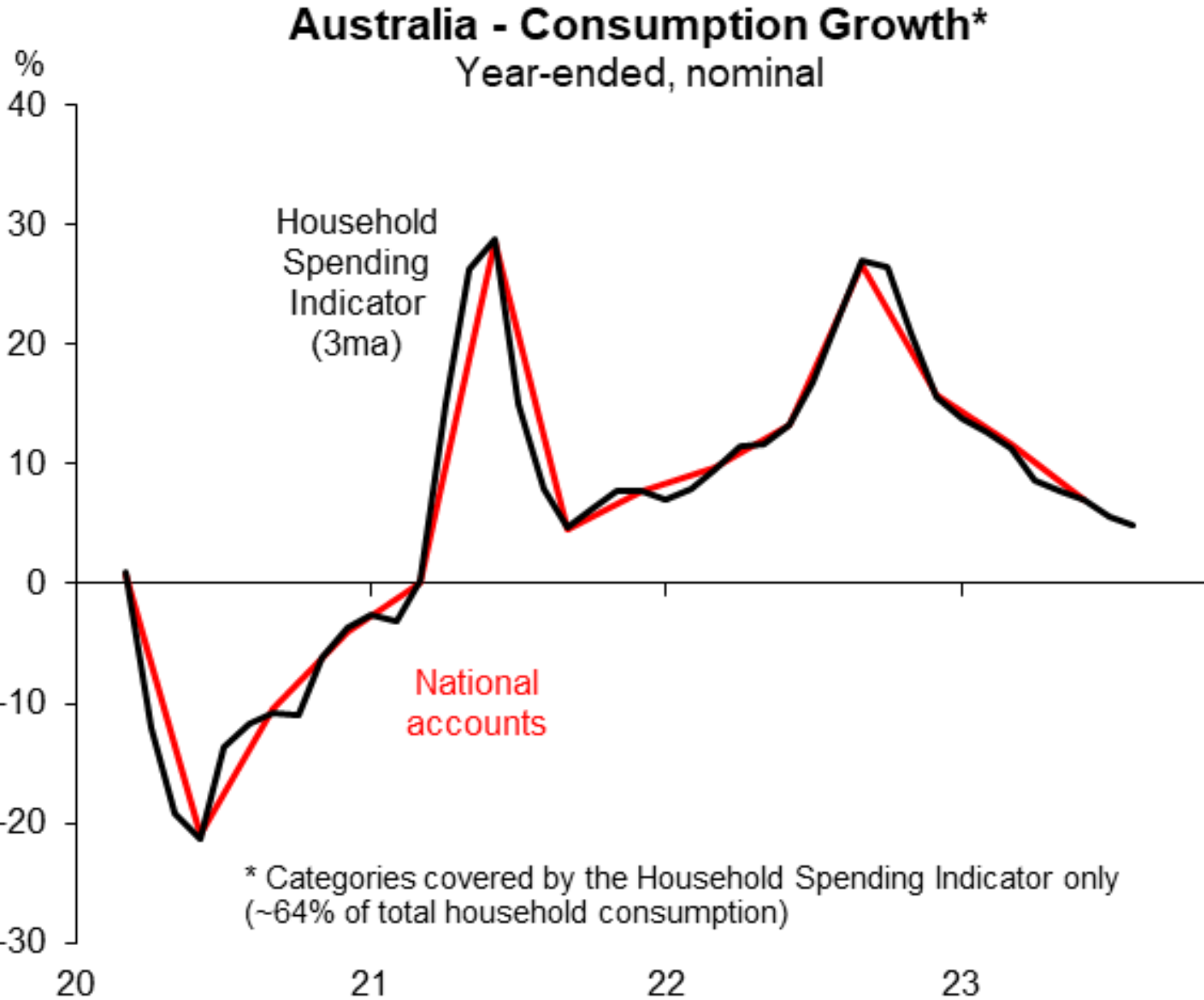

Earlier this month, Justin Fabo from Macquarie Group posted the below charts on Twitter (X) showing the sharp deceleration in nominal household consumption, as measured by the quarterly ABS national accounts and the more timely ABS Household Spending Indicator:

Source: Justin Fabo (Macquarie Group)

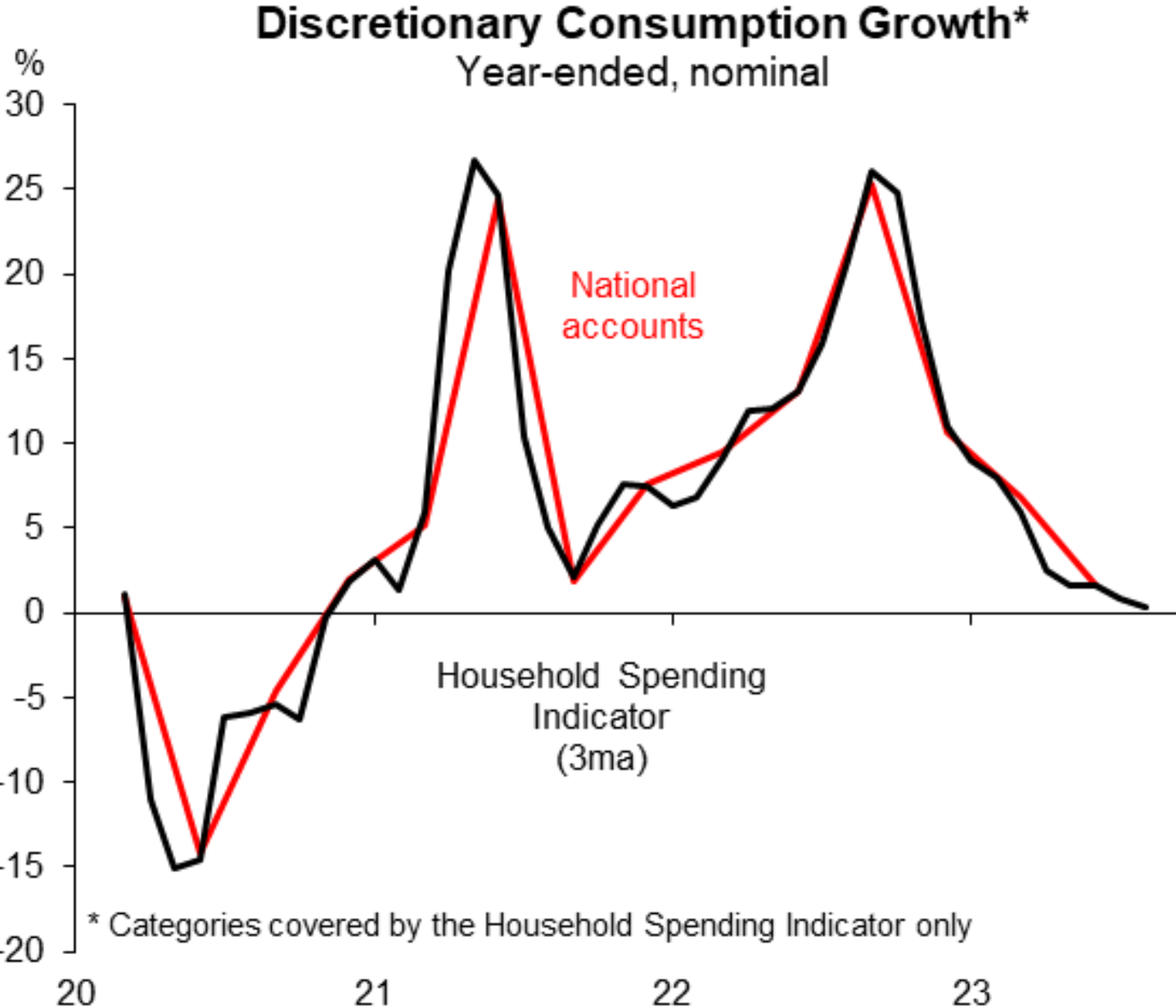

The decline in consumption is being driven by discretionary spending:

Source: Justin Fabo (Macquarie Group)

The Australian economy was already experiencing a per capita recession in the June quarter, following two consecutive -0.3% prints:

The recession has been driven by a 0.2% contraction in real household consumption per capita in the year to June:

Household consumption comprises more than half of Australia’s economic growth. Therefore, when it falls, Australia’s GDP usually follows, as shown above.

This explains why the IMF this month forecast a two-year per capita recession for Australia, with 2024 expected to be even worse than 2023.

The Albanese government’s record immigration program is the only thing standing in the way of a “technical recession” – defined as two consecutive quarters of negative GDP growth.

While Australia’s economic pie continues to grow slowly because of record population growth, everybody’s slice of the economic pie is shrinking and broader living standards are declining at a record pace.